.png)

If you are in search of cheap money transfer options to send money to India from the US, you have come to the right blog!

With countless options available in the money transfer marketplace, it is important to know how to navigate the labyrinth of international money transfer services to find the most affordable and secure solution.

This blog is your guide to achieve just that-affordable, cheap, and secure money transfers to India from the USA.

Say goodbye to hidden fees and unfavorable exchange rates as we uncover tips, and services that will empower you to make your international money transfers a breeze.

An international money transfer's cost depends on a few key factors:

If you want to send money in a different currency, it is crucial to understand the intricacies of currency exchange rates.

When you send money internationally, the financial institution or service provider handling your transaction will convert your USD to INR. This conversion rate is where they make a profit, typically offered at a rate higher than the real exchange rates.

To ensure you are getting a fair deal, compare what you are quoted with the real exchange rates, which you can find on any of the currency conversion tools such as XE, Reuters, etc.

While the exchange rate is not a fee, it significantly impacts the cost of the money transfers. It determines the final amount your beneficiary receives.

Given that exchange rates fluctuate due to market conditions, it's best to consider these fluctuations when sending money transfers to India from the USA.

Some money transfer services use third-party banks to facilitate international money transfers. This third party usually deducts a certain fee from the amount that your beneficiary finally receives. The fees vary depending on the banks and are typically not shown upfront.

This fee is imposed by the service provider and the exact amount can differ from one provider to another.

It is applied when you are converting one currency to another. The fee is typically consistent and follows rates established by the government. It's important to be aware that this tax is associated with currency conversion transactions.

Service tax is a charge applied to the commission, not the entire transaction amount. In other words, the percentage applied for service tax is based on the commission fee imposed by the service provider, not the total amount of the transaction.

We all know banks have been the traditional method for sending money overseas for a long time. However, they aren't always the cheapest and most efficient method.

They charge exorbitant fees, offer you poor exchange rates, and often have hidden charges that will increase the overall cost of the transfers.

In addition, even a simple international money transfer involves a lot of paperwork, long waits, and complicated bank procedures.

Your best bet for cheap money transfer options would be online money transfer services. These dedicated money transfer platforms offer much better rates and overall better services.

A website or mobile app is all you need to place the money transfer order and complete the transaction. These platforms are available 24x7 so you can place an order at any time, at your convenience.

Before you decide on which service is best for transfers to India from the US, it is important to know that the cheapest method will depend on your specific requirements such as the transfer size, the transfer speed, the payment method, and the delivery method.

Also, note that the cheapest method may not be the best method for your needs.

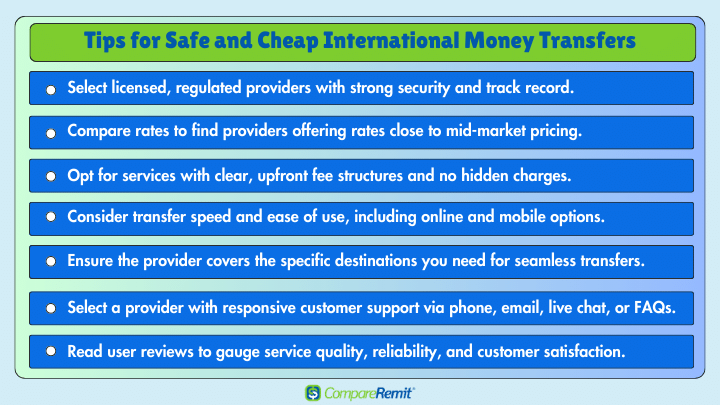

Here are a few tips to help you choose the right service:

Now let's get to the main topic of the blog which is the cheapest ways to transfer money to India from US.

Wise is one of the cheapest online money transfer services to send money anywhere in the world. The service is far more affordable, quicker, and more convenient for anyone looking to send money from the US.

Real Exchange Rates: Wise uses a mid-market exchange rate or the real exchange rate. It’s the rate you see on Google or XE. This will save you from the exorbitant exchange rates that are typically masked as free or zero-commission transactions.

Low Fees: The fixed cost consists of a flat fee of about $1 and a percentage of the transfer value, slightly less than 1%. Credit card fees are higher. Using a debit card or an ACH transfer from your bank account is cheaper.

Upfront Costs: You will see the costs for your overseas transfers upfront and be assured that you will only pay what you see!

Free First Transfer: You can use the referral link which will exempt you from the transfer fee on your first transfer.

High App Ratings. Users rate Wise’s iOS and Android mobile apps 4.3 out of 5 stars.

Fast Transfer Speed: 50%+ of payments are instant, 90%+ arrive in 24 hours

Not Always the Best Deal for Larger Transfers. Some providers don't charge any fees and can offer competitive rate markups, which can make some transfers cheaper than Wise.

With over 25 years of experience, XE is a reputable authority in the currency world. Businesses and individuals alike rely on XE to facilitate comprehensive money transfers and provide competitive rates and foreign exchange risk management solutions.

Competitive Exchange Rates: XE Money Transfers typically provides favorable exchange rates that are close to the interbank rates.

No Transfer Fees: They often do not charge any transfer fees.

Cheaper for Large Transfers: It offers the cheapest rates for large transfers ($4000 and above). A good pick for large bank-to-bank transfers.

Transparent Pricing: XE offers clear and detailed information about the exchange rates and any potential fees, ensuring you know exactly how much your recipient will receive.

Market Updates and Tools: You have access to valuable market insights, currency conversion tools, and historical exchange rate data, helping you make informed decisions when transferring money.

Limited Delivery Option: Only offers bank-to-bank transfers.

Complex Fee Structure: The fees of XE can be somewhat complex and may not be the cheapest out there. Additionally, the recipient's bank may impose additional fees for receiving international transfers, and these fees are beyond the control of XE money transfers.

Skrill is a trusted e-wallet platform that enables international money transfers over 40 currencies. Though it is originally associated with the gambling industry, it is a safe and secure platform. It was founded in the UK and it is regulated by the Financial Conduct Authority.

Zero Transfer Fees: If you have a Skrill account, you can send money to an international bank account with zero transfer fee. There are also no transfer fees for receiving the money to your Skrill account or when paying a merchant directly from your Skrill wallet.

Prepaid Mastercard: Skrill offers a prepaid Mastercard linked to your account that can be used to withdraw money from ATMs and make in-person purchases.

Multi-Currency Wallet: You can hold and manage multiple currencies within your Skrill account, enabling you to make exchanges and send money in different currencies with ease.

Verification Process: Some users have found the verification process for Skrill accounts to be cumbersome and time-consuming.

Fees: Skrill may charge fees for certain transactions, including currency conversions and withdrawals, which can make it less cost-effective for some people.

Inactivity Fees: Skrill may charge inactivity fees for accounts that remain dormant for an extended period, which can be a concern if you do not use the service frequently.

Withdrawal Restrictions: There may be limits on the amount of money you can withdraw from your Skrill account, which can be restrictive if you have larger transfer needs.

Remitly is among the most affordable and popular international money transfer providers for sending money to India from the US. Founded in 2011, millions of people have used Remitly to send money to friends and family overseas.

Competitive Exchange Rates: Remitly offers competitive USD to INR exchange rates

Best Option of In-person Cash Pick-up: Opt for cash pick-up at 100,000+ locations in India.

Multiple Transfer Options: Provides different delivery options, including bank deposits, cash pickup, mobile money, and airtime top-up.

Promotional Offers: Remitly occasionally offers promotional rates and discounts for new users. You can also earn rewards when you refer your friends and family and use an offer code to redeem an offer.

Express and Economy Services: Offers both express and economy transfer services, allowing users to choose the speed of their transactions, with corresponding fee differences.

Transparent Fee Structure: Provides clear information on transfer fees and exchange rates.

Fees for Express Transfers: While Remitly may offer lower fees for economy transfers, the fees for express transfers can be relatively high due to its faster delivery speed.

Inconsistent Transfer Fees: Transfer Fees vary depending on the country and quantity transferred.

Limits on Transfer Amounts: There may be limits on the amount of money you can send or receive which can be a concern for users with larger transfer needs.

Based out of Singapore since 2014, Instarem makes money transfers easy, quick, and reliable for everyone who needs to send or receive money. One of the top picks for those looking to transfer money from the US to India at an affordable rate.

Competitive Exchange Rates: They offer competitive exchange rates, which means you get more money in your recipient's currency compared to other providers.

Low Fees: They charge low fees for their services, which can save you money on your international transfers. (Anywhere between 0.25% to 1% in fees).

No Hidden Charges: Unlike some of its competitors, Instarem has no hidden fees or charges, so you can be sure of the total cost of your transfer upfront.

Fast Transfer Times: Offers fast transfer times, with some transfers arriving within minutes or hours, depending on the recipient country and payment method.

Reward Points: You earn 25 InstaPoints when you sign up. Earn an additional 100 InstaPoints when you complete your e-verification in the first 36 hours after you sign up. You can redeem these points in your next transfer.

Only Allow Bank-to-Bank Transfers: Instarem supports only bank-to-bank transfers, and alternative methods such as bill payments, cash-pickup, and mobile top-up options are not available.

Transfer Limits: There may be limits on the amount of money you can send or receive, which may be not ideal for larger transfers.

SBIC or State Bank of India-California is a branch of the State Bank of India (SBI) located in California, USA. It provides various banking and financial services to individuals, businesses, and the Indian community in California.

Indian Diaspora Services: SBIC caters to the needs of the Indian diaspora in the US, offering services and solutions tailored to this community, such as NRI accounts and remittances.

Fee-Free Online Bank Transfers: With SBIC’s remittance service, you can transfer directly to any bank in India online at zero costs within a few hours.

Competitive USD to INR Exchange Rates: The exchange rates are subject to change and can vary based on the transfer amount and transfer method. For example, tiered exchange rates for in-branch transfers mean the higher the transfer amount, the higher the exchange rate.

Limited Coverage: The physical presence of SBI California is limited to a few locations in California, which can be inconvenient for customers outside those areas.

Limited Currency Options: SBI California primarily deals in Indian Rupees (INR) and may have limited currency exchange options for other currencies, which may not be suitable for all customers.

Time Zone Differences: Time zone differences between California and India can result in delays in customer support and transaction processing during certain hours.

ICIC Bank is India's largest private-sector bank. The bank launched Money2India, an online remittance service to facilitate money transfers to India from countries like the USA, UK, Canada, Singapore, and UAE at some of the best exchange rates available in the market.

Money2India was founded with the aim to cater to Non-resident Indians sending money to India.

Well-Established Institution: ICICI Bank is a reputable and well-established financial institution, which can instill confidence in customers regarding the security of their funds and transactions.

Hassle-free Bank Account Transfer: One of the best options to send money to a quick transfer to an Indian bank account.

Competitive Exchange Rates: ICICI Bank offers competitive exchange rates, especially for larger transfer amounts.

Accessible to Non-ICICI Customers: Sign-up is open to everybody and not restricted to ICICI Bank customers.

Quick Pay Feature: Repeat a transaction in only 3 clicks. Set up recurring transfers or schedule a transfer for the future, minimizing your hassle.

Complex Transfer Fee Structure: There isn’t a way to estimate your transfer fee until right before you confirm your transfer.

Not Ideal for Small Transfers: The less money you transfer, the poorer the exchange rate you get in comparison to if you are sending a large sum of money.

WorldRemit is a leading digital money transfer provider that lets you send money to all states and Union territories in India from the U.S.

WorldRemit is a low-cost alternative to other high-street bank transfers. It is also one of the fastest ways to send money abroad.

Multiple Sending Options: Users can choose from various sending options, including bank transfers, cash pickup, mobile money, airtime top-ups, and more. This flexibility allows you to tailor your transfers to the recipient's needs.

Lower Transfer Fees: Charges lower transfer fees than other similar money transfer companies.

Transparent Fees: It is known for its transparent fee structure, with clear and upfront information about the charges involved in a money transfer.

Fee-Free Transfers Offer: The first 3 transfers for new customers are free of cost.

Speed: Many transfers are completed within minutes, especially if using services like mobile money or cash pickup. This can be crucial in emergency situations.

Inconsistent Transfer Fees: Costs include transfer fees and a markup on the exchange rate, and can vary depending on the delivery method you choose - which can get expensive.

Transfer Limits: WorldRemit imposes certain transfer limits, which vary depending on the destination country.

Limited Delivery Options: All delivery methods are not available in all locations. This can be a drawback for users who prefer a specific delivery method.

Placid Express was established over two decades ago and offers international payment services to a range of countries in Europe and Asia including India. Placid offers easy and economical cross-border money transfers because of its direct partnerships with a number of banks and financial institutions.

Competitive Rates: Placid offers competitive exchange rates, which can result in cost savings for users compared to traditional banks.

Low Fees: Placid's fees for money transfers are lower than those charged by traditional banks and some other online transfer services, making it a cost-effective choice.

Fast Transfers: Many Placid transfers are processed swiftly. For direct bank account transfers, it can take 3 business days. If you pay with a card, the money gets delivered in as little as 10 minutes in some cases.

SpotCash! Service: This service allows your recipient to collect the payment in local cash from an agent.

Fees: The transfer costs for card payments are fairly high.

Limited Coverage: Placid may not be available in all countries, so the range of countries you can money is limited.

Potential Transfer Delays: A few things could slow down the transaction, like the recipient's bank's processing time or the delays caused by the intermediary bank.

Transfer Limits: Placid has limits on the amount of money that can be sent within specific time frames. This can be inconvenient for people or businesses with large transaction needs.

User-Friendly Interface: Some people have noted that Placid’s website is not the most user-friendly, especially for those not familiar with online remittances.

Sending money to India from the US doesn't have to be a costly endeavor. With the right approach and using the various options available for cheap money transfers, you can save both time and money when you send money to India from USA.

Whether you're supporting your family back in India, making investments, or simply need to transfer funds for any reason, the key is to stay informed, explore your options, and choose the one that best suits your needs.

You can make your international money transfers more affordable and efficient by comparing exchange rates and fees and considering digital remittance service providers.

To find the best dollar-to-rupee rate, use CompareRemit for real-time USD to INR exchange rates from the best remittance providers to send money to India today!

15778 views

15778 views