.png)

In an ever connected world, online money transfers are naturally the preferred and most convenient method for sending money across international borders, making it easier than ever to support your family, friends, or business partners in the Philippines.

Whether you're an OFW (Overseas Filipino Worker) or a person with ties to the Philippines, this blog will walk you through the step-by-step process of sending money through GCash, the Philippines’ leading mobile wallet, to effortlessly and securely send money to your loved ones.

Say goodbye to long queues and lengthy paperwork – and say hello to instant and accessible money transfers.

Gcash is a mobile wallet and financial services platform based in the Philippines which came into operation in 2004. It was introduced by Mynt, a subsidiary of Globe Telecom, one of the Philippines’ major telecommunications companies.

GCash allows users to carry out various financial transactions, mobile payments, and services through their mobile phones, making it a convenient and efficient way to manage money.

You can make bank transfers, pay bills with QR codes, take out loans, and top-up airtime on your mobile phone. It is one of the most popular mobile wallets in the Philippines and the most convenient option for Overseas Filipino Workers (OFWs) to send money to their loved ones in the country.

With 81 million active users and 2.5 million merchants and sellers as of May 2023, GCash is truly the undisputed mobile wallet king in the Philippines.

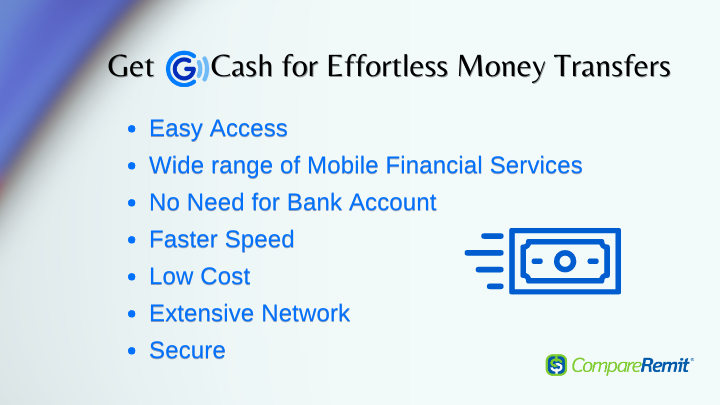

This is especially important for people who want to send money to the Philippines. GCash offers multiple benefits for sending money to the country:

Convenience: You only need a mobile app to send money to friends and family in the Philippines making it easily accessible and convenient. You need not go to any money transfer centers to make a money transfer.

Mobile Services: Apart from money transfers, it offers a wide range of financial services, such as bill payments, online shopping, and even investments.

No Need for Bank Account: Your recipient does not need a bank account to receive money through Gcash.

Speed: It is faster to send money to Gcash than traditional methods. Your recipient can receive the money instantly or within a few minutes, depending on the transaction type.

Lower Fees: Due to its lower fees, it is a cost-effective method to send money to the Philippines.

Extensive Network: Gcash has a vast network of partner merchants, banks, and money transfer companies in the Philippines, making it easy for the recipients to access and withdraw the money.

Security: Various security measures such as PIN verifications, fingerprint scanning, and two-factor authentication are put in place to protect users’ accounts and transactions.

To use GCash, you need to download the GCash app from the App Store or Google Play and sign up for an account. You will enter your personal details (mobile number, name, address), complete the customer verification process, and create a secure PIN.

After creating your account, you will need to fund your GCash Wallet. There are several ways to do this:

Once your GCash is funded, you can start using it for various transactions, such as:

The best way to send money to GCash, Philippines is through a digital money transfer platform. Gcash has partnered with several top online money transfer companies including Remitly, Skrill, Wise, WorldRemit, and Western Union among others.

These platforms allow you to send Philippine Pesos (PHP) to Gcash in an affordable, quick, and efficient manner.

.png)

Here are the steps to follow:

Using Wise, you can send PHP to any individual or business bank account in Philippines or mobile money to any of the several mobile wallets such as GCash, PayMaya, GrabPay, Starpay, etc. To send money to mobile wallets, you'll need your recipient's mobile number, starting with the country code +63. The maximum limit for money transfers to bank accounts and mobile wallets is 9 million PHP per transfer and 50,000 PHP per transfer respectively. It may take 1-2 working days to complete the transfer.

You can do a Remitly transfer to GCash via Mobile Money in the Philippines. Remitly offers two ways to transfer money to Gcash wallets in Philippines based on how you pay for the transfer. Using a debit card (Express) to pay will take a few minutes for the money transfer while it may take 3-5 business working days if you pay via than bank account (Economy). The GCash wallet limit is PHP 100,000. Make sure you have sufficient funds availability in your account to do the transfer. Remitly is the optimal choice to send GCash from USA if you are looking to make fast and secure mobile payments.

WorldRemit facilitates mobile money transfers to several mobile wallets in the Philippines including GCash. The cash is deposited within minutes. You can send up to PHP 50,000 per transfer and a maximum of PHP 100,000 total remittances per month to the mobile wallet. To avoid delay in transfer, make sure your recipient's details are correct. WorldRemit might be your cheapest option as they often charge no fixed fees, but this depends on the sending country. In the case of top-sending countries like the USA, the company does not charge fixed fees.

Western Union is a well-known international money transfer service that has partnered with GCash to facilitate remittances to the Philippines. To initiate a transfer, you can simply go to your GCash account and proceed to the Cash-In segment within the GCash App and opt for Western Union as your preferred money transfer option. Or you can either go to a Western Union Branch or their website to make the transfer. You will find that sending money to a mobile wallet, GCash is less expensive than sending cash to a pickup location.

MoneyGram, a well-established money transfer company is also a GCash partner, enabling users to receive international remittances directly into their GCash wallets. To send money directly to GCash wallet, either go to the MoneyGram website or any agent location. Provide your recipient's details and select 'Mobile Wallet as your delivery option. Both you and your recipient will receive a notification once the money is sent.

By partnering with GCash, Xoom enables users to effortlessly transfer funds to GCash accounts. To start the transfer process from Xoom to GCash, download the Xoom app, and create an account. Then, enter the transfer amount and choose GCash as the receiving option, provide the details of your recipient's mobile wallet, and pay for your transfer using a PayPal account, bank account, credit card, or debit card.

Xoom may be a popular option for transferring funds to GCasg, however, they are a little expensive due to transfer fees and exchange rate margins. Look for cheaper alternatives on our list.

Pangea provides global money transfers to regions in Latin America and Asia. Through their mobile app, you can make the payment and use your linked bank account or debit card to pay for the transaction. If you pay using a card to transfer money for pickup, your recipient will receive the funds within minutes, while selecting a bank transfer method will take a little longer.

By leveraging its digital wallet expertise, Skrill offers users a secure and efficient way to send money to GCash, contributing to the financial accessibility of recipients in the Philippines. Skrill offers various ways to transfer money to GCash including bank account transfer, payments via debit card or credit cards, and letting you choose mobile money transfer. Opting for bank transfers is typically the cheapest, allowing you to send funds from your bank account to a GCash wallet at a lower cost compared to other payment methods. However, the transfer will take a little longer.

Note: The availability of GCash GCash as a delivery option on the above money transfer platforms can differ due to variables like the sender's location, the platform's offered services, and potential shifts in partnerships. It's recommended to visit the platform's website or app prior to utilizing any money transfer service to verify the current selection of delivery methods and choices for sending money to the Philippines.

The cost of transferring money to GCash can vary depending on the service provider, the country you are sending money from, the transfer method you choose (bank transfer, debit/credit card, etc.), the amount being sent, and any applicable fees for currency conversion or processing. Different remittance platforms and financial institutions might have different fee structures.

Carefully review the terms and fee information provided by the specific service you plan to use to determine the exact cost of the transfer to GCash. Keep in mind that some providers may offer promotions or fee waivers for certain transactions or during specific timeframes.

You can withdraw funds through several options in the Philippines. If you have a GCash Mastercard, you can visit any BancNet or Mastercard ATM, or any GCash Partner Outlet.

Here is the list of the GCash Partner Outlets:

The steps for cashing out might be different with each partner outlet. You can look it up in the GCash App.

GCash is primarily not a currency exchange platform. The currency exchange is usually handled by the money transfer provider or financial institution initiating the money transfer to the Philippines from abroad.

For example:

However, GCash may display the received amount in both the sender’s currency and PHP within the app for the recipient’s reference.

If you want to get the best exchange rates while sending money to the Philippines or abroad, the best way is to compare your options. To compare the best rates to send money to the Philippines using Gcash, use our online comparison tool to check the best providers today!

137774 views

137774 views