Source: Reuters

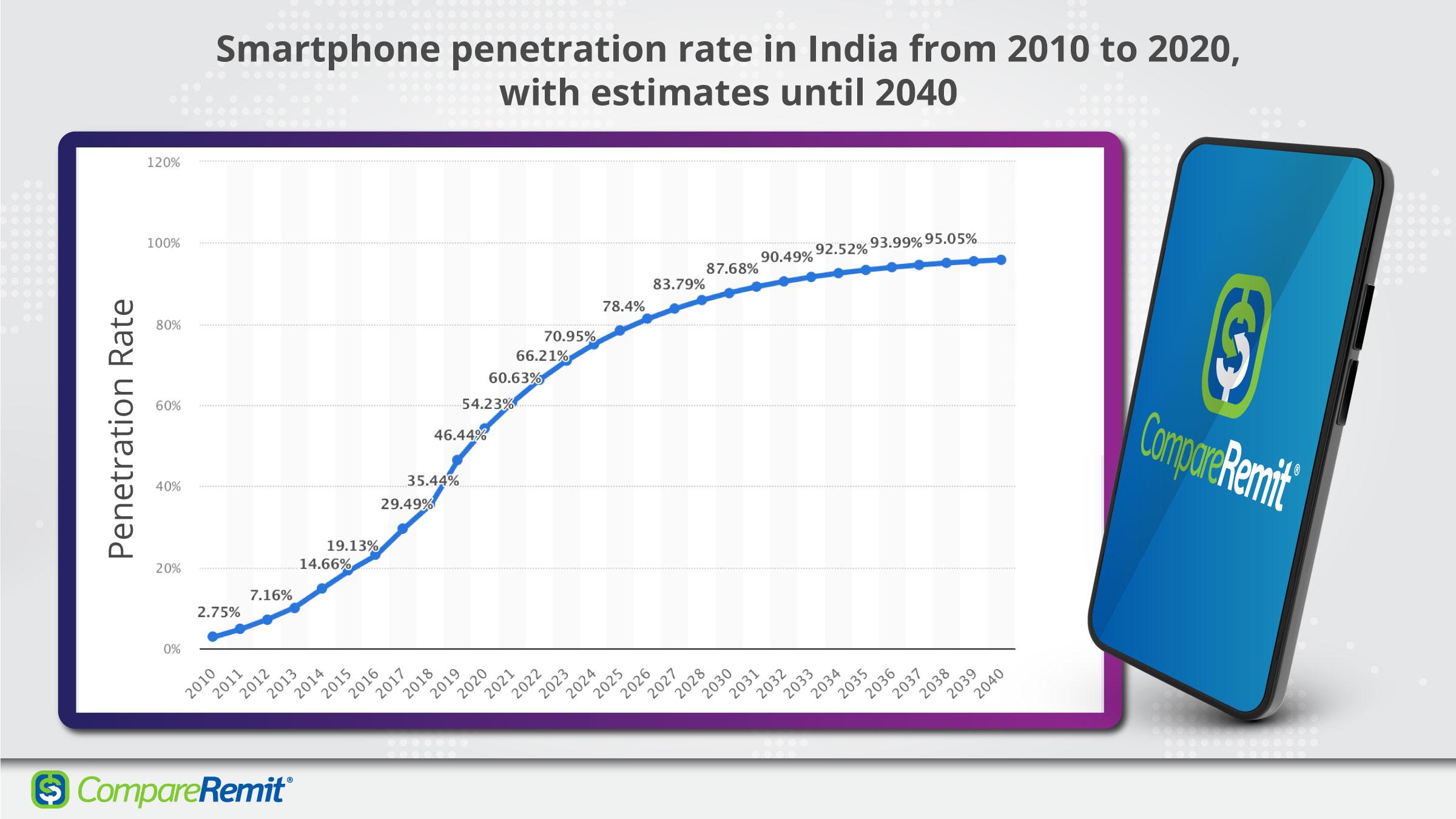

India has the second-largest internet population with over 749 million users as of 2020, of which 744 million users have internet access through their mobile phones. By 2040, this could become around 1.5 billion users. The number of smartphone users in India has now reached 54% of the population and it is estimated to reach 96% in 2040.

The payments industry has undergone a massive transformation in recent years. The implementation of the Unified Payment Interface (UPI) by the National Payments Corporation of India has led several Indian banks and other third-party companies to introduce UPI-enabled mobile payment apps allowing users to send and receive money between UPI-linked bank accounts.

Thanks to the Indian Government's "Digital India" initiative, Indians were already moving towards digital payment systems even before the Coronavirus pandemic hit. The pandemic undoubtedly pushed more and more Indians to adopt cashless transactions.

India witnessed the maximum number of digital transactions in 2020 with 25.5 billion digital transactions, followed by China with 15.7 billion transactions.

The growth is also propelled by increased mobile usage and mobile internet connectivity along with the drive to use cashless transactions, mobile payment apps, and mobile wallets. These digital payment apps are rapidly replacing the traditional way of payment methods such as checks, credit cards, debit cards, etc.

Before we list the best digital payment apps in India, here is the definition of a payment app.

What Is A Payment App/ Mobile Wallet?

A payment app or a mobile wallet is a mobile application that allows you to store your debit or credit card information that can be used to pay for goods and services in digital money instead of using physical cards or cash and also send money online to friends, family, or merchants in an instant. It is just like having a digital wallet on your phone.

Digital payments are a fast-growing industry in India. There are over 50 third-party applications that are operational under the UPI system.

In a bid to ensure parity among the players, the National Payments Corporation of India (NPCI) capped the market share to 30%, limiting their share in the overall volume of transactions on the unified payment interface.

Here is our list of the best digital payment apps in India:

PhonePe

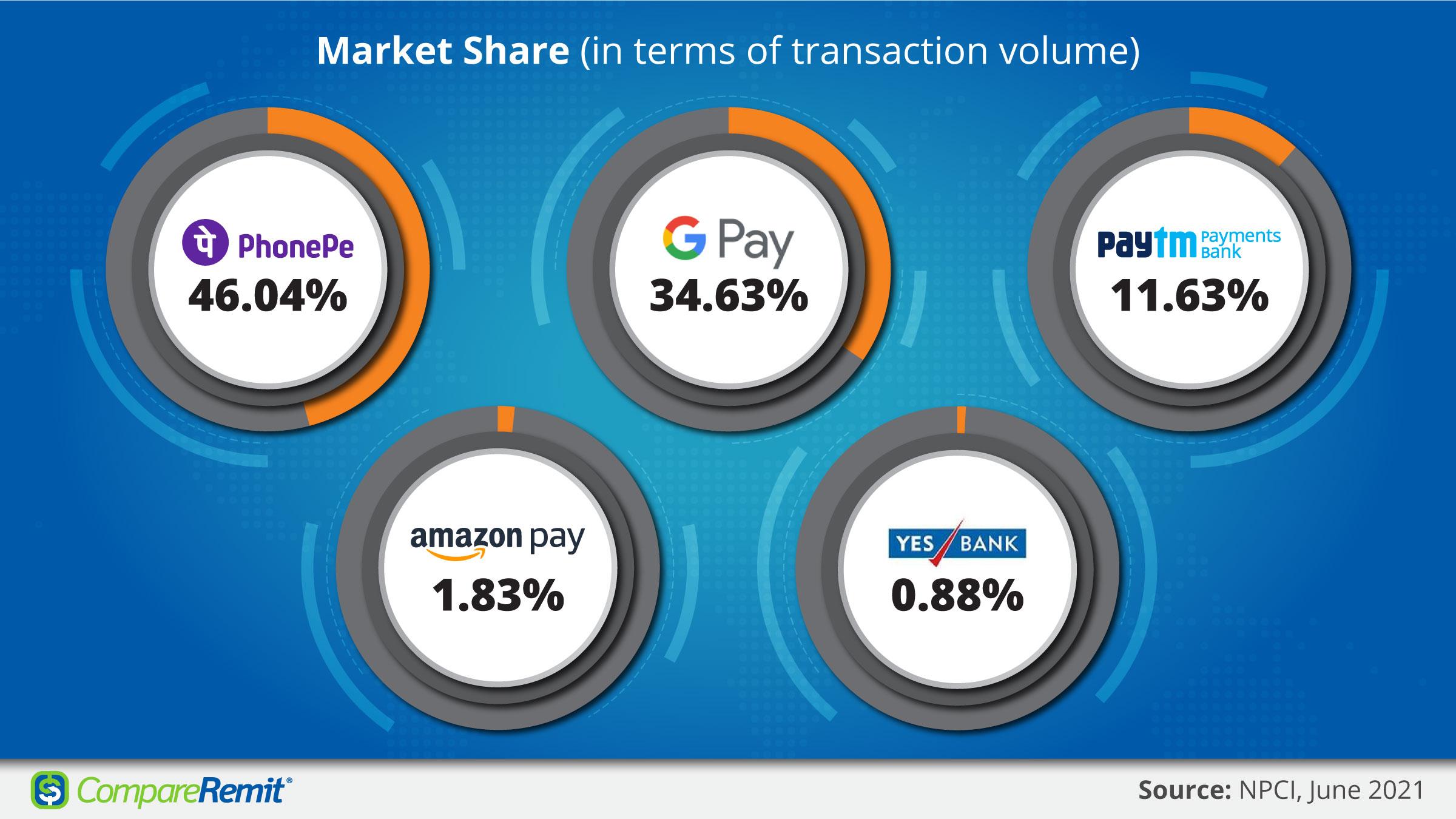

This Bangalore-based online payment app is India's first UPI-enabled payment app, backed by Walmart-owned Flipkart with over 300 million registered users across India. PhonePe leads the UPI payment market in India with a 46.04% market share.

With PhonePe, you can transfer money, recharge, pay bills, shop online, book flights, invest, etc. Since it works on the UPI system, you can link your bank account with your PhonePe account to make transactions. You can also make payments through PhonePe wallet, debit card, and credit card.

You can link your other existing e-wallets such as Jio Money, Airtel Money, and others with the PhonePe app for hassle-free money transfer between these wallets.

Google Pay

Google Pay, formerly launched as Tez in India is a digital payment app from Google which utilizes the UPI to enable in-app, online, in-store, and in-person cashless transactions on mobile devices, tablets, smartwatches. Users can send and request money from other Google Pay users within India.

Google Pay India also has similar product offerings in other markets such as various cashback and other rewards including scratch cards, discounts, etc.

As per the latest data from the NPCI, Google Pay shares 34.36% of the total UPI payment market in India, second to PhonePe. There are over 70 million active users in the country.

Paytm

Paytm (or pay through mobile) is a Noida-based fintech firm that is owned by One97 Communications. Paytm is one of India's largest mobile payments and e-commerce player. It allows cashless transactions through the Paytm app or Paytm website.

Paytm wallet lets you store and send money from one wallet to another wallet or pay directly from your bank account using the UPI. You can recharge your mobile phones, metro cards, data cards, DTH cable and make utility bills payments, postpaid payments. Or book movies and travel tickets, do online shopping or use at various locations such as taxis, grocery shops, restaurants, malls, etc.

With over 150 million active users, Paytm continues to be at the top with the largest volume of transactions by any payment firm in India. Paytm is valued at $16 billion as of 2020.

Amazon Pay

Amazon Pay, owned by e-commerce giant Amazon is an online payment service that allows customers to use payment methods stored in their Amazon account for the purchase of goods and services on Amazon and other third-party e-commerce websites. Users can also pay utility bills, phone bills, send money to contacts, and more.

You can also set up Amazon Pay UPI for UPI transactions by registering through the Amazon app. Amazon UPI services are provided by Axis Bank. There are now 50 million customers using Amazon Pay UPI services.

FreeCharge

Trusted by over 27 million users, FreeCharge is a popular e-commerce website and a digital wallet owned by Axis bank. Customers use FreeCharge to recharge their prepaid, postpaid, metro card, DTH, utility bill payments, and do online shopping and in-store purchases.

Marketed as the one-stop solution for online recharge, it covers major network providers in India including Airtel, Aircel, Vodafone, BSNL, etc. It offers generous cashback, multiple discounts for various transactions.

FreeCharge wallet is UPI-enabled which allows customers to send and receive money through the UPI system.

JioMoney

JioMoney is a digital payment app by Reliance Industries that can be used for bill payments, recharge mobile/DTH, and making payments at thousands of online and physical stores. JioMoney is available as a payment option at several e-commerce sites.

JioMoney also offers discounts, cashback, coupons, and deals.

JioMoney Wallet is available for download on Apple App Store or Google Play Store. The money can be added to the wallet using Net banking, debit card, or credit card or link the bank account.

BHIM

BHIM or Bharat Interface of Money is a popular mobile payment app based on the UPI system and is backed by the government of India. You can link multiple bank accounts in the app and choose the one that will receive the payments which are directly credited to the bank account. And also request money through the app.

Customers can pay using a QR code, UPI pin, mobile number, bank account number, or Aadhar number. It also supports multiple languages.

The app is available for download on android phones and iPhones and once installed, you can register for a UPI ID for the linked bank account. As of June 2021, the monthly transaction through the BHIM app is over 73 billion Indian rupees.

Mobikwik

Founded in 2009, Mobikwik is one of the largest mobile wallets that is used for online payments such as sending and receiving money, mobile recharge, pay utility bills, online and in-store purchases, and more.

Users can use debit or credit cards to add money to the wallet to make the payments. The services are available on a desktop site too. Mobikwik claims to have more than 107 million users, 3 million merchants, and over 200 bill payers on their platform.

The company has a valuation of over $700 billion.

Airtel Money

Airtel Money is one of the mobile wallets available in India that lets you send money, pay bills, recharge your mobile phones, and shop in-stores. Airtel Money is part of the Airtel Payments Bank, a subsidiary of Bharti Airtel.

Users can operate Airtel money without a bank account and even work without an internet connection. It is linked to your mobile number and makes for a hassle-free transaction.

Airtel Money also gives offers and deals for shopping online and making payments. You can get extra talk time if you recharge your Airtel prepaid phone through the app.

Pockets By ICICI Bank

Pockets, a VISA-powered digital wallet provided by ICICI bank allows customers of any bank to transfer money, recharge mobile, make bill payments, shop online at any e-commerce site or use the Pockets Physical card to shop at retail stores.

You can fund the wallet using a debit card or net banking. Since it is a UPI payment app, you can share a QR code or your UPI ID with others to receive payments.

With existing ICICI bank customers, their internet banking user ID and password are all they need to register in the app.

The evolution of payment technology has only made it clear that we prefer payments that are fast, convenient, safe, and simple. And mobile payments are emerging as the needed solution in today's fast-paced lifestyle.

In the Indian context, with the market cap mandated by NPCI and a competitive marketplace with multiple new players, consumers stand to benefit the most from various offers and promotions. We expect to see collaborative efforts to support new features that allow users to send money internationally. The mobile payments industry will continue to grow and evolve to meet the various demands of the customers.

135678 views

135678 views