For sending money from Europe to the United States or vice versa or anywhere internationally, many of us are inclined to approach a bank whether we want to send the money for business or personal reasons.

Banks may seem like an easy option but it is not the most cost-effective and convenient. When compared to specialized money transfers service providers, banks often lack tools and products for a streamlined transfer process, provide poor exchange rates (margin up to 5%), charge huge fees (up to $30 or more), have a longer delivery period, and in many, they have hidden fees.

In this day and age, the traditional way of international money transfers via banks is being challenged by highly competitive international money transfer specialists whose sole purpose is to facilitate money transfers with lower costs, faster speed, and enhanced convenience.

Today, international money transfers are almost instant at the touch of a few buttons, no matter where you are in the world. You can send money online securely or through mobile apps without needing to leave the comfort of your home.

There are several money transfer companies to choose from, each offering competitive exchange rates, low transfer fees, faster transfer speed, different payment methods, and more. Whatever the reason for sending money overseas, it is best to consider your options and choose the best service for your specific needs.

Before we list the top options for your EUR/USD transfers, here are 5 important things you need to consider to find the best way for you to transfer money internationally.

Exchange Rates

Getting the best exchange rates will get you the best value for your money since it affects how much money is received at the other end. The foreign exchange market is highly volatile and the rates can fluctuate constantly. That is why timing your transfer will make a huge difference. A favorable exchange rate on large transfers particularly can save you a significant amount of money.

Fortunately, there are online tools that can help you set alerts for your preferred exchange rates. Some providers allow you to fix exchange rates if you need to make regular payments in the future through a Forward Exchange Contract.

Most upscale banks add a 5%-7% margin on the mid-market exchange rate (the rate you see in Google/Reuters) when converting from one currency to the other (in this case, from EUR to USD). On the other hand, money transfer specialists offer a more competitive rate which is a better option. They offer value for money, added convenience, and also peace of mind for the future.

Fees

Fees can make international money transfers expensive. The fees vary widely between money transfer providers: it can be fixed, free, or a percentage of your transfer amount. It will also depend on the pay-in and pay-out method, the speed, the destination country to name a few factors.

Also, be aware that a zero-transfer fee doesn't necessarily mean you will save money. In such cases, the exchange rate can be very low. Conversely, an attractive exchange rate can come with a higher transfer fee.

Be mindful of hidden fees so that you don't end up losing money without your knowledge and your recipient receives less money than you intended to send.

Speed

Transfer speed is another factor that needs to be taken into account when choosing a service provider. Transferring money overseas can take place within a few seconds, minutes, a few hours, and even more depending on several factors such as the currencies used, destination country, payment method, bank holidays, time zones, etc. The cost of the transfers will also vary with how fast and slow the money is being sent.

Cash transfers are usually instant while it will cost a little extra when compared to bank wire transfers which can take 1-5 business days. In case of an emergency where you need the money to send in an instant, high-speed transfer matters. If you are not in a hurry, the less expensive option lets you save money.

Security

With money transfer companies becoming a popular alternative to banks, it is worth checking the company's reputation by reading online reviews before engaging with any money transfer specialists.

You will have to make sure that they are authorized by appropriate financial authorities such as FCA (Financial Conduct Authority), FinCEN (Financial Crimes Enforcement Network), FINTRAC, or any other regulatory body to carry out money transfers in the country they operate and that your money is safe via secure encryption methods.

Proper research and awareness can protect you from becoming a victim of money transfer scams.

Customer Service

An efficient customer service team is very handy when you need assistance during the transfer process. A dedicated team should be able to resolve any issues with transfers from initial account set-up to the receipt of money by the recipient.

Make sure the money transfer company you choose has a reputable customer service record. There can be many instances where you need to speak to the support team for guidance and to put your mind at ease if you are not familiar with sending money overseas. It can be complicated and confusing at times without a guide.

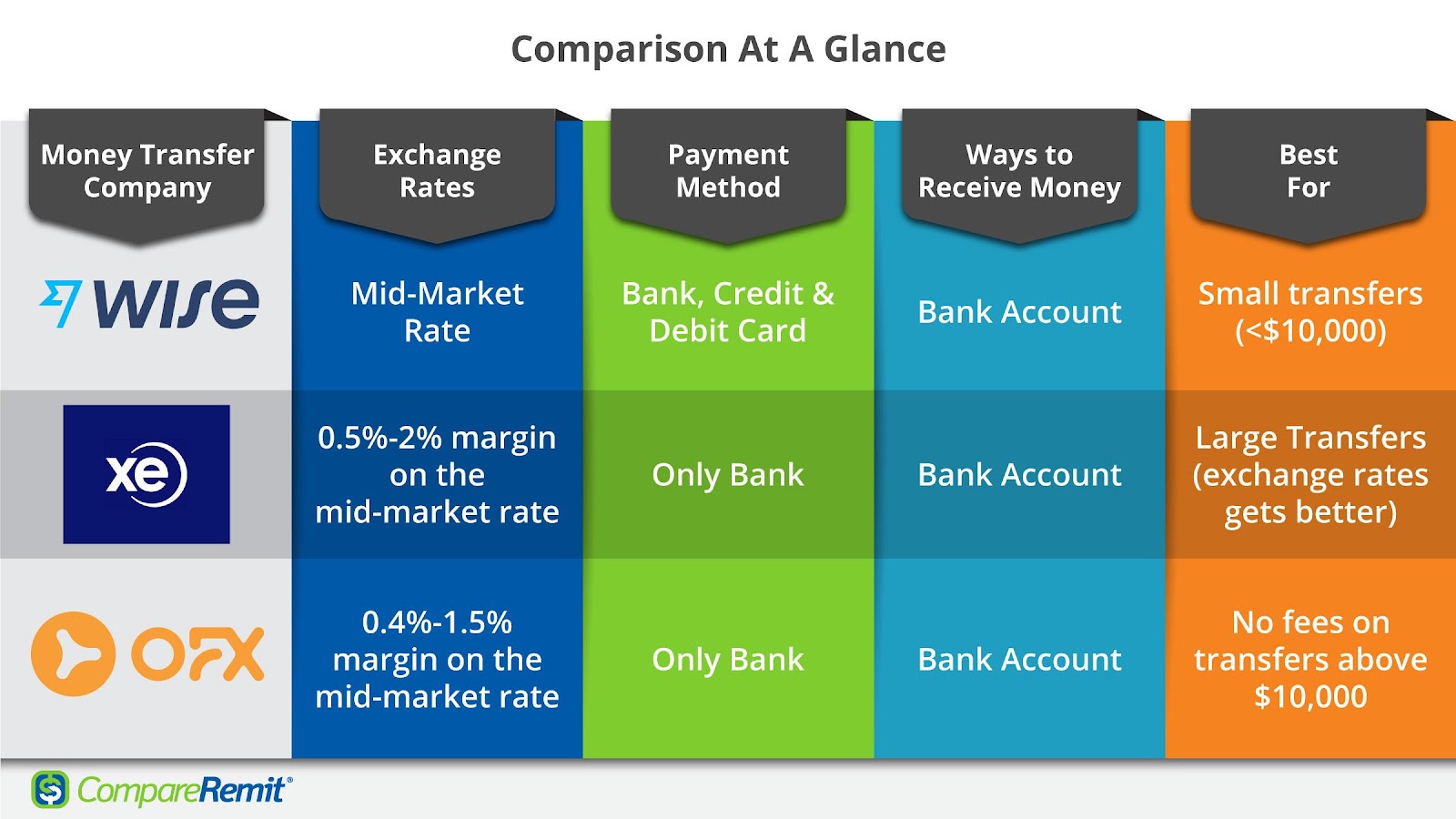

Wise (formerly TransferWise): Best Exchange Rates For Small Transfers

Wise with a valuation close to $11 billion is a London-based financial technology company, popularly known for providing one of the cheapest money transfer services globally, especially if you are sending small amounts. For larger transfers (more than $10,000) a specialist foreign exchange provider can be a little cheaper.

Wise is among the few companies that offer the mid-market rate and have transparent fees. Their fees depend on how fast you want the transfer to be, the transfer amount, how are you paying, and which currencies are being used.

You can pay with your bank account, debit card, or credit card. The cheapest is direct bank debit or ACH, followed by bank wire transfer, debit, and credit card.

Since Wise only offers bank-to-bank transfers, your recipient will need to have a bank account in the U.S. But the services they offer are much cheaper than the traditional bank transfer services. You also get access to a multi-currency account and a Mastercard debit card. There are services for both businesses and individuals.

It is regulated by multiple financial authorities including FCA in the UK and FinCEN in the U.S. and other agencies around the world. Wise uses the latest encryption technology to safeguard your money.

It is extremely easy to create an online account or you can download Wise's mobile app for Android and Apple iPhones. You will need to provide the recipient's details including their bank details. The transfer can take anywhere from minutes to a few days.

Wise has a Trustpilot rating of 4.6 out of 5 which is one of the best.

XE: Best Exchange Rates For Large Transfers

XE is a Canada-based online foreign exchange company that offers international money transfers to over 170 countries in more than 60 currencies. It is a trusted and reliable money transfer service provider with low fees.

XE charges no transfer fee but puts a small mark-up (in the range of 0.5%-2%) on the mid-market exchange rate. Most importantly, you get better exchange rates with larger transfers, which means the margin gets smaller as the transfer amount increases. Once you are all set to transfer, you will be able to see the exchange rate offered for that particular transfer.

There is no limit on the transfer amount with XE. You can send up to $500,000 or currency equivalent online. You can get in touch with their currency experts to guide you through the transfer process for larger transfers.

You can transfer money on their website or mobile app after setting up an account and providing the necessary information like recipient details, transfer amount, etc. You can only pay through a bank account. There is no card option. The majority of the transfers are completed in a day although they can be delayed due to certain factors. You can track the transaction online.

Trustpilot rating is 4.5/5 with over 46,000 reviews.

OFX: Fee-Free Online Transfers

OFX, an Australia-based online foreign exchange company has been in the money transfer business for more than 20 years providing money transfer services to over 190 countries, in over 55 currencies. It has a wide banking network, physical offices spread across the world, and is monitored by over 50 regulators globally.

With OFX, customers can send money online with no fees on transfers over $10,000. For smaller transfers below $10,000, a flat fee of $15 is charged. Do keep in mind that OFX does have a minimum transfer amount of $1,000. So it is not ideal for users sending smaller amounts of money.

OFX makes money by putting a small margin on the mid-market exchange rate (usually 0.4%-1.5%) which is way lower than what banks charge. You can lock your preferred exchange rate for 24 hours.

Money transfers can be done via their online platform or mobile app. Sign up for an account with your personal details and set up for a transaction online. You can also check rates and track your transfers.

Payment is to be done through a bank account, so your recipient needs access to a bank account to receive the money. The money typically arrives in 1-2 days but can take longer (3-5 days) with certain currencies.

OFX offers excellent customer service which is available 24/7 both on phone and email. The advantage of having a global presence is that customers in different time zones don't have to worry about the absence of customer support at any point in time.

OFX has a Trust pilot rating of 4.3 out of 5.

There are several other options apart from our top 3 picks for EUR/USD transfers. The point is each of the options has both advantages and disadvantages. You will have to decide the best one according to your needs. It could be the speed, low fee, exchange rate, transfer amount, etc that will determine your choice.

A little research, planning, and comparing your options can get you the best deal for sending money overseas.

19541 views

19541 views