Travel insurance is an essential aspect of trip planning, providing financial protection against unforeseen events such as trip cancellations, medical emergencies, and lost luggage. However, finding the right travel insurance plan at an affordable price can sometimes be challenging. In this comprehensive guide, we'll explore strategies to help you save money on travel insurance without compromising on coverage or quality.

Before diving into ways to save money on travel insurance, it's crucial to understand what travel insurance entails. Travel insurance typically offers coverage for various aspects of your trip, including trip cancellation or interruption, emergency medical expenses, baggage loss or delay, and travel assistance services. By purchasing travel insurance, travelers can mitigate financial risks associated with unforeseen events during their journey.

The cost of travel insurance can vary depending on several factors, including:

If you are apprehensive about giving away your money on travel insurance, there are many ways to cut down on the cost of the insurance plan.

Here are some tips to save money on your travel insurance plan.

Conduct thorough research and compare quotes from multiple insurance providers to find the most suitable plan at the best rate.

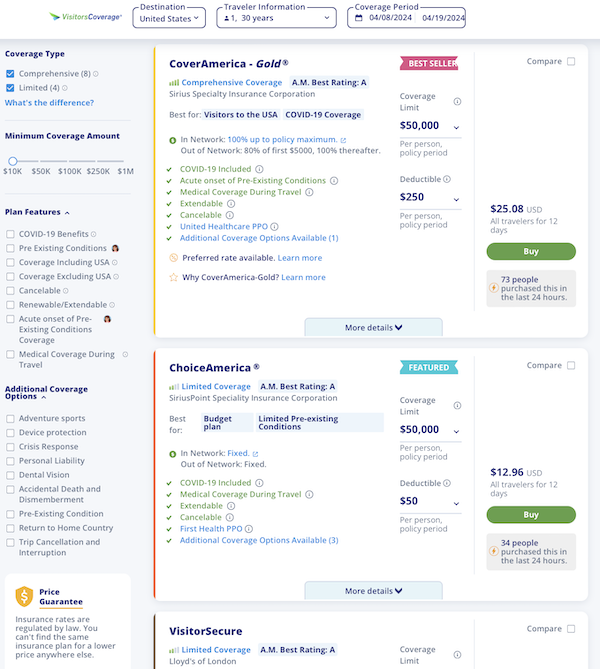

Utilize online comparison tools to evaluate coverage options, premiums, and exclusions across multiple plans. Websites like VisitorsCoverage allow you to compare prices and coverage options from various insurers, allowing you to make an informed decision for your needs.

As shown here, comparison sites, like VisitorsCoverage, allow you to compare and contrast various travel insurance plans based on your custom needs. You can customize the plans available to you by specifying your coverage amount, plan features–including COVID-19 coverage and pre-existing conditions coverage–available, and additional coverage options.

If you are considering visiting multiple comparison sites, let us save you the hassle. Insurance prices are regulated. This means that the same plan with all conditions remaining constant will not have a lower price at other agents, travel insurance aggregators, the insurance company issuing the plan, or any other source.

However, similar plans by different companies may have a price differentiation depending on the customizations you enter, hence it is critical to evaluate inclusions and exclusions in the policies.

Don’t pay for coverage you don’t need. It is vital that you customize your plan to get the most specific coverage for you. Luckily, modern-day comparison tools and insurance providers allow us to do just that. When purchasing your policy, a big money saver can be avoiding purchasing unnecessary add-ons or upgrades that may inflate the cost of your policy. Assess your travel needs and opt for coverage that aligns with your specific requirements.

It is important to know what exactly your travel insurance plan entails and what it covers. Make a list of things that you need to be covered depending on the types of trips you will be taking and if there are any specific medical conditions that may need attention.

The details are always in the fine print. Don't just look at the premium value, read the policy document for inclusions and exclusions in the plan. In the long term, this will save you money and trouble.

However, there is a strong caveat to this. While opting for the cheapest plan may seem cost-effective initially, inadequate coverage could lead to significant expenses in the event of a claim. Should you run into an emergency that is not covered, you will have to pay out of pocket. At the end of the day, the cheaper plan may end up costing a whole lot more. Read policy documents thoroughly to understand coverage details and exclusions before making a decision.

When booking flights or accommodations, you may encounter offers to purchase travel insurance directly from the booking site. Skip the checkbox for travel insurance on these booking sites. These plans often come with commissions and may not provide tailored coverage. For optimal savings and personalized coverage, opt for a separate plan from reputable insurers.

Sometimes, these add-on plans might seem like a good deal. However, keep in mind that, many times, these plans try to be a one size fits all solution. The amount of premium will vary depending on who is buying the plan. For example, an older person traveling with medical issues will pay more premium than a young person traveling with no medical issues. Using a “one size fits all” option may lead to a situation where you have to pay out of pocket in the case of an uncovered medical emergency.

For those looking for trip insurance rather than travel medical insurance, there is a great option you may already be accessing without realizing. Some credit cards offer complimentary travel insurance benefits, such as trip cancellation, trip interruption coverage, and baggage delay protection. Cards such as Chase Sapphire Reserve are well known for their comprehensive travel insurance coverage.

Review your credit card's terms and conditions to understand the extent of coverage provided and consider leveraging these benefits as a supplement to your travel insurance plan.

You could always use travel protection offered by your card as a top-up to another policy that covers the emergency medical expenses. There is no reason to spend extra money on trip insurance when you are getting the benefits as a cardholder.

Explore review websites and rating platforms to gain insights into the products and services offered by leading travel insurance companies. Reading reviews can help you make informed decisions and ensure you receive excellent customer service.

There are several review websites and rating websites such as VisitorInsuranceReviews.com, Trustpilot where you can read in-depth on the products and services offered by leading travel medical insurance companies.

It is also important that you have access to excellent customer service from your insurance providers to get the best value for your money. Even if you save a few dollars in insurance costs but face unresponsive customer service for hours on end, the situation gets more costly.

VisitorsCoverage is a one-stop shop for travel issuance which also offers an award-winning, industry-leading customer service team. They also offer AI-based customer support for those wanting quick and easy help. You can get in touch with the call team via WhatsApp messages and email. Or call them using their toll-free line number: 1-866-384-9104.

"Cancel for Any Reason" is an upgrade option that lets you cancel a trip for any reason for 40%-75% of your insured trip costs. This option can help you save a lot of money should you run into a reason your trip is canceled. While these riders offer added flexibility, they also come with additional costs that may not be worthwhile for every traveler. But you have to pay extra to include it in your plan.

Insurance companies usually have a list of the covered reasons in “Cancel For Any Reason” trip insurance. These include terrorism, natural calamities, traffic accidents, and more. If it is not listed, it will not be covered.

Sift through the list with a fine toothed comb to see which scenarios are covered. Most travelers find their trip cancellation reasons covered. If you don't need the optional "Cancel for any reason", don't add it.

Some plans have promotional offers that may include this coverage if you purchased the plan within a certain time frame. Make sure to check for any promotions and offers like this.

For frequent travelers, annual multi-trip insurance plans offer significant savings compared to single-trip plans.

With coverage extending for an entire year, these plans provide convenience and cost-effectiveness for individuals who travel overseas multiple times a year.

If your travel expenses, such as airfare or hotel bookings, are refundable, there's no need to purchase insurance for them. If you insure a refundable cost and try to seek reimbursement in the event of cancellations, you will need to show proof that certain prepaid costs were non-refundable or your claim will be denied. Instead, focus on insuring non-refundable expenses to minimize coverage redundancy and reduce premiums. This will reduce the coverage and lessen the premium of the travel insurance that you plan to purchase. It is cost-effective to know which trips need to be insured and when you don't need a policy in the first place.

While the prospect of traveling without insurance can be daunting, finding affordable travel insurance doesn't have to be. By following these practical tips and strategies, you can secure comprehensive coverage without breaking the bank. Remember, investing in travel insurance is an investment in peace of mind, ensuring that you're financially protected against the unexpected twists and turns of travel. Safe travels!

7560 views

7560 views

1.png?v=46)