Money, trade, and issues of sovereignty have been curiously intertwined. The history of Philippine money follows an interesting timeline - from the pre-Hispanic era to the Republic of the Philippines that we know today.

The Peso is the official currency of the Philippines, and Piso is its Filipino name. PHP is its ISO code. The Bangko Sentral ng Pilipinas (BSP), the Philippines' central bank is the issuer of the Philippine Peso. The peso is subdivided into 100 cents (sentimo).

The history of the Philippine Peso through the years can be divided into different periods based on the ruling power of the time. The evolution of the Philippine peso reflects the country's journey through colonization and independence.

Prior to the arrival of Spaniards in the Philippines in 1521, trade among the early Filipinos and traders from China and other neighboring lands was performed using the barter system. Cowry shells then were adopted as a medium of exchange due to the inconvenience of the barter system.

Piloncitos, which are small pieces of gold, became the first form of coinage. It had a flat base engraved with an inscription of the letters "MA" or "M" that resembles the Javanese script of the 11th century. It is believed that this inscription was used by the Chinese traders to identify the Philippines during the pre-Spanish era.

The Spanish introduced the coins to the Philippines. The cobs or macuquinas of colonial mints were the earliest coins that were brought in. These were minted in various Spanish countries around the world.

The Spanish dos mundos that were extensively circulated worldwide from 1732-1772 also reached the Philippines. The coin features twin crowned globes reflecting Spanish rule over the Old and the New World.

The shortage of fractional coins at the time led the Spanish government to create the barillas, crude bronze or bronze coins worth about one centavo in the Philippines. The Filipino term "barya", meaning "small change," had its origin in barrilla.

Coins from other Spanish colonies that reached the Philippines were counter-stamped to legally circulate in the country. Gold coins with the portrait of Queen Isabela were minted in Manila. Silver pesos with the profile of Alfonso XII were the last coins minted in Spain.

The first paper money in circulation was the pesos fuertes which were issued by the country's first bank, the El Banco Espanol Filipino de Isabel II.

The 1898 Declaration of Independence brought a short-lived revolutionary currency replacing the Spanish-Filipino Peso. The first Philippine president, General Emilio Aguinaldo, issued its own coins and paper currency under the Malolos Constitution.

Two types of two-centavo copper coins were introduced into the system. Revolutionary noted in denominations 1, 5, and 10 pesos were printed and hand-signed by Pedro Paterno, Mariano Limjap, and Telesforo Chuidian.

Revolutionary currency was withdrawn from circulation and declared illegal currency after the arrival of the Americans in 1898 and the eventual surrender of General Aguinaldo to the Americans.

The United States took possession of the Philippines in 1901 and established a new unit of currency. The introduction of modern banking, credit systems, and currency made the Philippines one of the most prosperous countries in East Asia.

The country's monetary system was based on the gold standard, and the Philippine peso was pegged to the American dollar exactly half of a US dollar or 2 pesos per USD in 1903 until the country became independent in 1946.

The coins issued bore the designs of Filipino engraver and artist, Melecio Figueroa. Coins in the denomination of one-half centavo to 1 peso were minted.

El Banco Espanol Filipino was renamed to Bank of the Philippine Islands in 1912. After which, all the notes and coins issued up to 1933 were changed from Spanish to English. The treasury certificates replaced the silver certificates series, and a one-peso note was added beginning May 1918.

World War II caused severe disturbances to the Philippine monetary system. During the Japanese Occupation of the Philippines, two kinds of notes were issued. These war notes were in big denominations and had no backup reserves. The Filipinos dubbed it "Mickey Mouse" amidst the worst inflation in the history of the Philippines.

On the other hand, provinces and municipalities issued their own guerrilla notes or resistance currencies which were in low denominations. Most of these were sanctioned by the Philippine government-in-exile to show resistance against the Japanese occupation.

The establishment of the Central Bank of the Philippines in 1949 led to the reintroduction of a formal Filipino currency. The first currencies issued were the English series of banknotes and later in the late 1960s, became more filipinized with the adoption of the Filipino language in the currency and the images of national heroes. A series of notes in denominations of 1, 5, 10, 20, 50, and 100 pesos was launched in 1969.

In 1973, the Ang Bagong Lipunan (ABL) series notes were circulated. The lowest denomination was the 2 peso, and the highest denomination was the 100 peso.

The ABL series was followed by the New Design Series (NDS). The new 500 pesos was launched in 1987. The BSP issued the first 1,000 peso notes in 1991 and 200 peso notes in 2002. It was later retitled as the BSP series and bore the new seal of the BSP.

In 2009, the BSP launched a massive redesign for the current notes and coins to enhance security and increase longevity. The notes displayed popular Filipinos and iconic natural wonders.

In December 2010, BSP released the New Generation Currency (NGC) Series. The full set of NGC coin series consisting of 1 sentimo, 5-sentimo, 25 sentimo, and the 1-piso, 5 piso, and 10 piso coins were released in March 2018.

Currently, banknotes of denominations of 20, 50, 100, 200, 500, and 1,000 pesos are in circulation. All notes are of vibrant colors and have images of famous Filipinos and events in Philippine history as well as the country's endemic fauna and flora and natural riches. The bills' size does not vary but is distinctly different in colors.

In February 2016, the BSP distributed a new 100-peso note, which came with a better purple or purple hue. The 100 peso of the NGC series is still in circulation. The NDS in circulation since 1985 was demonetized in 2017.

On December 11, 2019, the BSP announced that the 20 peso note would be converted into a coin.

Currently, coins of 1,5,10 and 25 cents and 1, 5, 10, and 20 pesos are in use. These coins are from the previous BSP coin series and the newly released NGC coin series.

The BSP declared a redesign of the 5-peso coin of the NGC series. The new design requires the inclusion of bumps on both sides of the coin.

The 100-Piso bill became a subject of controversy after the bill was printed with the then President, Gloria Macapagal-Arroyo was misspelled. The bills incorrectly spelled the President's name as "Gloria Macapagal-Arrovo'' instead of the correct "Gloria Macapagal-Arroyo." 2 million of the erroneous notes were already in circulation as legal tenders prompting a public apology from the BSP.

Many collectors have fueled a secondary market for coins and note with errors using platforms like eBay, where buyers and sellers can bid and auction. Bills with "Gloria Macapagal-Arrovo" became a much sought-after collectors' item.

By August 2006, it became publicly known that the Philippine 1 peso coin is equal in size and weight to a UAE 1 dirham coin. This led to fraud in places that accepted Dirham coins, such as vending machines and parking tickets.

Similar frauds have also occurred in the United States, as the 1 peso coin is roughly the same size as the USD 25 cents coin. Although digital parking meters were not affected, most vending machines will still likely accept it as a quarter.

In the most recent case, President Rodrigo Roa Duterte's middle name was misspelled as "Boa" in the 1,000 Peso banknotes released in 2010. However, the BSP denied that the PHP 1,000 bills with the incorrect surname of the president are not recognized as legal tender by the BSP and did not come from its printing facility in Quezon City.

Fake or counterfeit notes are another problem that all governments and central banks need to watch closely. The BSP runs a reward scheme to encourage the public to report any information on currency counterfeiting, defacement/mutilation of Philippine currency banknotes and coins, or any activity pertaining to currency integrity.

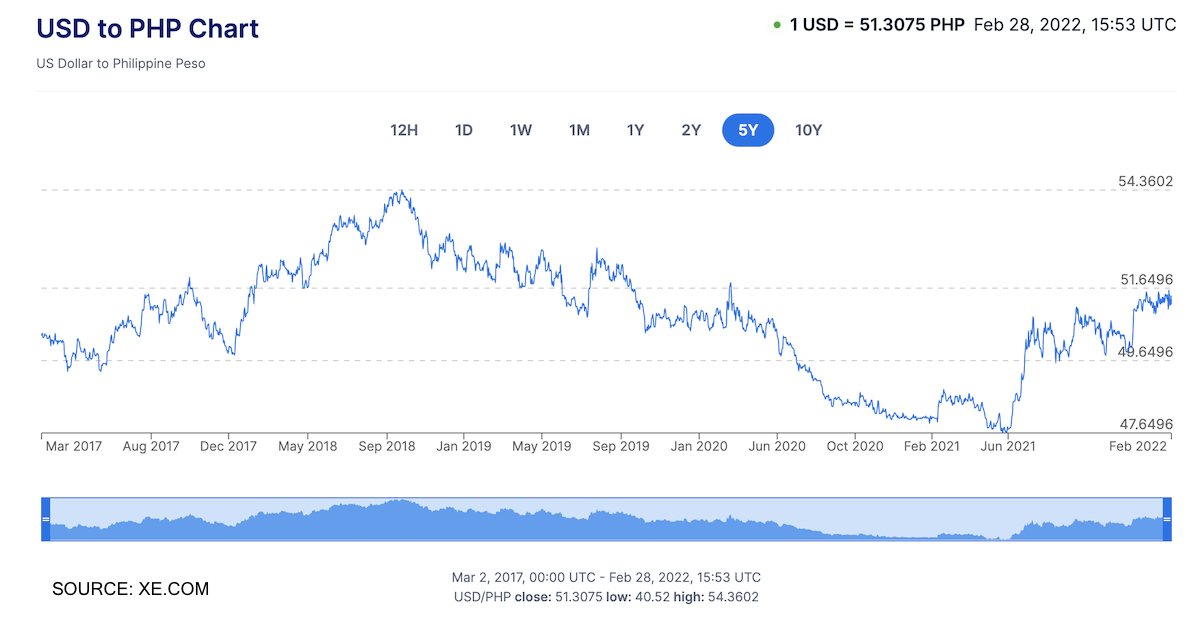

In the history of USD to PHP exchange rate pairing, USD to PHP reached an all-time high of 56.341 in October 2004 and a record low of 2.000 in Jan 1962. The conversion rates of USD/PHP today stand at 1 USD to 51.33 PHP at the time of writing.

The exchange rate fluctuates daily. Many factors affect the exchange rate. The value of the Peso has slumped over the years. However, the weak PHP against the USD has one silver lining: the Overseas Filipino Workers (OFWs) can send more pesos in remittances to families in the Philippines.

OFW remittances are an important source of foreign income for the Philippines. In fact, the United States was the highest source of remittances in 2020, accounting for around 11.94 billion U.S. dollars.

In addition to exchange rates, fees on money transfers impact the remittances being sent. While it is not possible to avoid the transfer fees every single time, there are cheap ways of sending money to the Philippines from the US.

In conclusion, to understand the evolution of PHP, we had to understand the evolution of the Republic of the Philippines. The sensitivity around the topic is an interest for many fields of research.

While socio-political factors impact a currency's standing, it is mostly down to the basic economics - demand and supply. The value of PHP in relation to other currencies is what we know as the exchange rate, such as USD to PHP. Because exchange rates fluctuate daily if you send money from the US to the Philippines, always compare USD to PHP rates before sending money.

166463 views

166463 views