The Indian rupee ended 2022 as the worst-performing Asian currency with a fall of 11.3%, its biggest annual decline since 2013, weighed down mainly by the worries over the nation’s wide current account deficit due to the increase in oil prices sparked by the Russia-Ukraine conflict.

However, heading into 2023, market analysts predict that the Indian rupee will trade with an appreciation bias. Despite the likelihood of a difficult first half of the year, recovery prospects for the second half of the year seem to be more promising.

In this blog, we covered the performance of the US dollar-Indian Rupee in 2022, the Indian rupee's current outlook, what's driving the value of USD, the USD to INR forecast, and much more.

The Indian rupee finished the year at 82.72 to the US dollar, down from 74.33 at the end of 2021 while the dollar index had its biggest yearly gain since 2015.

The index-an effective dollar performance measure- shows its relative strength or weakness compared to a handful of competing currencies such as the British pound (GBP), Canadian Dollar (CAD), Japanese yen (JPY), Swedish krona (SEK), and Swiss franc (CHF).

The continued rupee dollar weakness since January 2022 has been consistent with the depreciation experienced by most dollar-paired currencies.

The surging dollar was a result of the tough monetary policy stance taken by the US Federal Reserve to combat inflation.

Despite the decrease in crude oil prices in the later part of the year, the rupee lagged behind its Asian counterparts as the country's central bank, RBI, mopped up dollars to increase its currency reserves.

The dollar relative to its rival currency gained ground due to hawkish Federal Reserve (Fed) policy and global inflationary pressures.

Although recession worries have lowered the dollar's 2022 high to 11.87%, its overall strength still signals a more positive relative outlook for confidence in the U.S. economy.

The key driver behind the dollar's strength has been the skyrocketing inflation, which prompted the Federal Reserve to raise interest rates six times in 2022. Such monetary policy aims to curb inflationary pressure by increasing the cost of borrowing and spending.

However, rising interest rates also make the dollar more alluring to investors while compelling people to save money.

While current inflationary pressures in the US have reached their highest level of inflation in 40 years, other factors have also strengthened the dollar.

The geopolitical uncertainty brought on by the Ukraine conflict, dramatically increasing energy costs, and labor shortages sparked by the "great resignation," have overall contributed to soaring prices, prompting a forecast of 8% for the U.S. Consumer Price Index (CPI) for the year. This further demonstrates the dollar's counter-cyclical nature and its safe haven status for capital inflows.

The USD to INR exchange rate has been in a bearish outlook in 2023 for several reasons.

The rupee's value against the dollar has received a temporary reprieve thanks to the better-than-expected CPI figures released for October. Inflation dropped from 8.2% in September to 7.7% in October, which was lower than anticipated.

Investors were motivated to swap dollar safety for riskier asset classes amid the reduced likelihood of further Federal Reserve interest rate hikes.

The USD/INR plunged as the US dollar index crashed to the lowest level in 7 months. Inflation plummeted for six straight months while retail sales dropped. A mild recession may be on the horizon as companies like Microsoft, Google, Salesforce are laying off thousands of employees.

As a result, the rupee gained dramatically in strength against the dollar, generating a positive INR to USD forecast.

Second, the recovery of currencies from emerging markets has caused a decline in the USD/INR rate. Some emerging market currencies, such as the South African rand, have recently recovered as investors have adopted a risk-on attitude.

Additionally, it is anticipated that the Indian economy will lead the economic recovery in the coming few months. The continuous outflows from China are a key driver for the Indian economy. As tensions with western nations rise, businesses like Apple have begun moving their operations from China to India.

This rupee gain might only be fleeting, though. Some longer-term predictions see it as a correction in the dollar's long-term strength versus the rupee. The rupee is therefore anticipated to continue to decline over the following months, gradually giving up its gains versus the dollar.

A large wide current account deficit this fiscal year will likely keep the Indian rupee under pressure.

RBI has used up a large number of reserves in 2022 to manage the Indian rupee dropping. If there is an inflow of liquidity back into domestic markets, that will help build back the reserves.

However, the rupee weakness won't lead to runaway depreciation, but a milder 2-3% drop in this fiscal year starting April 1.

The rupee is anticipated to weaken against the US dollar in the first half of 2023 as ongoing concerns about global inflation and the economy continue to dampen risk appetite.

However, the recovery prospects appear brighter in the second half due to the easing of the crude oil and other commodity prices and the expectation that foreign investors will keep buying Indian equities.

Equity inflows, according to analysts, would be a crucial indicator to watch for the rupee for foreign investors.

Two major concerns for the rupee are that the Fed may keep rates higher than expected and India's exports may suffer if the slowdown in developed nations deepens into a sustained recession.

However, experts warned that predicting the direction of the stock market has grown challenging in light of numerous uncertainties going into 2023, such as restrictive monetary policy conditions, a possible recession in some economies, and a prolonged geopolitical conflict.

The critical question is whether weak growth or prolonged inflation would be the main issue in 2023. The U.S. dollar will decline if there is weak growth. If inflation remains high, the dollar will appreciate.

If commodity prices continue to be kept in check, there could be some decrease in the growing twin deficits namely the current account deficit and trade deficit.

In the later part of 2023, the US Federal Reserve may decide to stop raising interest rates since there may be clear signs that inflation is moving in the direction of their target of 2%.

Experts expect the rupee to trade in the range of 80-89 per dollar. The current USD/INR exchange rate is 81.52.

The following INR USD forecasts are based on information that is currently available. Depending on the extent to which key factors, such as interest rates and central bank policy match market expectations, the forecasts could be changed and turn out to be false.

Always conduct your research and remember that future results don't depend on past performance.

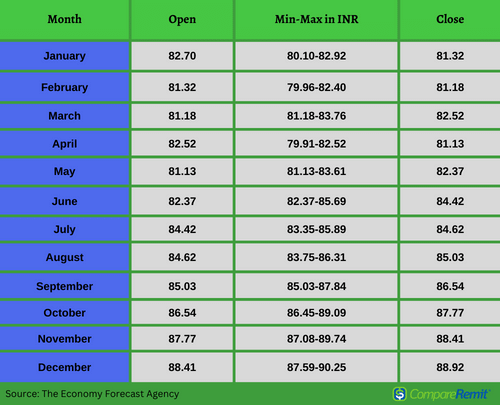

January 2023: At the beginning at 82.70 Rupees. At the end of the month 81.32. Maximum 82.92, Minimum 80.10. The average exchange rate is 81.76.

February 2023: At the beginning at 81.32 Rupees. At the end of the month 81.18. Maximum 82.40, Minimum 79.96. The average exchange rate is 81.22.

March 2023: At the beginning at 81.18 Rupees. At the end of the month 82.52. Maximum 83.76, Minimum 83.76. The average exchange rate is 82.16.

April 2023: At the beginning at 82.52 Rupees. At the end of the month 81.13. Maximum 82.52, Minimum 79.91. The average exchange rate is 81.52.

May 2023: At the beginning at 81.13 Rupees. At the end of the month 82.37. Maximum 83.61, minimum 81.13. The average exchange rate is 82.06.

June 2023: At the beginning at 82.37 Rupees. At the end of the month 84.42. Maximum 85.69, minimum 82.37. The average exchange rate is 83.71.

July 2023: At the beginning at 84.42 Rupees. At the end of the month 84.62. Maximum 85.89, Minimum 83.35. The average exchange rate is 84.57.

August 2023: At the beginning at 84.62 Rupees. At the end of the month 85.03. Maximum 86.31, Minimum 83.75. The average exchange rate is 84.93.

September 2023: At the beginning at 85.03 Rupees. At the end of the month 86.54. Maximum 87.84, Minimum 85.03. The average exchange rate is 86.11.

October 2023: At the beginning at 86.54 Rupees. At the end of the month 87.77. Maximum 89.09, Minimum 86.45. The average exchange rate is 87.46.

November 2023: At the beginning at 87.77 Rupees. At the end of the month 88.41. Maximum 89.74, minimum 87.08. The average exchange rate is 88.25

December 2023: At the beginning at 88.41 Rupees. At the end of the month 88.92. Maximum 90.25, minimum 87.59. The average exchange rate is 88.79.

If you wish to send money to India, the higher USD/INR exchange rates are in your favor because you can get more rupees for your dollars. To send money to India, there are many options available.

The best way to send money to India from the US is online. Compare the top money transfer companies here to find the best exchange rate.

Compare your options and shop around to find the best USD to INR exchange rate using our comparison tool.

#protip Use online money transfer services, which have some of the lowest prices when compared to conventional brick-and-mortar banks, to avoid paying exorbitant fees.

Given the strength of the dollar in 2022 and the bearish forecast for the rupee, the rupee's weakness is likely to continue in the long term.

However, do keep in mind that the forecasts are often inaccurate and subject to correction. The USD to INR forecasts are based on the rate of inflation, central bank policies, and the health of the US and Indian economies.

Send money home to India today while the USD to INR exchange rate is in your favor! Compare rates and providers by using our online comparison tool.

143521 views

143521 views