India received 4.4 percent of the total remittances sent worldwide. In contrast, the average amount of remittances received by other countries is merely 1.5 percent.

According to the 2020 data of the World Bank, a total of USD 529 billion were sent in remittances worldwide. And India received the highest remittance at USD 83 billion, closely followed by China, Mexico, and the Philippines.

But where does this money go? Which state in India receives the highest remittance from abroad? How does this remittance inflow contribute to the development of the Indian economy?

When discussing amounts of money in billions, these common questions come to mind, right? Let's try and find some answers for you.

But first, let's understand the concept of remittances from an Indian perspective.

The Reserve Bank of India has segregated remittances into two main types - inward remittance and outward remittance.

Inward remittances refer to transfers of funds to India from abroad. Such transfers are generally of personal nature and are sent to provide family support. For example, you are an NRI in the US, and you send money to your parents in India - that will be an inward remittance.

Inward remittances are typically sent through a bank, money transfer agents, and more recently through online money transfer specialists such as Xoom, Wise, and Remitly. Sending money to India is easy, quick, and hassle-free if you send money online through a top money transfer service provider.

Outward remittances refer to transfers of funds from India to overseas countries. For example, sending money to your children studying in the US from India will be an outward remittance.

Under the Liberalised Remittance Scheme (LRS), an individual can transfer up to USD 2,50,000 per financial year (April-March).

Inward remittances are typically sent through banks. The industry is not as competitive as the inward remittance industry. Although, we now have a few online money transfer companies offering money transfer services from India to the USA at a faster and cheaper rate than traditional ways of sending money.

Kerala received the highest amount of remittance, according to the latest data by the Reserve Bank of India in 2018.

Kerala topped the charts in 2018 by receiving 19 percent of the total inward remittances. Maharashtra closely followed Kerala at 16.7 percent, Karnataka at 15 percent, Tamil Nadu at 8 percent, and Delhi at 5.9 percent.

It is interesting to note that the Indian state of Uttar Pradesh sent the highest number of workers abroad the same year but received only 3. 1 percent of the remittances sent to India.

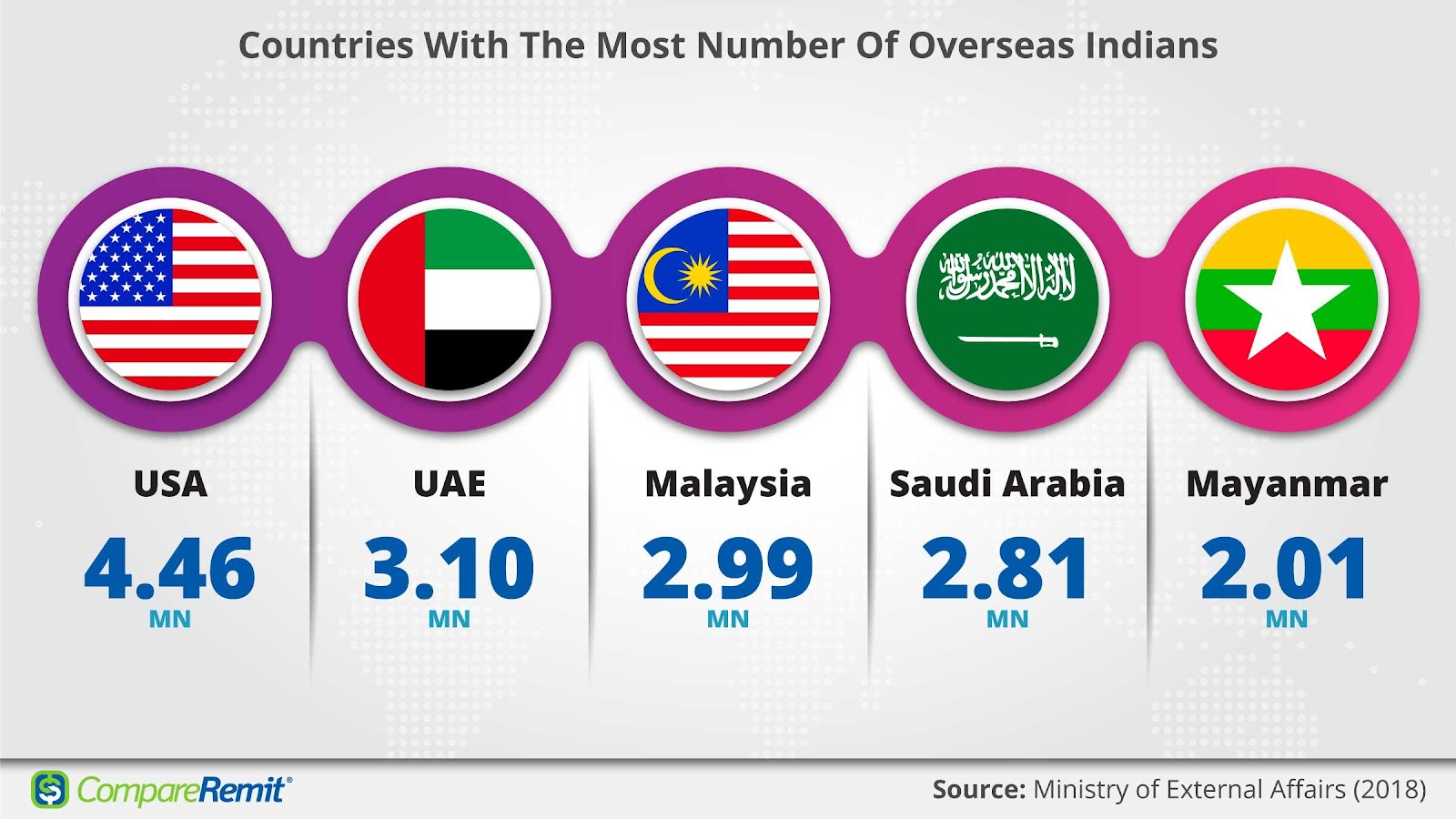

According to the Ministry of External Affairs data, The United States had the highest number of NRIs with a population of 4.46 million in 2018. Closely followed by the United Arab Emirates (UAE) at 3.1 million, and Malaysia at 2.99 million.

In 2018, at the same time as the date referred above, UAE sent the maximum amount of remittances to India. 82 percent of the total remittances were sent from seven major countries, viz.:

Kerala topped the charts in 2018 with 19 percent of the total inward remittances.

However, this boosted remittance may result from the flooding disaster in this southern Indian State.

Please note that the 2018 survey is the latest state-wise distribution of remittances data published by the RBI. Although World Bank publishes data for country-wise remittances every year, we are using the 2018 data for coherence. While it would be interesting to see the updated pre and post Covid trends in migrations and remittances, fresh analysis for India is inhibited by the limited official data available.

According to the latest World Bank data, the United States sent the maximum inward remittance to India at USD 68 billion in 2020, followed by:

There are different ways of sending money to India. Your mode of money transfer determines how much it will cost you to send money. Here are some popular methods of remittance:

Modes of remittance range from traditional methods: like check and demand drafts to more advanced, easier, and faster channels like online money transfer operators, wire transfers, and SWIFT transfers.

Recently, big techs like Google Pay are testing international money transfers through peer-to-peer (P2P) technology. On the other hand, incumbent money transfer companies like MoneyGram facilitate money transfers through a partnership with popular digital wallets or digital payment apps like Paytm.

Hawala is not a legal way of sending money. It has been declared as an illegal way of transferring money by The Foreign Exchange Management Act (FEMA), 1999.

However, people have used the notorious Hawala system to transfer money internationally. It is illegal and can attract heavy penalties including imprisonment.

Most of the remittance constitutes money sent by immigrants to support their families. In fact, according to the latest report released by RBI, 59.2 percent of the remittances received by Indian residents are used for family maintenance.

The remaining is distributed among banks and investments wherein deposits in banks stand at 20 percent and investments in equity shares, land, property, etc., at 8.3 percent.

How Does The Inward Remittance Benefit India?

The foreign inward remittance to Indian residents has lifted many people from poverty and served as a cushion for families during difficult times. Many households rely on remittance for sustenance.

In addition, remittances help support education, provide quality medical care, and entrepreneurship for friends and families.

For India, the inward flow of remittances has been the backbone of the Indian economy. Remittances are one of the crucial inputs in financing India's trade deficit.

In addition, it is also a great source of foreign exchange. It helps spur consumption in India, ultimately reducing poverty, improving access to healthcare and education, facilitating a healthier lifestyle, increasing financial literacy, asset accumulation, and so on.

Remittances play a vital role in the development of states in India, especially in times of crisis. For instance, when the state of Kerala was devastated by floods in 2018, remittances provided a cushion to spring the economy back into action.

As we continue to see new variants of COVID-19 continuing to disrupt the lives of so many people worldwide, remittances provide a crucial lifeline for many households and economies.

In conclusion, while the state-wise distribution will continue to evolve, India will remain the top recipient of remittances worldwide. India is expected to receive another USD 87 billion in remittances in 2021.

What hasn't changed is - how expensive it still is to send money internationally. The global average cost of sending money is around 7 percent. It can reach up to 30 percent depending on the factors such as the method of remittance, exchange rates, sending countries, and receiving countries.

The good news for the NRIs sending money to India regularly is that - as more financial institutions aggressively tap into the NRI market, the market becomes more competitive, and the cost will ultimately reduce further. In fact, for some remittance corridors like USD to INR, CAD to INR, and GBP to INR, the cost of sending money is the lowest.

Financial institutions are moving beyond just money transfers and offering homes loans for real estate purchases, investment opportunities tailored for NRIs, and medical insurances for parents traveling to visit their children.

The Indian government has also laid out policy frameworks to make it easier, cheaper, and quicker. If the Indian diaspora abroad responds well to these incentives, we can expect the number of remittances to India to flourish in the coming years.

57805 views

57805 views