Neobanks is the current buzzword in the FinTech (financial technology) ecosystem and is often considered as the digital disruptor in BFSI (banking and financial services industry).

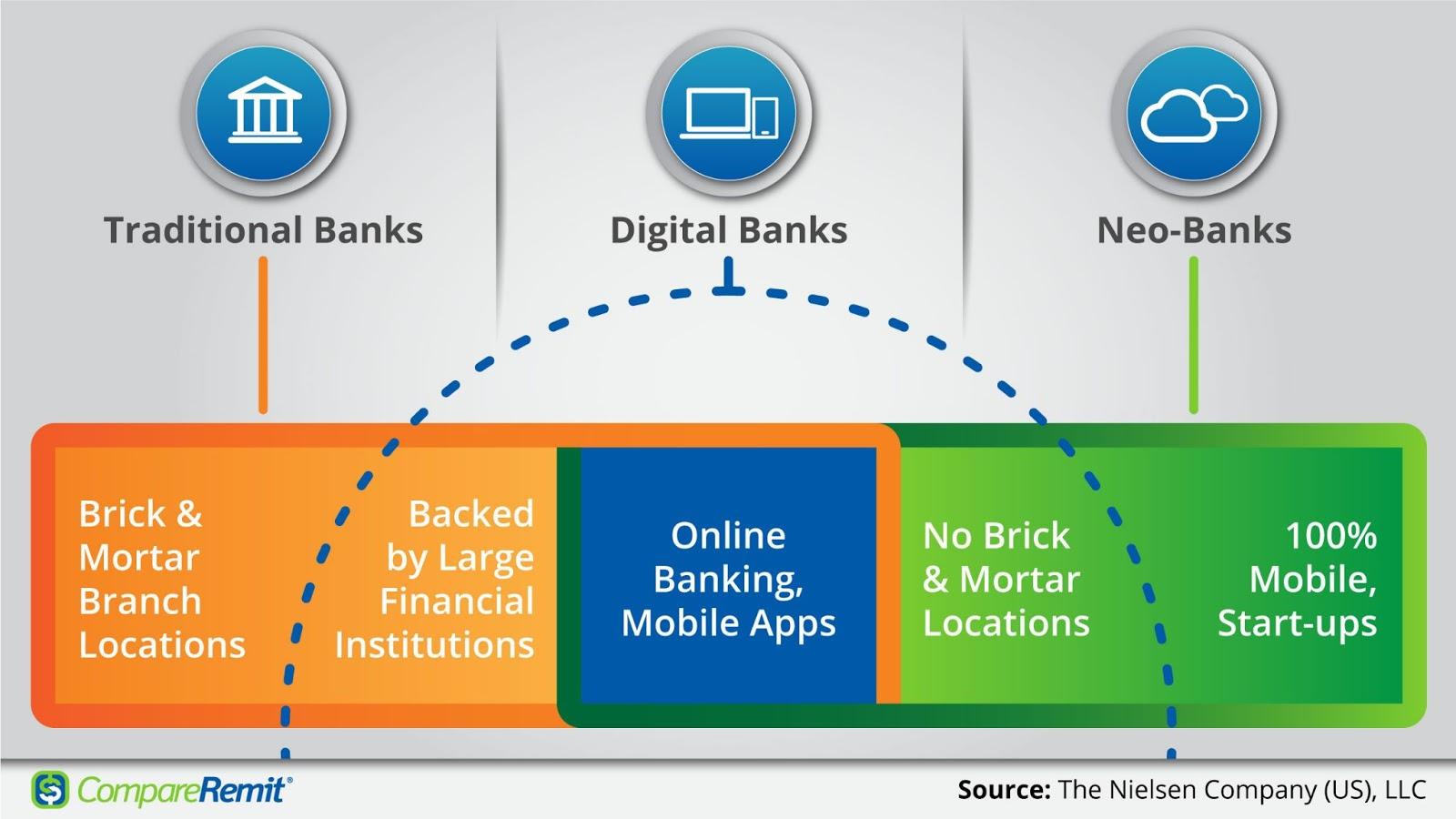

This new breed of digital-only banks, mobile-only banks are posing new challenges to brick and mortar-based traditional banks.

Neobanks such as Monzo, Revolut, N26, Onjuno are challenging the old business model through feature-rich products and services, low cost, ease of use, and seamless online customer experience.

So What Exactly Is A Neobank? And Should You Switch To A Neobank For A Superior Banking Experience?

Neobanks, sometimes referred to as challenger banks, are fintech service providers that offer mobile and online banking with a focus on enhanced user experience, easy accessibility, and low or no-fee services. Neobanks are 100% digital and have no physical branches.

The moniker "challenger bank" was popularized in the U.K to refer to the various fintech banking startups that cropped up in the aftermath of the 2007-2009 financial crisis. These fintech firms are generally known as Neobanks in the U.S.

Since they challenge the traditional banks crippled with outdated infrastructure and legal systems with more customer-centric banking services and better convenience, the term 'challenger bank' is quite apt.

As there are no physical branches, it operates mainly through a mobile application & digital or online platforms.

The app and website as the primary contact point of the customers is more feature-rich and more efficient than other ordinary banking apps.

They also tend to be faster and transparent than the big banks. This lets users have greater control over their money management.

Neobanks is powered by a data-driven decision-making process. These banks collect and analyze data, recognize patterns and trends to understand the behavior of the customers to come out with predictions or results that match consumer needs. They are able to provide highly customized and personalized services.

Neobanks offer a wide range of financial services including:

What sets Neobanks apart from traditional banks are the innovative features and simplified processes including account opening in minutes, free debit cards, instant payments, lower prices, cryptocurrencies, peer-2-peer transfer, mobile deposits, mobile-budgeting tools, user-friendly interfaces, and more.

Neobanks can have different operating models and are categorized into three main types:

Neobanks' business model is different from the traditional banking institutions. A major chunk of their revenue comes from interchange fees paid by merchants when customers purchase goods and services using their debit cards. The interchange percentages can go up to seven times higher than those charged by banks.

Other strategies include freemium pricing strategies, multi-tiered subscriptions, and targeting specific niches. For example, OnJuno, a Neobank, is aimed at Asian Americans. OnJuno is known for offering an attractive saving rate of 2.15%. The OnJuno founders believe that it will serve the diaspora community in the U.S (typically South Asians and East Asians) which are numbered around 20 million, earning a higher average salary of approximately $50,000 per year, more likely to save plus are tech-savvy. Also, OnJuno is located in India which means costs are lower.

The neobanking sector was valued at $34.77 billion in 2020 and is expected to grow at a compound annual growth rate (CAGR) of 47.7% from 2021 to 2028 as per a market analysis report by Grand View Research.

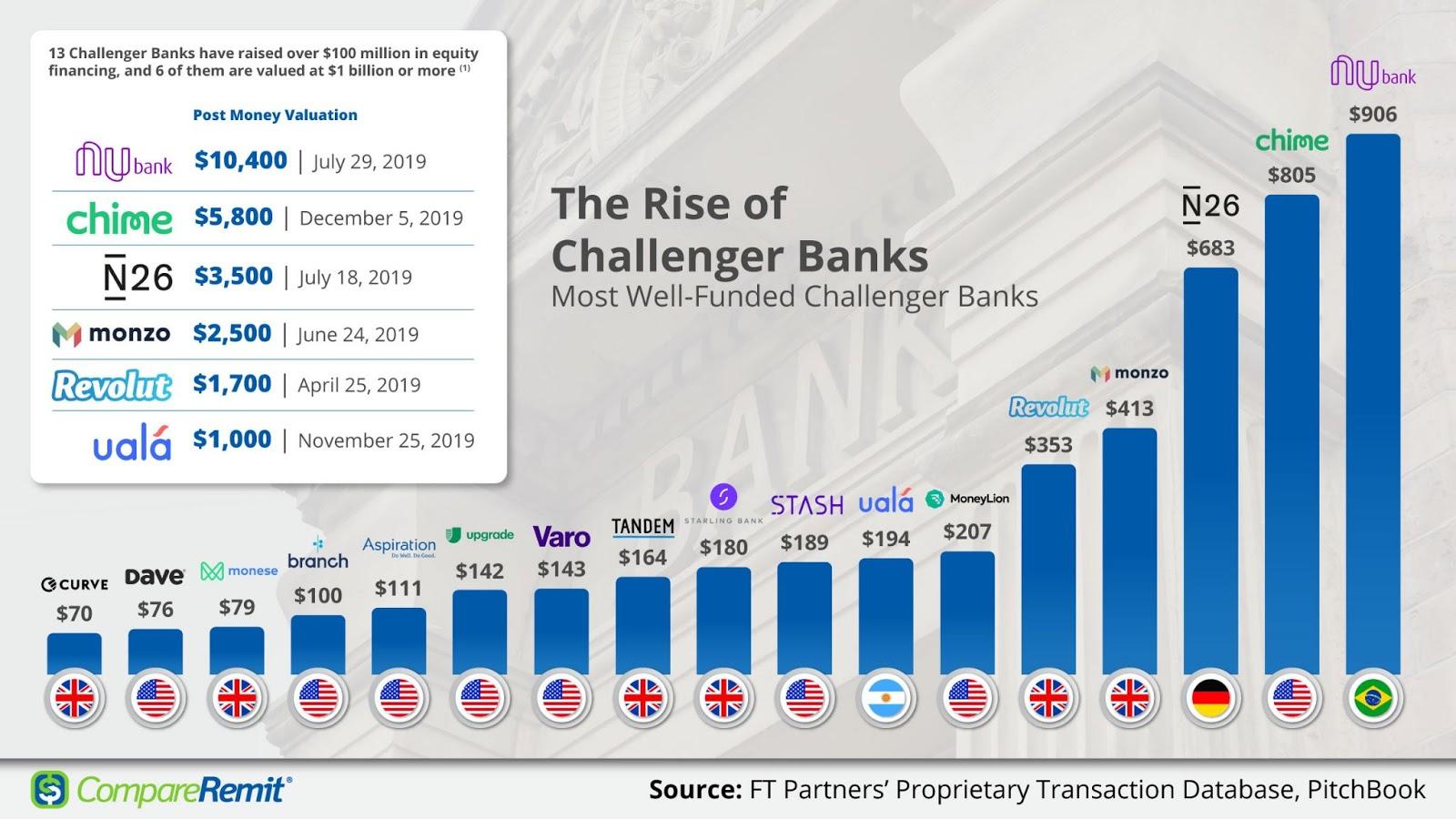

Neobanks are rapidly gaining popularity and have seen tremendous growth over the past few years, partly because of the increase in investments within the Fintech sector. According to a 2020 report by MEDICI Global, since 2018, a total of $5.627 billion has been invested, and in 2019, a record-breaking $4.361 billion have been poured into Neobanks.

Pitchbook, the PE/VC (Private Equity/ Venture Capital) data provider estimates that Neobanks will have 60 million customers in North America and Europe in 2020, and by 2024, it will reach over 145 million.

In the U.S., Chime is valued at $14.5 billion, becoming the most valuable U.S. consumer fintech with 12 million users.

With Neobanks, you have access to banking services at the convenience of your smartphone. Account opening is hassle-free and is done in minutes with minimal data requirements. Their added innovative features also allow you to manage your finances efficiently.

There is no differentiating line between national and international transactions with Neobanks. Unlike traditional banks, you don't need to upgrade your debit/credit card to transact internationally. Also, you get to save money on the cost of exchange rate on international transfers or purchases. For instance, Revolut doesn't charge any fees for currency exchange and their account accepts more than 100 different currencies.

However, it is worth noting that international money transfer function is not supported by most of the Neobanks as of now. Online money transfer companies offer the fastest and cheapest way to send money internationally.

International money transfer companies or cross-border payments service providers such as Remitly, Wise, Azimo, etc are integrating traditional banking services to their core services.

Since Neobanks operates digitally, there are no operational and labor costs of running physical branches. This affords them to charge little or no fees for basic services such as free ATM withdrawals. They are much more cost-effective due to fewer regulations and no credit risks.

User-friendliness is a priority for Neobanks. Their apps are highly responsive, clean, and crisp, and well-designed to cater to the needs of customers. The extremely user-friendly interface is a major plus point.

Neobanks are safe as they still have to abide by the regulators. They have some of the latest security features such as biometric verification, 2FA (2-factor authorization), RBAC (Role-Based Access Control), modern encryption technology among other security measures.

NeoBanks provide better reporting to customers on their accounts & finances helping them plan and manage their money more efficiently

They are relatively new to the financial market, have limited services, and have not had the time to come up with products and services you will get from traditional banks.

Traditional banks are stepping up to the challenges, investing in new technologies, and financial tools to stay relevant in the current scenario. In addition, people have established trust with incumbent banking institutions despite the slow and outdated processes. Potential customers may be hesitant to adopt it.

Since they lack brick-and-mortar branches, there is no in-person assistance when you are having difficulties with account-related issues. Neobanks may appeal to people who are tech-savvy and who grew up with internet access for almost everything.

The pandemic has been a catalyst for the digital transformation in the banking sector. Having said that, a lot remains to be seen when it comes to Neobanks. While traditional banks have largely preserved their position, this may be changing as challenger banks are gaining traction.

On a global scale, the growth of Neobanks is an upward trajectory. Thanks to their attractive value propositions such as low rates, personal finance management features, and ease of use, Neobanks will continue to attract customers and investors.

16244 views

16244 views