The year 2022 concluded with the Indian Rupee hitting an all-time low against the US Dollar. The COVID-19 pandemic significantly impacted global economies, leading to the devaluation of the Indian Rupee. Throughout the pandemic, the rate experienced a gradual decline in value, setting the stage for potential recovery in 2023.

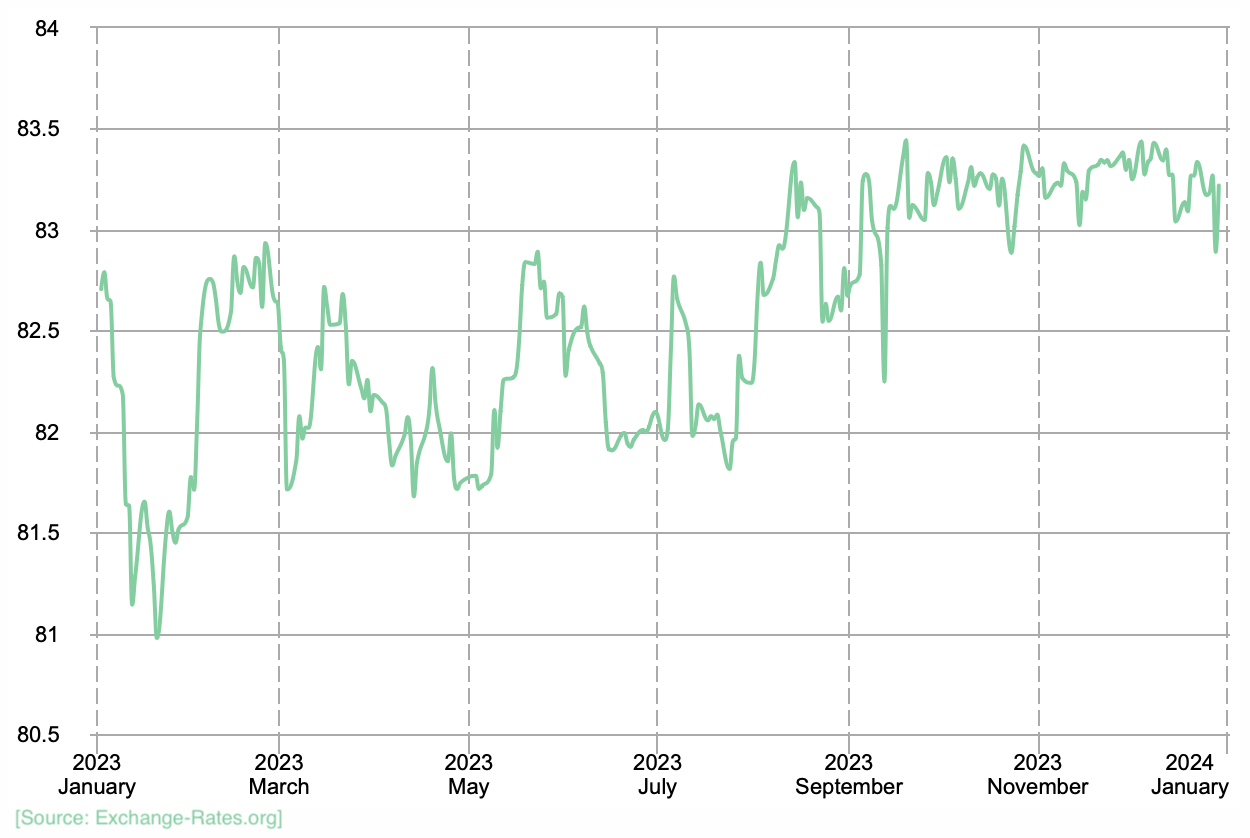

The US Dollar to Indian Rupee exchange rate did, in fact, see that recovery over the year’s performance. 2023 ended on a high, with the exchange rate averaging at $1 = ₹83.249 in December 2023.

As we are well into 2024, it is crucial to begin looking to the future and understand what the predictions for the year’s rates are. If you are planning to send money to India this year, this is particularly important as it will help you understand what is the best time to send your money and take advantage of an opportune rate.

Navigating the USD to INR exchange rate landscape requires understanding market dynamics and leveraging available resources to make informed decisions in 2024 and beyond. That is why we have accumulated expert forecasts and predictions all in one place for you. In this guide, we will be covering the Indian rupee's current outlook, what's driving the value of USD, the USD to INR forecast, and much more.

As we delve into the USD to INR forecast for 2024, let's rewind and understand the context.

2023 had an unpromising start, leaving many wondering whether the value of the Rupee was going to continue to decline despite the aftershocks of the pandemic having pretty much worn off. On January 20th, 2023, the USD to INR exchange rate reached its lowest point for the year. However, as the year progressed, 2023 witnessed a slow but steady increase in the exchange rate compared to 2022.

The USD/INR rate experienced a positive shift of +0.62% in 2023, indicating an increase in the value of the US Dollar against the Indian Rupee. The year's peak rate was recorded at 83.442 INR on September 19, 2023, with an average exchange rate of 1 US Dollar = 82.579 Indian Rupee for the year.

Various factors contributed to the strength of the USD against the INR and the subsequent exchange rate fluctuations. Economic indicators, such as GDP growth rates, inflation, and employment data, played a significant role. Additionally, geopolitical events, trade policies, and interest rate differentials between the US and India influenced investor sentiment and currency valuations.

Various factors contributed to the strength of the USD against the INR and the subsequent exchange rate fluctuations. Economic indicators, such as GDP growth rates, inflation, and employment data, played a significant role. Additionally, geopolitical events, trade policies, and interest rate differentials between the US and India influenced investor sentiment and currency valuations.

The aftermath of the pandemic boosted investor confidence in the robust US economy, while economic indicators, trade imbalances, and geopolitical events played their part in shaping the fluctuations of the USD to INR exchange rate in 2023.

Current market sentiment indicates a bullish outlook for the USD to INR exchange rate. That means the overall market-in favor of the United States-is expected to go higher, meaning that the value of the US Dollar is expected to increase.

The US Dollar is projected to experience a 1.64% rise in the next year, with the USD to INR rate anticipated to reach around ₹ 84.82. We have already begun to see the rate reach closer to that rate as the yearly average so far has been around ₹ 83.17.

[Source: Coincodex]

This is good news for those hoping to send money to India in 2024 as the rate leans more favorably for the US Dollar. It is, however, unfortunate news for those wanting to convert their Indian Rupee to travel to the United States, study in the USA, etc.

As we peer into the crystal ball for 2024, as stated before, the current sentiment in the USD to INR market is currently estimated to be bullish. The 14-day RSI reading is 53.64.

Forecasts suggest an upward trajectory for the USD to INR exchange rate in the coming months. Projections for the next six months indicate a potential 1.42% increase, bringing the exchange rate to ₹ 84.64.

Looking further into the future, as stated earlier, the one-year forecast anticipates a 1.64% rise, resulting in a rate of ₹ 84.82.

This all can be very overwhelming for those of us unfamiliar with how to navigate market fluctuations or even interpret terminology used by experts when discussing the exchange rate and market health. That is why we are providing you with a monthly breakdown with the predicted exchange rates for each month in 2024, that way you can make the best decision for when you would like to send money from the US to India or send money from India to the US.

The following INR USD forecasts are based on information that is currently available. Depending on the extent to which key factors, such as interest rates and central bank policy match market expectations, the forecasts could be changed and turn out to be false.

Please make sure to always conduct your own research and remember that future results don't depend on past performance.

Dollar to Rupee forecast February 2024: At the beginning 83.06 Rupees. At the end of the month 82.81, the change for February -0.3%. Maximum 84.07, minimum 81.53. The average exchange rate is 82.87.

Dollar to Rupee forecast March 2024: At the beginning 82.81 Rupees. At the end of the month 82.78, the change for March 0.0%. Maximum 84.02, minimum 81.31. The average exchange rate is 82.73.

Dollar to Rupee forecast April 2024: At the beginning 82.78 Rupees. At the end of the month 82.67, the change for April -0.1%. Maximum 83.91, minimum 81.43. The average exchange rate is 82.70.

Dollar to Rupee forecast May 2024: At the beginning 82.67 Rupees. At the end of the month 82.53, the change for May -0.2%. Maximum 83.77, minimum 81.29. The average exchange rate is 82.57.

Dollar to Rupee forecast June 2024: At the beginning 82.53 Rupees. At the end of the month 82.61, the change for June 0.1%. Maximum 83.85, minimum 81.37. The average exchange rate is 82.59.

Dollar to Rupee forecast July 2024: At the beginning 82.61 Rupees. At the end of the month 82.82, the change for July 0.3%. Maximum 84.06, minimum 81.58. The average exchange rate is 82.77.

Dollar to Rupee forecast August 2024: At the beginning 82.82 Rupees. At the end of the month 83.16, the change for August 0.4%. Maximum 84.41, minimum 81.91. The average exchange rate is 83.08.

Dollar to Rupee forecast September 2024: At the beginning 83.16 Rupees. At the end of the month 83.63, the change for September 0.6%. Maximum 84.88, minimum 82.38. The average exchange rate is 83.51.

Dollar to Rupee forecast October 2024: At the beginning 83.63 Rupees. At the end of the month 83.82, the change for October 0.2%. Maximum 85.08, minimum 82.56. The average exchange rate is 83.77.

Dollar to Rupee November 2024: At the beginning 83.82 Rupees. At the end of the month 83.20, the change for November -0.7%. Maximum 84.45, minimum 81.95. The average exchange rate is 83.36.

Dollar to Rupee December 2024: At the beginning 83.20 Rupees. At the end of the month 84.15, the change for December 1.1%. Maximum 85.41, minimum 82.89. The average exchange rate is 83.91.

For those looking to send money from the US to India in 2024, numerous options and companies offer highly competitive rates. Some even provide first-time rates higher than the economic USD to INR exchange rate.

Utilizing a comparison tool can help individuals find the best way to send money, ensuring they get the most favorable rates for their transactions. Use the CompareRemit comparison tool to find the best USD to INR exchange rate.

Compare and contrast the top money transfer companies on the market to find the best USD to INR exchange rate using our comparison tool.

Protip: Many companies offer a first-time user rate that is significantly better than their regular rate. Make sure you utilize those offers to get the best exchange rate that you can.

As the USD to INR forecast for 2024 unfolds, staying informed about currency dynamics is essential for making informed financial decisions. Whether conducting international transactions for business or personal purposes, understanding exchange rate trends and exploring efficient remittance methods empower individuals to navigate the currency landscape with confidence and foresight.

However, do keep in mind that the forecasts are often inaccurate and subject to correction. The USD to INR forecasts are based on the rate of inflation, central bank policies, and the health of the US and Indian economies.

Send money home to India today while the USD to INR exchange rate is in your favor! Compare rates and providers by using our online comparison tool.

135262 views

135262 views

.jpg?v=46)