.png)

Whether you're exploring new horizons or revisiting familiar destinations, the security of travel insurance can offer peace of mind. Interestingly, many credit cards provide various types of travel insurance, from trip cancellation to car rental loss and damage coverage, when you use your card to pay for travel expenses.

But do you really need additional travel insurance? While purchasing a separate policy can be wise, you may find that your credit card offers extensive travel insurance benefits, saving you the extra expense. However, not all credit card travel insurance is created equal. In this guide, we'll delve into the realm of credit card travel insurance to help you determine the best card for your specific needs.

Travel insurance is a protective measure designed to mitigate financial risks associated with travel-related incidents. It typically covers a range of unforeseen events such as trip cancellations, medical emergencies, lost baggage, flight delays, and more. By having travel insurance, travelers can embark on their journeys with peace of mind, knowing that they have financial protection in case of emergencies.

Before we explore the top credit cards offering travel insurance, it's essential to understand the various types of coverage your credit card may provide to protect your trip and yourself:

1. Baggage Delay: Imagine arriving at your destination only to find that your luggage hasn't made the journey with you. In such situations, your credit card's baggage delay coverage may reimburse you for the costs of purchasing new attire and essential items. The coverage amount and required delay period vary by card.

2. Lost/Damaged Baggage: If your bags are lost, damaged, or items are stolen from your luggage by a carrier, your credit card provider may offer monetary compensation to alleviate the financial burden.

3. Trip Delay: Delays in travel plans are not uncommon. If your trip on a common carrier is delayed, your credit card's trip delay coverage can help cover expenses such as meals, hotels, transportation, and necessary purchases up to a specified amount per ticket.

4. Trip Cancellation/Interruption: Unexpected circumstances may force you to cancel a prepaid, nonrefundable trip. In such cases, trip cancellation coverage can provide compensation to offset the lost funds. This benefit typically applies to cancellations for covered reasons, which vary by card.

5. Medical Treatment and Evacuation: Medical emergencies can occur while traveling. If you require medical treatment or evacuation due to injury or illness, your credit card's travel insurance may cover medical expenses up to a certain amount and the costs associated with returning home for care.

6. Travel Accident Insurance: In the unfortunate event of accidental death or dismemberment while traveling, your credit card may provide coverage to you or your beneficiary.

7. Rental Car Insurance: Renting a car? Your credit card's rental car insurance can offer protection against theft and damage to the rental vehicle. The coverage may be primary or secondary to your personal auto insurance, depending on the card.

Annual Fee: $550

Sign Up Bonus

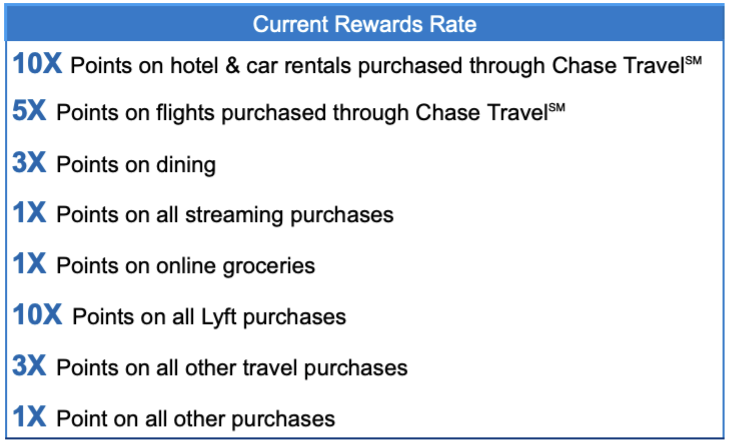

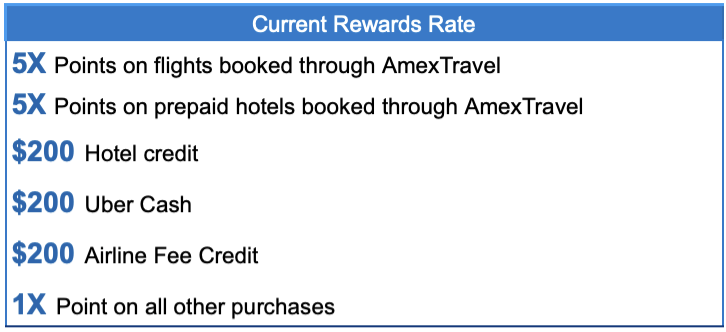

Chase Sapphire Reserve Card Rewards

Travel Insurance Coverage Details:

Annual Fee: $95

Sign Up Bonus

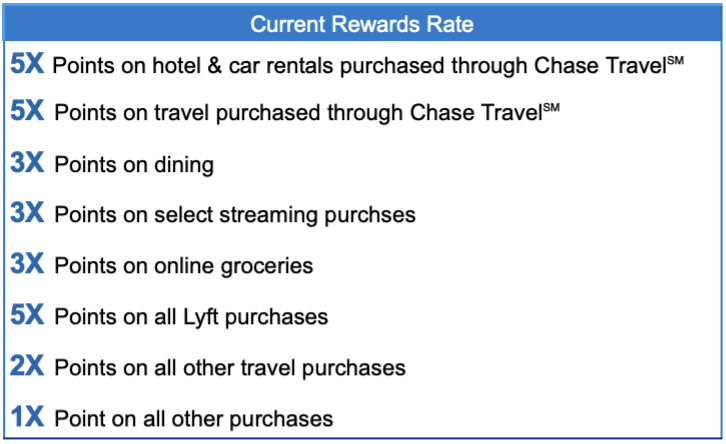

Chase Sapphire Preferred Card Rewards

Travel Insurance Coverage Details:

Annual Fee: $69

Sign Up Bonus

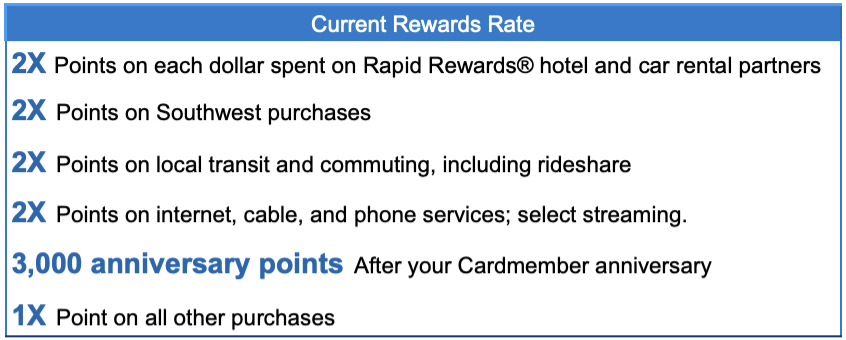

Southwest Rapid Rewards Plus Rewards

Travel Insurance Coverage Details:

Annual Fee: $695

Sign Up Bonus

Platinum Card Rewards

Travel Insurance Coverage Details:

Annual Fee: $95

Sign Up Bonus

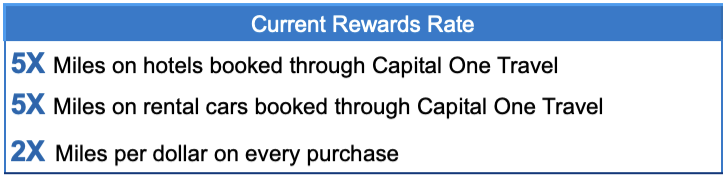

Capital One Venture Card Rewards

Travel Insurance Coverage Details:

Annual Fee: $0 intro annual fee for the first year, then $95

Sign Up Bonus

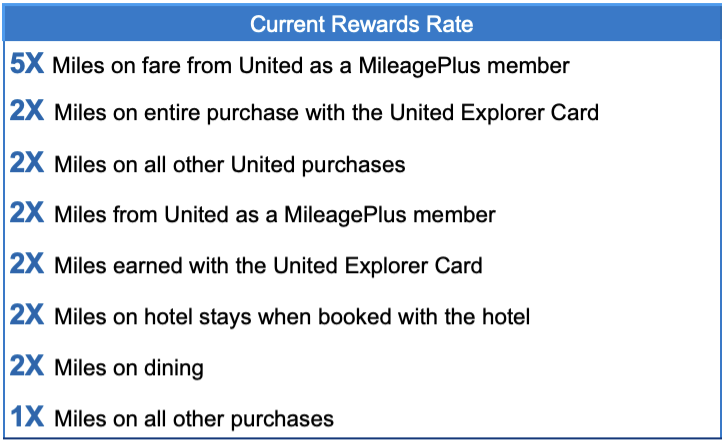

United Explorer Credit Card Rewards

Travel Insurance Coverage Details:

Choosing the perfect credit card for travel insurance involves careful consideration of various factors to ensure it aligns with your specific needs and preferences. Here's a comprehensive guide to help you navigate through the selection process:

1. Determine Your Desired Travel Insurance Benefits

Different credit cards offer varying levels of travel insurance benefits. Some may provide only basic coverage such as trip cancellation and interruption, while others include a broader range of benefits like trip delays, baggage delays, medical emergencies, and emergency evacuations. Assess your travel habits and requirements to determine which benefits are essential for you.

2. Evaluate Coverage Limits and Terms

Understanding the coverage limits, exclusions, and any requirements associated with the benefits is crucial. Pay attention to details such as pre-existing condition clauses, minimum spending thresholds to activate benefits, and the total trip cost covered. Also, consider the coverage for rental car insurance, ensuring it aligns with the types of rental cars you typically use.

3. Consider When Coverage Applies

It's important to note that having coverage doesn't guarantee its applicability in all situations. For instance, trip cancellation insurance may only permit cancellation for specific covered reasons. Similarly, rental car coverage may not include liability coverage, leaving you, as the driver, uninsured. Evaluate the circumstances under which coverage applies to ensure it meets your needs.

4. Assess Your Travel Habits

Take into account your travel patterns and preferences, including whether you travel domestically or internationally, the mode of transportation you use, and your accommodation preferences. This will help you prioritize the types of coverage that are most relevant to your travel style when comparing credit card options.

5. Consider the Annual Fee

Many credit cards offering robust travel insurance benefits come with an annual fee. Evaluate whether the benefits outweigh the card's annual fee based on your expected card usage and the value you'll receive from the travel insurance coverage. Additionally, consider any other perks or rewards associated with the card that may offset the fee.

6. Explore Additional Card Benefits

Aside from travel insurance, assess the card's other features such as travel rewards, airport lounge access, travel-related discounts, or concierge services. These additional perks can enhance your overall travel experience and provide added value, making the card more appealing.

7. Research Reviews and Recommendations

Read online reviews and seek recommendations from other travelers who have experience with the credit cards you're considering. Their insights can offer valuable perspectives on the reliability and quality of the travel insurance coverage provided by different cards.

How do I file a travel insurance claim with my credit card?

Is credit card travel insurance sufficient?

Does credit card travel insurance work?

While credit card travel insurance can offer valuable benefits, it won’t include everything. It is essential to ensure you have comprehensive coverage for your travels. The last thing you want is to be traveling and run into an emergency only to have to pay out of pocket at the end. Consider obtaining additional travel insurance through VisitorsCoverage to supplement your credit card coverage and ensure you're adequately protected against unforeseen circumstances. By being informed and prepared, you can enjoy worry-free and enjoyable travel experiences.

Remember, both travel insurance and sending money overseas require careful consideration and research to ensure a smooth and secure experience during your international journeys. If you're looking to send money overseas, compare exchange rates and choose a reliable money transfer service to maximize the amount received by your recipient.

For more information on travel insurance, visit VisitorsCoverage.com!

7127 views

7127 views

.jpg?v=46)