.jpg)

An Overseas Direct Investment (ODI) refers to investments made by a domestic firm in a foreign country to expand its operations.

From an Indian context, Overseas Direct Investment refers to investments outside India as a business strategy. ODI can be made in different forms depending on the company such as:

*ODI does not include portfolio investment.

Difference Between FDI and ODI

Foreign Direct Investment (FDI) is when a non-resident Indian invests in an Indian company. Outward Direct Investment (ODI) is when Indian resident companies invest in a wholly-owned subsidiary or a joint venture in a foreign country as part of a strategy to expand their business.

Routes of ODI From India

Direct investment outside India is governed by Foreign Exchange Management (Transfer or Issue of Any Foreign Security) Regulations, 2004, as amended from time to time. Overseas Investment from India can be made through two routes:

i) Automatic Route and

ii) Approval Route.

Under the Automatic Route, an Indian Party does not require any prior approval from the central bank, the Reserve Bank of India (RBI), for making overseas direct investments in a JV/WOS abroad. All those proposals not covered by the conditions under the automatic route require prior approval of the RBI.

Who Can Invest Through the ODI Route?

An Indian Party can make ODI under the Automatic route in any bonafide activity. However, Indian parties are prohibited from making investments or financial commitments in a foreign entity engaged in real estate or banking business without the prior approval of the RBI.

For the above restrictions, real estate means buying and selling of real estate or dealing in Transferable Development Rights (TDRs), not including the development of townships, construction of residential or commercial premises, roads, or bridges.

Guide on property related taxation and money transfer for NRIs

An Indian Party is also not permitted to invest in an overseas entity, which offers financial products linked to the Indian Rupee (such as non-deliverable trades involving foreign currency, stock indices linked to the Indian market, rupee exchange rates, etc.), and need prior approval from the RBI.

Who Is an Indian Party?

Indian Party encompasses:

When more than one such company, body, or entity invests the foreign JV/WOS, such combination will also constitute an "Indian Party."

Furthermore, the Indian Party should not be on the following list:

Also, all transactions relating to the investment in a JV/WOS should be routed through only one branch of an authorized dealer designated by the Indian Party.

Investment Limit of an Indian Party:

Indian Party can make ODI up to 400% of its net worth (paid-up capital and free reserves) as per its last audited balance sheet.

Any Financial Commitment (FC) exceeding USD 1 billion (or its equivalent) in a financial year would require prior approval of the RBI even when the total FC of the Indian Party is within the eligible limit under the automatic route (i.e., within 400% of the net worth as per the last audited balance sheet.

The prescribed limit will not be applicable if the investment is made out of balance held in the EEFC account (Exchange Earner's Foreign Currency Account) of the Indian Party or out of funds raised through the issue of ADRs/GDRs (American Depository Receipts/ Global Depository Receipts).

The total financial commitment of the Indian Party in all the JV/WOS comprise of the following:

* Investors need prior approval from RBI before transferring remittance beyond the limit prescribed for the financial commitment.

Can Resident Indians Make Investment Through ODI Route?

Resident Indians can make overseas investments, including purchase of securities and also setting up/acquisition of JV/WOS up to the limit prescribed by the RBI from time to time, per financial year under the Liberalised Remittance Scheme (LRS). Currently, LRS comes with a maximum cap of $250,000 a year per person.

Why Is the RBI Warning People About ODI Transfers?

RBI regulates ODI made by Indian entities and resident individuals in joint ventures and wholly-owned subsidiaries outside India pursuant to Foreign Exchange Management Regulations, 2004.

Recently, RBI has been sending queries and notices to several domestic entities, including companies and large family offices, seeking the status of unutilized money remitted abroad through the ODI route.

The remitted funds parked in foreign countries in financial assets including liquid funds by these firms could be a violation of ODI guidelines. Under the general permission, the remitted funds must be used for a specific business purpose. In this case, the firms would need to explain the retention of the remitted money in liquid funds.

As per the rule, any Indian Party that plans to make an ODI needs to approach a designated authorized dealer (AD) for investing along with duly signed ODI form, along with supporting documents like Board Resolution, Statutory Auditor Certificate, and many other documents to essentially satisfy the bonafide business test.

The investment can be processed once the AD Bank examines and approves the documents according to the regulatory guidelines. A Unique Identification Number (UNI) will be generated for the particular JV/WOS before the remittance. The UNI can be used for further remittances/ investments in the JV/WOS.

Mutual funds are another concern of RBI. Investment in mutual funds abroad is that only entities registered as non-banking financial companies (NBFC) can invest the outward remittances in foreign securities. This means funds transferred via the ODI route cannot be used for investments in mutual funds abroad.

Resident individuals can remit money outside India under the Liberalised Remittance Scheme (LRS) which has a maximum cap of $250,000 per year per person. The funds remitted under LRS can be used for investing in foreign securities, travel expenses, or sending money to Non-resident Indians (NRI) abroad.

The low limit under the LRS is allegedly making more individuals route the remittances through their family offices via the ODI route because the cap for an entity sending money through the ODI route is $1 billion per year or 400% of the net worth.

However, the ODI route is for large companies, corporates, or trusts that need to send large amounts of money out of India for business purposes. Sending money from India abroad through ODI to avoid the LRS limit is a violation of the ODI guidelines.

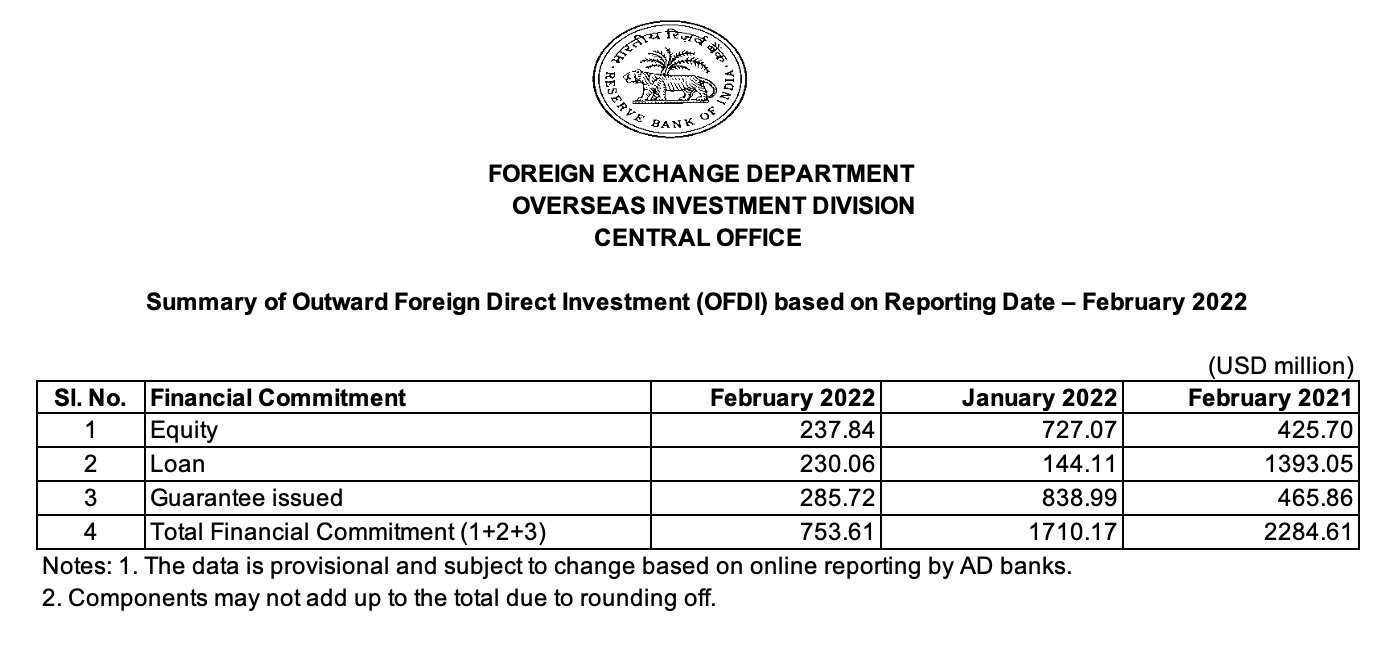

ODI From India Dips 68% To USD 754 Million in February 2022

ODI is also called outward foreign direct investment or direct investment abroad. The appetite for foreign investment was picking up and many Indian investors and companies were investing/acquiring stakes in numerous foreign companies.

However, following the restrictions by the RBI, coupled with the global economic crisis, investments have dropped. According to the RBI data on Outward Foreign Direct Investment, investment for the month of February 2022 (USD 753.61 Million) has dropped by 68% compared to February 2021 (USD 2284.61 Million).

*RBI said the data is provisional and is subject to change based on reporting by banks.

An increase in ODI can also be seen as a sign of a country's investment competitiveness, higher growth prospects in foreign markets, and a maturing domestic economy.

The Covid-19 pandemic has been widely cited as one of the reasons for not utilizing the money sent through the ODI route. Several deals didn't get through due to the second wave of Covid and people didn't want to lose interest in the money, hence have invested in products like liquid funds abroad. And maybe awaiting the right business opportunity to invest the money.

In conclusion, for ODI-related investment opportunities, we recommend consulting with a tax advisor. To keep yourself abreast with the latest guidelines pertaining to ODI, the Reserve Bank of India has issued detailed guidelines vide Notification No. FEMA 120/RB-2004 dated July 7, 2004, as amended from time to time, which can be accessed at RBI's website.

A Master Direction that has consolidated instructions on rules and regulations framed by the Reserve Bank under various Acts including banking issues and foreign exchange transactions and is available at the 'Notification' Section on RBI's website.

23670 views

23670 views