.png)

If you have ever transferred money internationally or received funds from abroad, you have likely come across the term IBAN. You may have wondered, what is an IBAN number and why is it important. This guide offers clear answers.

Here, you will find everything you need to know about IBANs, including what it is, how to find your IBAN, why they exist, and how they differ from a SWIFT code.

IBAN stands for International Bank Account Number. It is a standardized format used to identify bank accounts across countries. The purpose of an IBAN is to ensure that international transactions are processed accurately and efficiently, minimizing delays and errors.

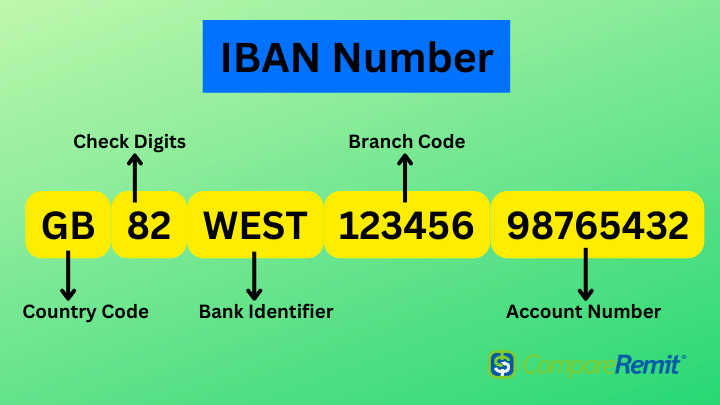

An IBAN can contain up to 34 alphanumeric characters. Its structure typically includes:

IBAN numbers from different countries look like this:

Besides the International Bank Account Number, there are two other money transfer codes you should know about:

Since an IBAN is often required for international money transfer, it's helpful to know how to locate yours. Here are four common ways to find it:

IBAN stands for International Bank Account Number, whereas SWIFT stands for Society for Worldwide Interbank Financial Telecommunications. While they both are used for international money transfers, they serve different purposes.

| Feature | IBAN Number | SWIFT Code |

| Purpose | Identifies individual bank accounts | Identifies banks and financial institutions |

| Characters | Up to 34 | 8–11 |

| Used in | 70+ countries | Globally |

| Example | GB82WEST12345698765432 | CHASUS33XXX |

Pro tip: When sharing your IBAN for receiving payments, always include the full international format along with your bank’s SWIFT code if required. This ensures smoother and faster processing of global transfers.

When making an international transfer, you will typically need the IBAN of the recipient, their bank name, and sometimes the SWIFT code of their bank. Here's how the process works:

If you enter the wrong IBAN, it can cause delays, failed transactions, or—in rare cases—misdirected funds. Always double-check it before sending the money.

All countries have a SWIFT code, not an IBAN number. While the system is adopted in more than 70 countries, some countries rely on an alternative format.

Understanding the IBAN meaning can help ensure that international money transfers are accurate, smooth, and secure. Using the correct IBAN helps avoid transaction delays, processing errors, and unnecessary fees. While IBANs ensure your payment reaches the right account, it's also vital to choose a reliable online money transfer service provider for the best exchange rates and lower transfer costs.

Before sending money overseas, always double-check the recipient’s IBAN and compare transfer services to get the most value for your money. If you want to save on fees and get the best exchange rates, CompareRemit makes it easy to compare money transfer providers in real time.

Whether you're sending funds to family, making business payments, or paying for overseas expenses, using the correct details—including the IBAN—can make the entire process smoother.

An IBAN can be up to 34 characters long and includes both letters and numbers. The exact length varies depending on the country.

It is not possible to directly get a SWIFT code from an IBAN. These are distinct codes serving different purposes. You will need to find the SWIFT code separately—either from your bank's website, account statements, or by contacting your bank directly.

If you enter the wrong IBAN, the transaction may be delayed or canceled. In rare cases, it could even result in your money being sent to the wrong bank account.

International transfers using an IBAN typically take 1–5 business days to process. The exact timing depends on factors such as intermediary banks involved, your bank's daily cutoff times for processing transactions, and the efficiency of the recipient's banking system.

While you cannot create multiple IBANs for a single bank account (since each IBAN is a unique identifier for one specific account), many banks now offer multi-currency accounts. These accounts allow you to send and receive different currencies through a single IBAN.

Yes, you can use your IBAN to receive money from abroad. The IBAN ensures that funds are accurately sent to the correct account.

42727 views

42727 views

.jpg?v=46)