Welcome to our comprehensive review and guide of Panda Remit, your go-to solution for seamless and secure international money transfers.

In today's interconnected world, where distances are bridged by digital technology, finding a reliable remittance service is essential. Panda Remit has emerged as a frontrunner in this competitive landscape, offering users a user-friendly platform, competitive exchange rates, and a robust security framework.

In this detailed article, we will delve deep into the features, pros and cons, fees, security measures, and step-by-step instructions, providing you with a complete roadmap to navigate your financial transactions effortlessly.

Whether you're sending money to family overseas or managing international business payments, join us on this exploration of Panda Remit, unlocking the full potential of cross-border money transfers.

Panda Remit, also referred to as Wo Transfer, is a digital platform that enables individuals and businesses to send and receive money internationally.

With a focus on simplicity, transparency, and cost-effectiveness, Panda Remit aims to provide users with a hassle-free experience when sending money across borders. The service prides itself on competitive exchange rates, low fees, and fast transaction processing times, making it an attractive option for individuals and businesses alike.

Panda Remit sports a long list of countries that you can transfer your funds to.

Countries serviced by Panda Remit include:

To view a complete list of countries that Panda Remit serves, navigate to the home page. There you will find the money transfer calculation tool. Select the drop down menu for the receiving country and you will be shown all the countries you can send money to!

Panda Remit charges a small fee for each transfer, which varies depending on where you are sending the money from. For example, for a transfer made from the United States, Panda Remit charges a $6.99 fee. After that, there is no additional handling or processing fee.

Panda Remit offers an exclusive offer for new customers, zero transfer fees on your first transfer (as of October 16, 2023).

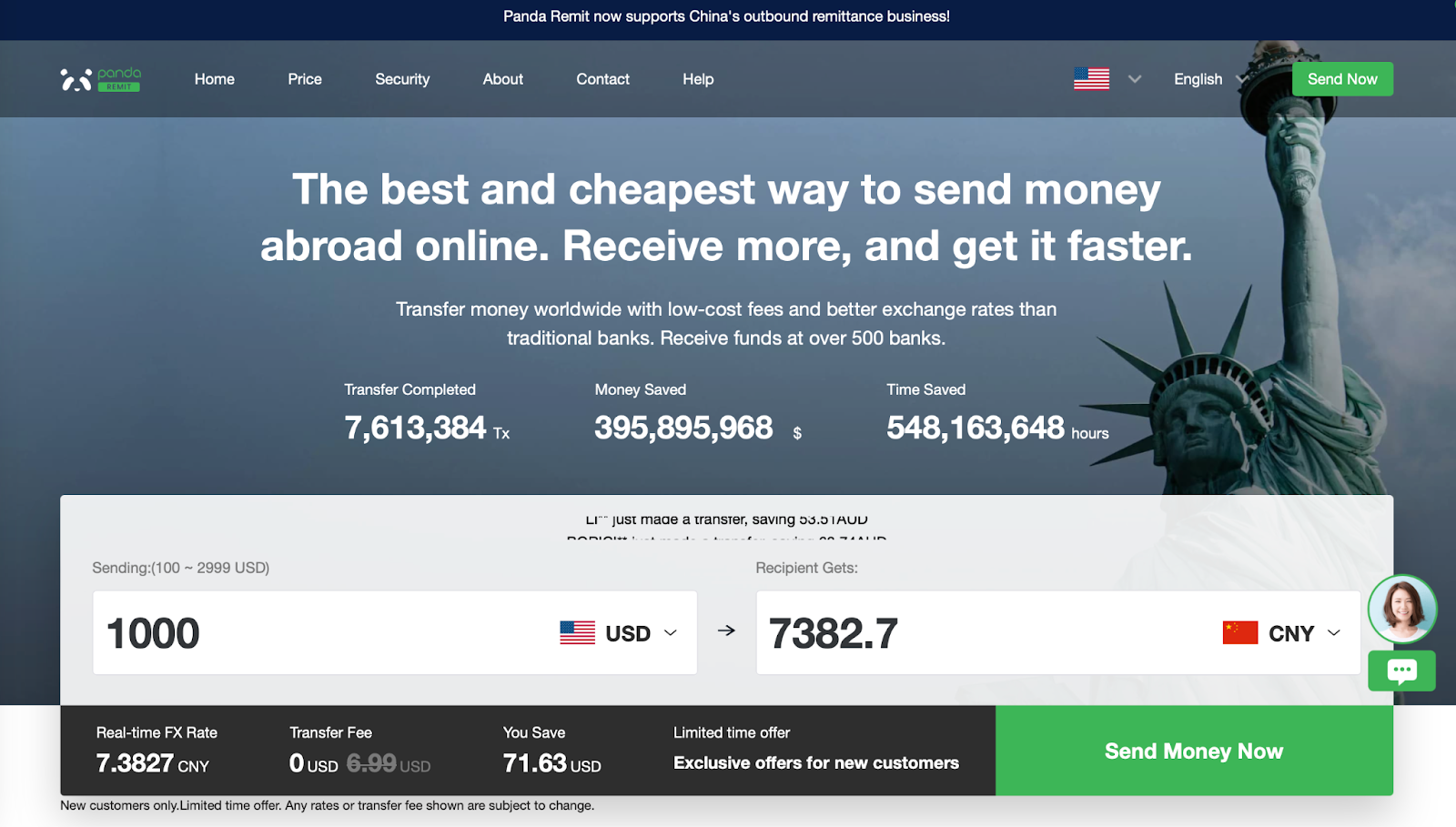

Their competitive exchange rate is displayed on their money transfer calculation tool. Once you enter the basic details of your transfer (where you are transferring money from, where you are transferring money to, and how much you want to transfer) then you will be taken to a breakdown of what your exchange rate will be and how much money your transfer recipient will receive.

Panda Remit doesn't set any limits on how much you can send or how often you can send it, but they do have to follow local rules. Sometimes, they might need some extra info from you, like where the money is coming from or how you're connected to the person you're sending it to. They do this to make sure everything runs smoothly and that you're protected and following the rules.

For example, if you're in China, the government says you can get up to $50,000 USD in remittances each year. But, when you're converting that to Chinese currency (RMB), it needs to match your yearly quota. If there are any questions, Panda Remit's customer service team is always ready to help through WeChat or email. They're quick, friendly, and happy to assist.

When it comes to sending money with Panda Remit, speed is the name of the game. While the exact time it takes can depend on a few things, like where you're sending the money and how you're paying, Panda Remit is all about making it quick and hassle-free.

In most cases, transfers through Panda Remit happen within a few business days if not within minutes, which is pretty impressive if you're in a hurry to get your money where it needs to go. Of course, like with any financial transaction, there might be some factors that influence the timing, such as the specific banks involved and the verification processes.

But fear not, Panda Remit is committed to getting your funds to the right place as swiftly as possible. For the most accurate estimate based on your unique situation, it's always a good idea to reach out directly to check their website or try to initiate a transfer on your own. They can give you the lowdown on exactly how long your transfer might take, ensuring your money reaches its destination in no time.

You might be wondering, is Panda Remit reliable? Don’t worry! Panda Remit, prioritizes the safety and security of its users' financial transactions.

Panda Remit employs encryption techniques and secure communication protocols to protect user data from unauthorized access during transmission.

The service operates within the legal frameworks of the countries it serves. It adheres to local and international regulations, ensuring compliance with anti-money laundering (AML) and know your customer (KYC) requirements.

Remember, while Panda Remit may be safe, always be cautious about phishing attempts. Ensure you're on the official website and never share sensitive information via email or unfamiliar communication channels.

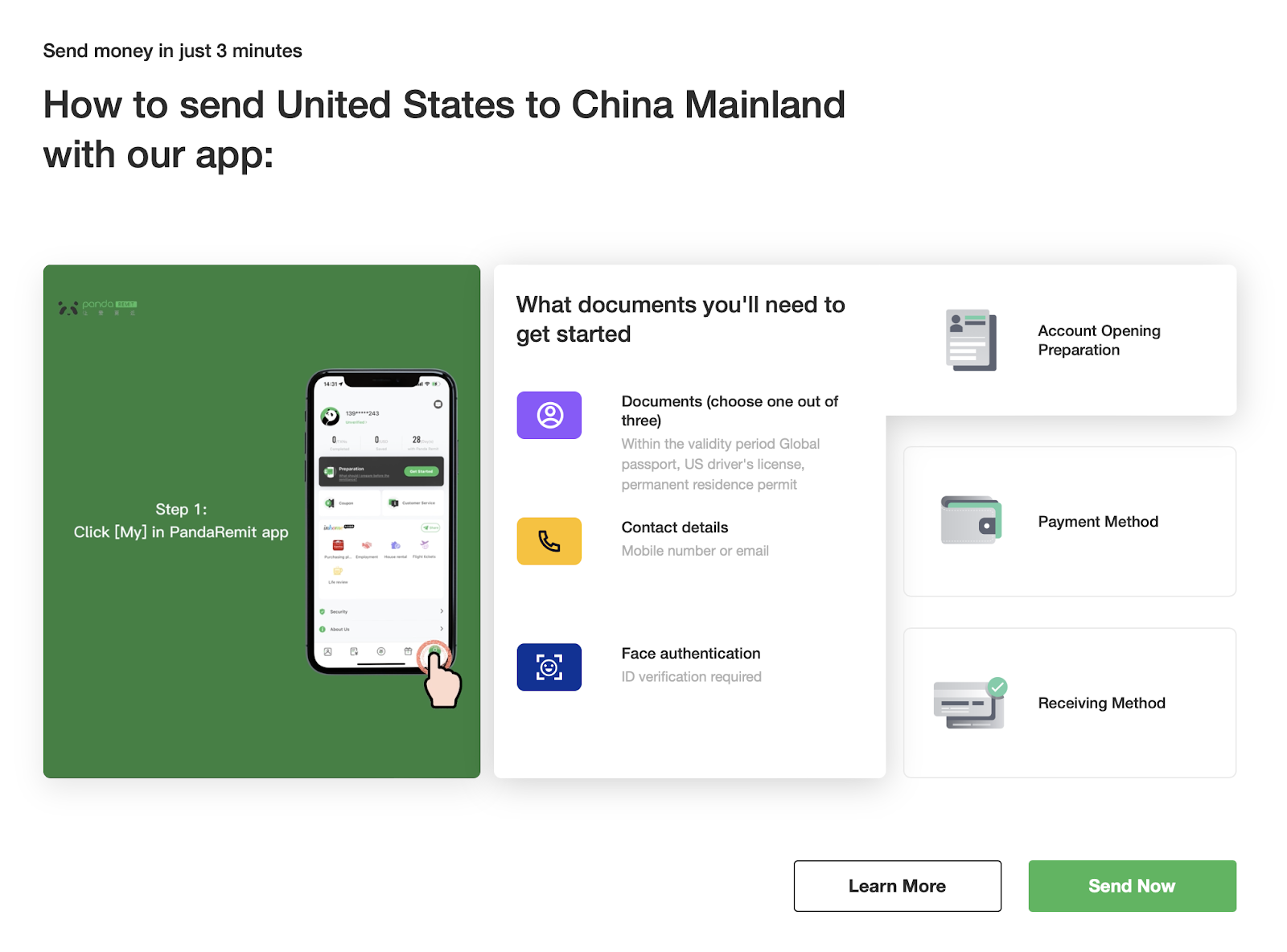

Now for the biggest question you must have: how does Panda Remit work?

Luckily, using Panda Remit for your international money transfers is relatively straightforward. Here's a step-by-step guide:

Panda Remit offers various ways to contact their customer support team for assistance or inquiries.

Panda Remit has a comprehensive help center or FAQ section on their website. This resource can provide answers to many common questions and guide you through various aspects of using their service.

Still can’t find the answer to your question? Visit the Contact Page on the Panda Remit website.

There you can find the different customer service numbers for Panda Remit:

You can also reach out to Panda Remit through their customer service email: [email protected]. Or you can submit the email

Another way to reach out to Panda Remit is to chat with them. Scan the QR from the image below or from the “Contact” page.

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Panda Remit money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Panda Remit service are:

Panda Remit's standout feature lies in its innovative and user-friendly money comparison tool prominently featured on their homepage. This tool simplifies the money transfer process by allowing users to input essential details – the origin and destination of their transfer and the amount – and instantly generates a transparent breakdown of the transaction. What sets Panda Remit apart is its commitment to transparency; the tool not only displays the exchange rate but also meticulously outlines any special offers and associated fees.

It's a game-changer for those seeking clarity and confidence in their international money transfers, making Panda Remit a trustworthy choice for users worldwide.

If you’re looking for an alternative to Panda Remit’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Panda Remit? Let’s see what users of Panda Remit have to say. Sourced from multiple platforms, customer reviews of Panda Remit are:

Panda Remit scores a “Great” rating on TrustPilot with a TrustScore of 4.0 out of 5.

“Remittance was completed in less than 2min from SG to Msia. With the locked in rate feature, you can get the best rate within the day. A smooth transaction with zero fee charge as they advertised for the first timer, working well for my experience.” - Celine Toh on TrustPilot

“I have been using Panda remit for 1 year and totally abandoned other app after I got much higher rate on Panda remit.” -Reviewer on Apple Store

“Best rates, money always transfers successfully. But it's a very weird app. Unlike other apps/websites, it does not send you email confirmations, does not even ask you to enter account number twice for security, does not send you any kind of notifications. Some of the content on the app is very poor English, which makes you feel like it's a fake app/scam. But, it's legit. Did several transactions and all were successfully sent in around 3 business days. Gives the best rates on the market.” - Reviewer on Google Play

Negative reviews pertain to issues with the first time offer, identity verification, and transfer delays.

To see even more trusted reviews from users of Panda Remit, check out CompareRemit’s review page.

With its user-friendly interface and competitive rates, Panda Remit offers a compelling solution for individuals and businesses needing to transfer funds across borders. While availability and payment options might be limited in some regions, its overall advantages make it a viable choice for many users.

In conclusion, if you are looking for a reliable, cost-effective, and efficient way to send money internationally, Panda Remit (Wo Transfer) could be the solution you’ve been searching for. With its commitment to user satisfaction and secure transactions, it provides a seamless experience for all your cross-border financial needs.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

16559 views

16559 views