Wise, formerly known as TransferWise, has revolutionized international money transfers with its transparent and cost-effective approach, making it a top choice for individuals and businesses alike. With it's mission to eventually make online money transfers completely free, Wise is paving the way for affordable and accessible remittance worldwide.

Let's take a look at how Wise has simplified cross-border transactions empowered users to send and receive money with utmost ease and confidence. Whether you're a seasoned Wise user or a curious newcomer seeking a reliable remittance solution, we've got you covered with all the essential information you need to know about this exceptional service.

In this comprehensive Wise review, we take a deeper dive into the Wise online money transfer service and determine if it is the best option for sending money overseas.

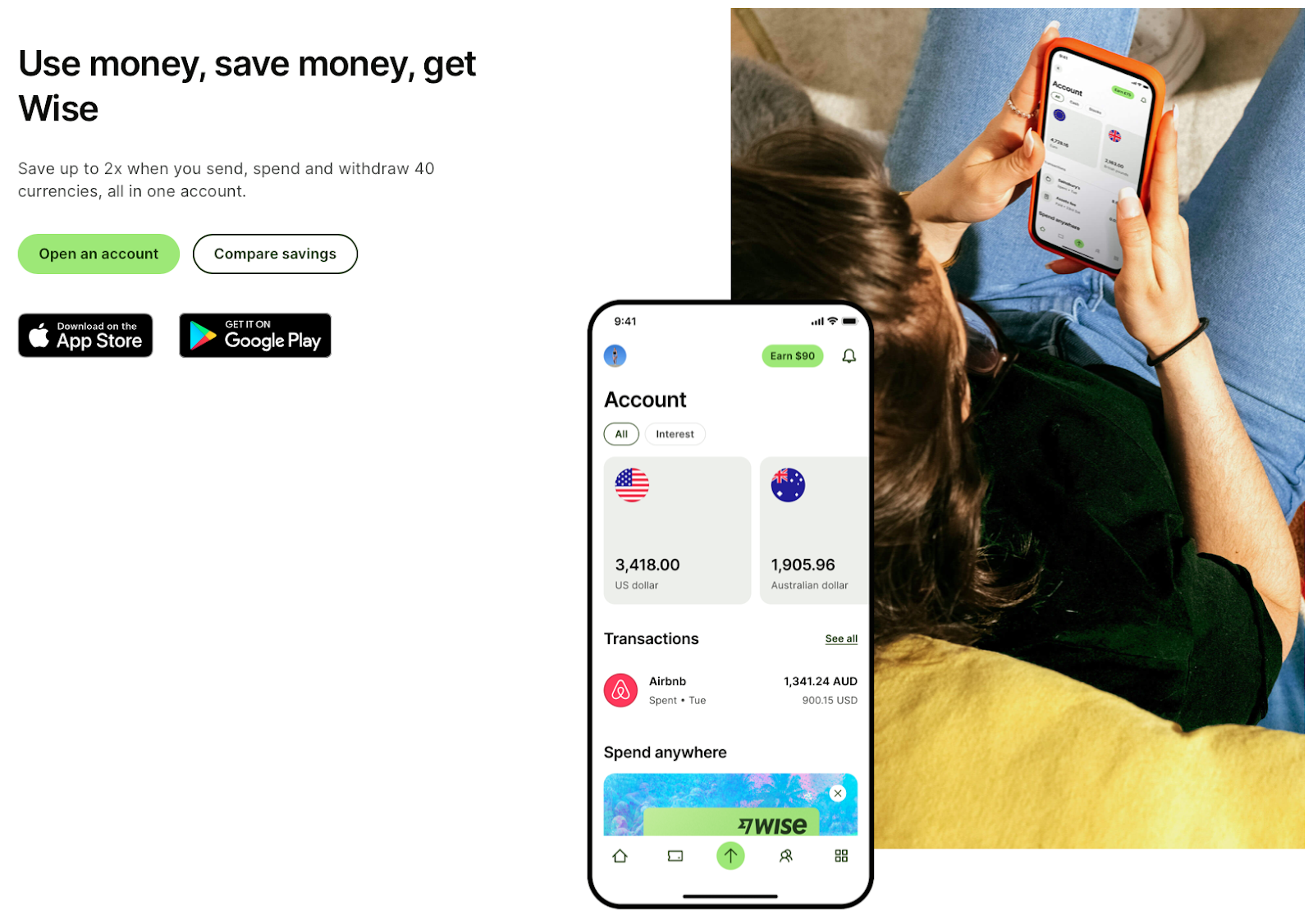

Wise, formerly TransferWise, is an online, international remittance service, “built to save you money and time.” Wise offers both domestic and international money transfer out of the United States and serves 160 countries and 40 currencies. To send money with Wise, you will need to simply create a free online account. Once you have secured your Wise login, you can begin the money transfer process through Wise.com or the Wise mobile application.

Countries supported by Wise Money Transfer include:

You can find a comprehensive list of the countries Wise serves on the bottom of the Wise homepage.

Sending money domestically with Wise is completely free; just make sure you have a balance opened up first. The recipient of a domestic transfer will need to pay a cost of 4.14 USD per domestic transaction.

To transfer money internationally, Wise charges a small fee of 4.25 USD + 0.61% of the amount that's converted per transaction. The recipient of the funds pays no fees. There is no required fee to create an account nor to maintain it.

Wise money transfer fees can vary based on transaction type - some transfer types charge different fees than others. There are also limits per country of how much you can send in a single transaction.

There is no minimum amount of money you can send internationally or domestically through Wise. There are, however, limitations imposed on the maximum you can send on some transfers, varying by country.

Wise does have a maximum amount of money that is permitted to transfer and receive. There is a daily limit of 20,000,000 USD and annual maximum of 35,000,000 USD.

While most transactions are completed within 24 hours, some even taking mere seconds, it can take up to five days to send and receive money through Wise, depending on the currency being transferred.

If you want a more exact estimate of how long your transfer will take before you commit to the process, you can visit their transfer calculation tool, enter vague details of the amount you wish to transfer and the destination for that amount, and scroll down to view the estimation provided by Wise.

Now for the biggest question you must have: how does Wise work?

Sending money with Wise requires you to first create an account. The account is free; you can register with your email and chosen password or simply sign in with your Google or Facebook account.

Before you begin the official process, you can use the transfer calculation tool to see a tentative estimation of the transfer cost, how much you will save, how much your recipient will receive, and how long the transfer will take.

Once you have an account created, follow these steps to set up your first remittance transaction.

Wise money transfer is a FinCEN registered service and one that is trusted by 15+ banks internationally, both ensuring that safe and trustworthy practices are used by the company. Wise employs around-the-clock fraud prevention systems, advanced data protection, and two-factor authentication to protect their customer’s account and transfers.

Wise has a thorough Help Centre catered to answering any queries you may have. Another great help service Wise provides is that, once you have begun a transfer and have questions, you can visit the Help Centre to receive personalized help catered to your transfer’s issue.

If your questions are still not answered, don’t worry, Wise has a phone line that you can reach out to:

1 (888) 908-3833

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Wise money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Wise service are:

As mentioned before, Wise introduces their money transfer calculation tool before you have even set up an account. This allows the user to check the tentative details of their planned transfer without the commitment of having to create an account and entering bank account details. Then, you can begin the process from right there by simply clicking “Get started.”

If you’re looking for an alternative to Wise’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Wise? Let’s see what users of Wise have to say. Sourced from multiple platforms, customer reviews of Wise are:

Wise scores high on TrustPilot with a TrustScore of 4.4 out of 5.

“Wise is convenient, well priced and secure,” - John C. on TrustPilot

“Yes- Wise is excellent service. The login info goes to "Plaid" I think which is a service used by many banks to connect accounts. You can look it up but I believe it is supposed to be pretty secure.” - user on Reddit

“I now have the app alongside web based access so logging on is a secure but easy process. I am trialling placing my money in the interest account. So far, a very positive experience” - James on TrustPilot

Negative reviews pertain to identity verification, bank verification, transfer delays, and account suspension frustrations.

The simple process allows for Wise to be a very convenient option for beginners, those seeking a service with a larger and diverse list of countries they serve, and those looking to transfer money quickly and hassle free.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

27293 views

27293 views