Instarem is an awarding winning remittance company that is focused on transforming the way people send money overseas by making the process easy and affordable for all. This leading money transfer service has revolutionized the way people send funds across borders with an easy-to-use platform, upfront low costs, and quick turnaround time. Instarem's focus on cost-effectiveness and reliability has earned it a loyal clientele and a stellar reputation within the industry.

In this Instarem review, we will explore the main features, benefits and possible drawbacks of Instarem to help you make an informed choice when considering their platform as a solution for your international remittance requirements.

Let’s take a closer look at the Instarem remittance service and whether or not it is a preferred choice for sending money overseas online in this comprehensive Instarem money transfer review.

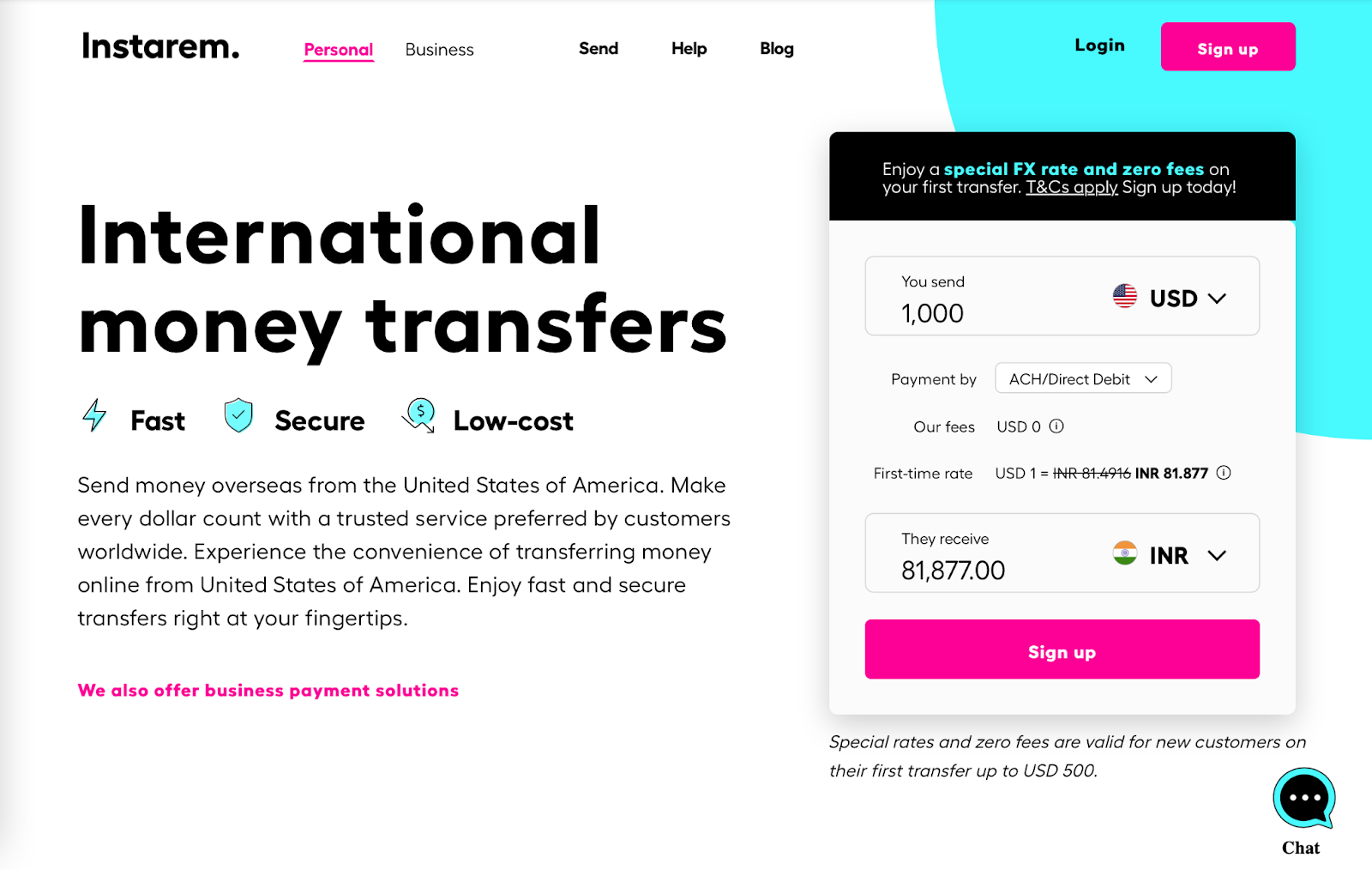

Instarem is an online, international money transfer service that allows users to send money overseas from the U.S. Instarem strongly believes in their model to use, “smarter, faster, and more reliable,” technology to, “make money simple for everyone.” They have offices located in 11 countries around the globe, and they serve over 60 countries. To send money with Instarem, you simply need to create an account and begin your money transfer process.

Instarem also has a unique system of referral codes, where you can earn rewards by referring others and entering the referral code upon signing up to earn points for yourself and the new account holder you referred.

Once you have secured your Instarem login, you can begin the money transfer process through Instarem.com or the Instarem app.

Countries supported by Instarem Money Transfer include:

You can find a comprehensive list of the countries Instarem serves by scrolling on the Instarem Send Money page.

Instarem calculates your transfer fee by adding a markup to the mid-market-rate. Calculating what the fee would look like for you will be tricky to do on your own. You can look up what the current mid-market-rate is on Google or use a currency converter. Once your Instarem login is secured, you can see in better detail how much your fees will be based on your individual transaction, since the total fee is determined from your transfer amount.

But what if you want to understand what your fee will look like before you commit to creating a login? Don’t worry, Instarem has a solution. Simply use their money transfer calculation tool, enter some basic information about your intended transfer, and get an estimation of what the transfer will cost and convert to.

Instarem does not charge a fee for keeping your account. Creating and maintaining your account is free.

Instarem’s minimum and maximum transfer amount varies based on which country you intend to transfer the money to. In a very clearly constructed chart, Instarem lays out all the details of the various limits, organized by country on their website. This chart also outlines the various payment methods available for each country and the maximum amount allowed for each payment method so you can decide for yourself, whichever option is best for you.

While it is important for us to highlight that each transfer is unique and their transfer times are dependent on the amount and destination country, Instarem prides itself on its speedy money transfer. Because of its global banking network, Instarem aims to complete your transfer within 1-2 business days, a very speedy transfer time in comparison to many services in the market.

Once you log in and begin your transfer process, Instarem will provide you with a more solidified deadline for your transfer. If you have the Instarem app, you will even be able to track your money transfer right at the click of your finger.

Instarem money transfer is licenced across all the countries it operates in and serves. It is licensed and regulated by financial authorities in different countries, including the Monetary Authority of Singapore (MAS), the Reserve Bank of India (RBI), Bank Negara Malaysia (BNM), Australian Transaction Reports and Analysis Centre (AUSTRAC), the Financial Conduct Authority (FCA) in the UK, and the Financial Crimes Enforcement Network (FinCEN) in the US.

Instarem employs the use of advanced encryption technology to protect your sensitive information and keep your transactions secure.

Now for the biggest question you must have: how does Instarem work?

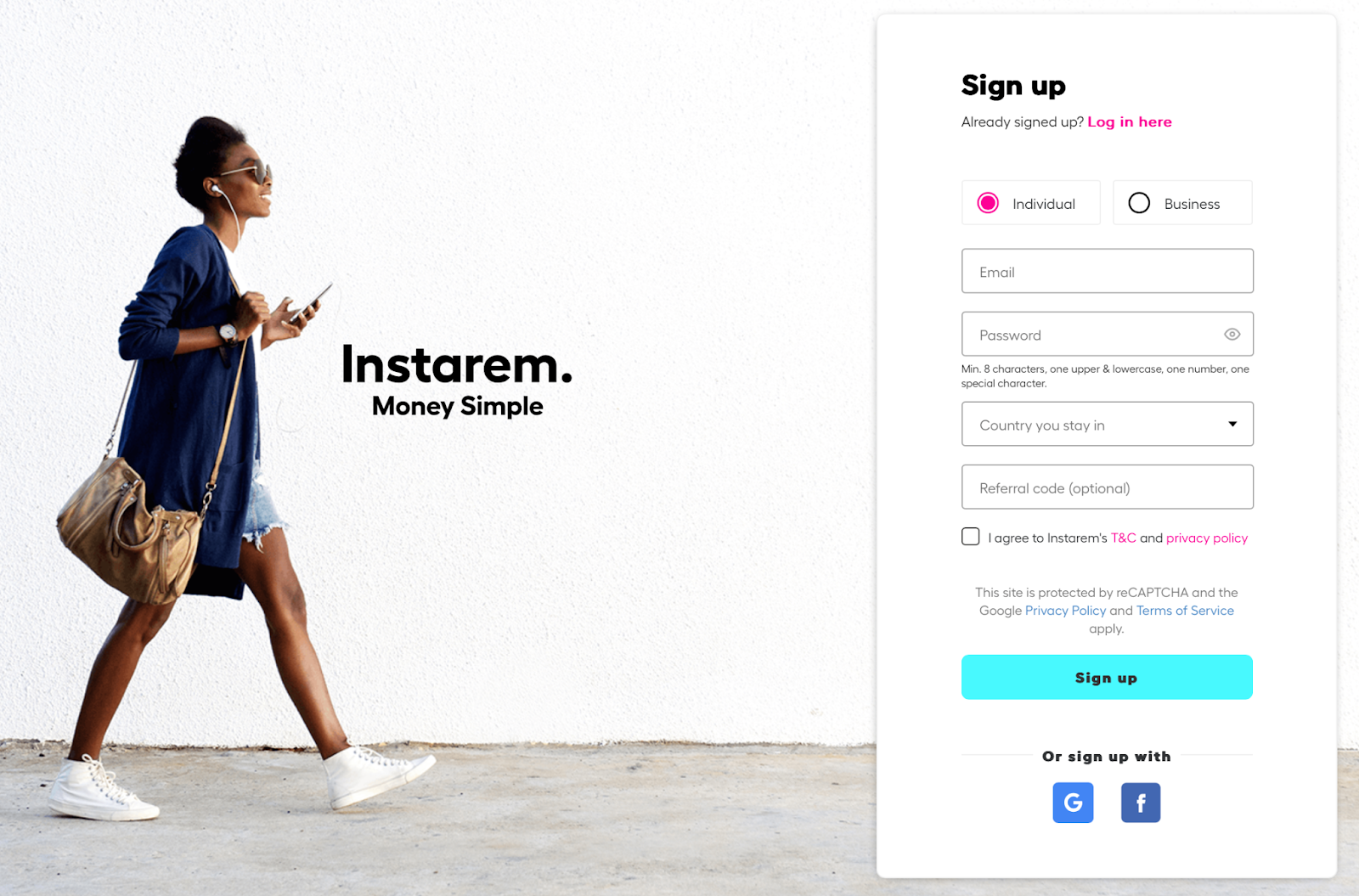

Sending money with Instarem requires you to first create an account. The account is free; you can register with your email and chosen password or simply sign in with your Google or Facebook account.

Before you begin the official process, you can use the money transfer calculation tool to see a tentative estimation of the transfer cost and how much your recipient will receive.

While creating your account, you will be asked to provide the following information:

Once you have an account created, follow these detailed steps to set up your first remittance transaction.

After the transfer has been completed, you are eligible to receive points that can be applied to future money transfers.

Instarem has an extensive FAQ and Help Centre for their customers to have all of their questions answered. To receive more active help, you can chat with their 24/7 chatbot in the “Help” tab on the main page.

You can also login to your Instarem account and send a query to ask more personalized questions.

Finally, if you still have questions or feel that your query is still unanswered:

You can send an email to [email protected]. Be sure to include the information below so Instarem can successfully assist you:

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Instarem money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Instarem service are:

As mentioned before, Instarem has a very well-set-up and easy-to-understand point system, allowing customers to save money on their future transfers. Each transfer earns points, meaning you can start saving money right away. This stands out as a stellar feature, especially for those transferring money frequently.

If you’re looking for an alternative to Instarem’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Instarem? Let’s see what users of Instarem have to say. Sourced from multiple platforms, customer reviews of Instarem are:

Instarem scores high on TrustPilot with a TrustScore of 4.5 out of 5.

“The transfer was easy, quick with absolutely no hassle. It was almost instantaneous! I had used the app for the transfer and the amount reached my India account in a matter of just a few minutes!” - Gaurav on TrustPilot

“Instarem is a good money transfer provider, easy enough to use and placing a great deal of importance on security.” - Mehdi Punjwani on MoneyTransfers.com

“Smooth, efficient and reliable. Used Instarem 3 times now and had no issues. Transfers get delivered within the day. The first transfer may take longer due to bank approving new payee. The other great thing is that the rate you agree to when you start the transaction doesn't change :)” - Jo Youssef on Google

Negative reviews pertain to identity verification, bank verification, transfer delays, and account suspension frustrations.

The simple process allows for Instarem to be a very convenient option for beginners, especially those looking for a service they can commit to and use multiple times. The InstaPoint system makes Instarem a great option to choose if you are looking to save money across multiple transfers.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

9576 views

9576 views