Money transfers aren’t always a simple process. Money transfer services have become an integral part of our lives, offering convenience and efficiency. But it can be tricky to find the right service for you. Paysend, a prominent player in the money transfer industry, has gained widespread attention for its user-friendly interface, competitive rates, and secure transactions. This comprehensive review and guide will delve into the features, benefits, and step-by-step process of using Paysend for your money transfer needs.

Paysend is a global money transfer platform that enables users to send money to over 70 countries worldwide. With a focus on simplicity and speed, Paysend aims to make international money transfers hassle-free for individuals and businesses alike. Whether you need to support family members overseas, pay for services, or conduct business transactions, Paysend offers a convenient solution.

Paysend proudly allows customers to transfer money to over 170 countries.

Countries serviced by Paysend include:

To view a complete list of countries that Paysend serves, navigate to the home page. There you will find the money transfer calculation tool. Select the drop down menu for the receiving country and you will be shown all the countries you can send money to! Another way to check the complete list is to scroll down on the home page and view the large list of countries they allow remittances to.

Paysend charges a flat fee for their transfers. For every transfer, Paysend displays the currency exchange rate, transfer fee and receivable amount before you make the transfer. This can either be accessed once you secure your Paysend login and initiate the transfer or it can be seen by filling out the money transfer calculation tool.

The Paysend fee is 2 USD for each transfer.

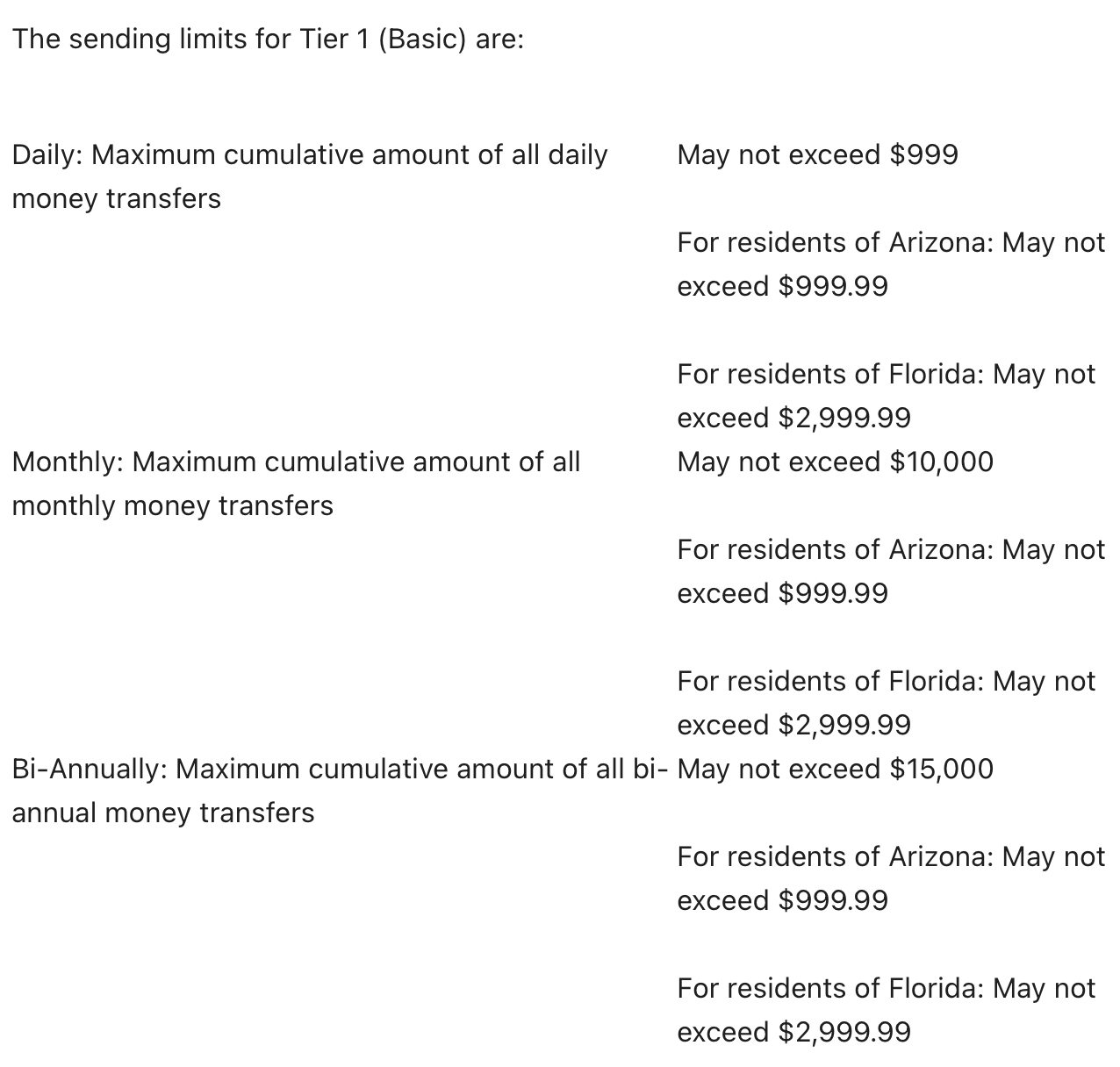

Paysend’s limits for transfers from the United States are based on a tier system.

Tier 1 is the basic tier. You will automatically be in this tier when you create your login. The limits for Tier 1 are listed below:

To qualify for Paysend’s Tier 2 (Advance) sending limits, you will need to successfully verify your SSN/ITIN number and personal data.

To qualify for Paysend’s Tier 3 (Ultimate) sending limits, you will need to successfully verify the source of income.

Here are some of the identity verification items that Paysend may ask from you:

The speed of your transfer depends on various factors: the provider’s processing time, the recipient's bank efficiency, destination procedures, paperwork, payment methods, and even the time of day you initiate the transfer.

Accessible 24/7 from your smartphone or laptop, Paysend ensures your money arrives within minutes, sometimes even seconds. No queues, no waiting – just swift, hassle-free transfers.

To accelerate your transfers, opt for a provider that checks these boxes:

Your funds usually arrive within minutes, sometimes even seconds, while the slowest cases might take up to three days due to the recipient's bank.

Yes, Paysend takes significant measures to ensure the safety and security of its users' transactions. The company employs robust encryption and security protocols to safeguard sensitive data, including personal and financial information.

Additionally, Paysend is regulated and authorized by financial authorities in various countries, which adds an extra layer of credibility and accountability to their services.

Regardless, it's always advisable to follow best practices, such as using strong, unique passwords and keeping your account information confidential, to enhance your online security when using any financial platform, including Paysend.

Now for the biggest question you must have: how does Paysend work?

Luckily, using Paysend for your international money transfers is relatively straightforward. Here's a step-by-step guide:

Paysend offers various ways to contact their customer support team for assistance or inquiries.

To get a frequently asked question answered, visit their Help Centre. Here, you will also find their chat bot, allowing you to ask live questions should you have any organic or follow up questions.

You can also provide feedback or submit a question by contacting the Paysend customer support team via their email: [email protected]

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Paysend money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Paysend service are:

Paysend's standout feature, undoubtedly, is its inviting and rewarding refer-a-friend program. Here's how it works: within your Paysend profile, you can discover your unique invite code on the Paysend Bonus page. Share this code with your friends, and when they complete their first transfer using your invite code, the magic happens. You stand to earn up to £12, 18€, or $24 in bonuses for each of your friends. What's even more impressive is that these bonuses keep coming! You can receive £1, 1.50€, or $2 for each of the 12 successful transfers made by your referred friends, within the first 12 months.

These bonuses are versatile and don't discriminate based on the frequency or destination of your friends' transfers; local or international, Paysend rewards them all. It's a win-win situation - your friends benefit too! They'll enjoy a fee waiver on their first successful transfer, access to instant transfers at favorable exchange rates, and the opportunity to pay it forward by inviting their friends and reaping Paysend bonuses. As for spending your well-earned bonuses, they can be seamlessly transferred to a bank card in pounds, euros, dollars, or your respective registered currency. The minimum transfer amount is just £5, 5€, or $5. So, refer your friends, share the benefits, and reap the rewards - all within the Paysend ecosystem.

Please note that this enticing program is open to all Paysend customers, with the exception of customers from specific countries

If you’re looking for an alternative to Paysend’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Paysend? Is Paysend legit? Let’s see what users of Paysend have to say. Sourced from multiple platforms, customer reviews of Paysend are:

Paysend scores an “Excellent” rating on TrustPilot with a TrustScore of 4.3 out of 5.

“The best money transfer ever. Very easy to setup the account, and worked excellent and fast…and basically free. Absolutely nothing negative about it.” - User on TrustPilot

“Honestly? Life-saving experience. If there would be a plus next to five stars, would give it without hesitation. Trustworthy, reliable, fast, affordable smooth service.” - Ilja Kabanen on Trust Pilot

Negative reviews pertain to issues with identity verification and transfer delays.

PaySend stands out as a reliable and convenient option for international money transfers. With its user-friendly interface, competitive rates, and commitment to security, PaySend provides a seamless experience for users looking to send money across borders. Whether you're supporting family members, conducting business, or making payments, PaySend offers a trustworthy platform to meet your financial needs.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

24759 views

24759 views