Every little penny counts when you are sending money across the globe. With a plethora of remittance companies on the market, it has become more challenging than ever to find the right company to trust with your money transfer.

Pomelo Money Transfer has emerged as a prominent player, offering seamless and secure cross-border financial transactions. In this comprehensive review and guide, we will delve deep into what sets Pomelo apart, examining its features, costs, safety, and the process of transferring money. Whether you are a frequent international traveler, a business owner, or simply someone who needs to send money across borders, this guide will provide you with valuable insights into the world of Pomelo Money Transfer.

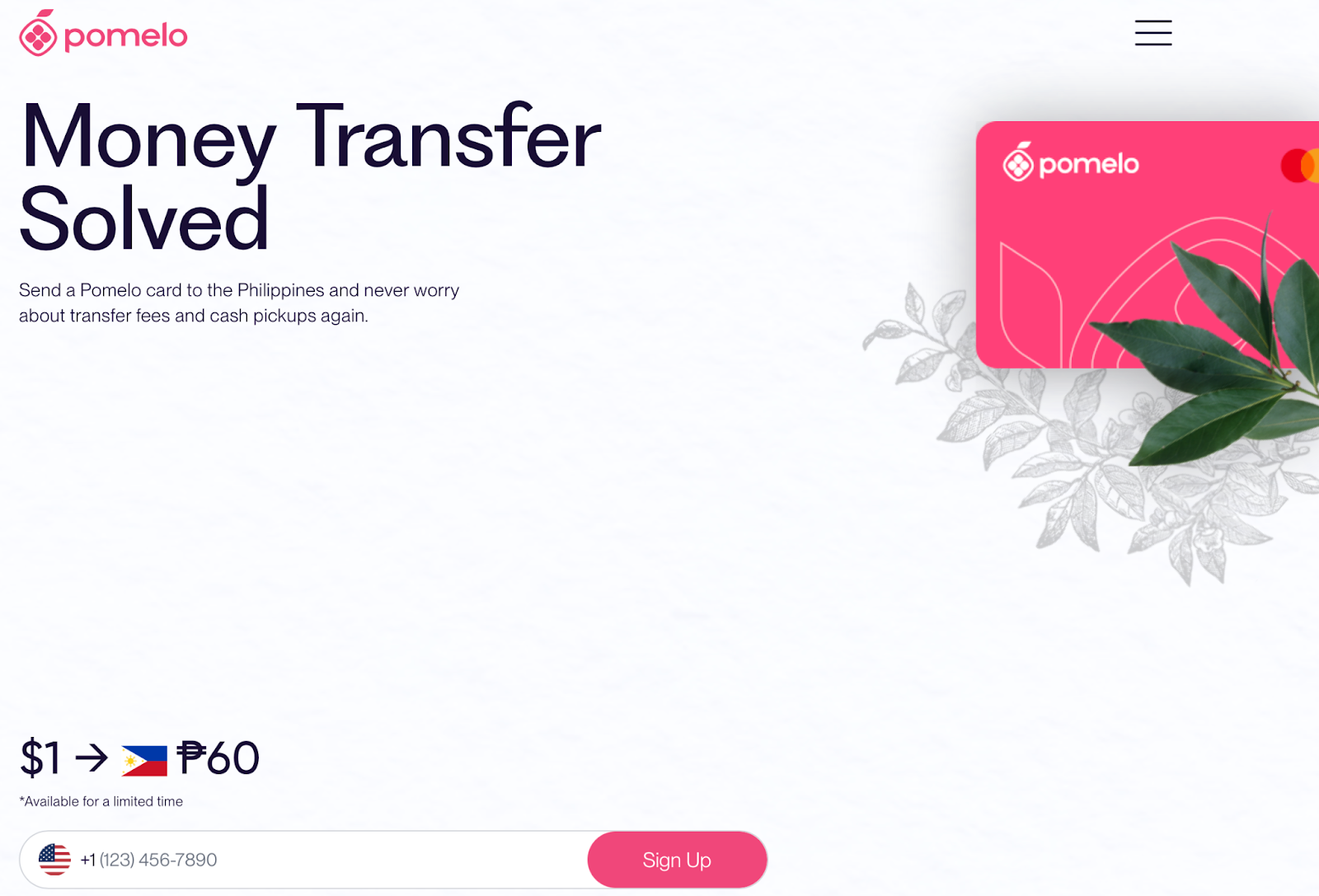

Pomelo Money Transfer is a revolutionary online platform designed to simplify international money transfers to the Philippines. What makes Pomelo unique is its user-friendly interface, seamless charge card system, and competitive exchange rates. By leveraging cutting-edge technology, Pomelo ensures swift and secure transactions, catering to individuals and businesses alike.

Unlike traditional money transfers, Pomelo completes money transfers as a charge card, a distinctive type of credit card where the entire balance must be paid off every billing cycle. This means no accruing interest whatsoever, as there is no APR (Annual Percentage Rate) involved. Additionally, Pomelo imposes a modest maximum limit, usually up to $1,000, ensuring that customers do not find themselves ensnared in debt.

The only fee associated with Pomelo is a late payment charge; however, to assist customers in avoiding this fee, auto-pay options are available. To obtain the Pomelo Mastercard, individuals need to follow the standard application process, similar to applying for any other credit card product.

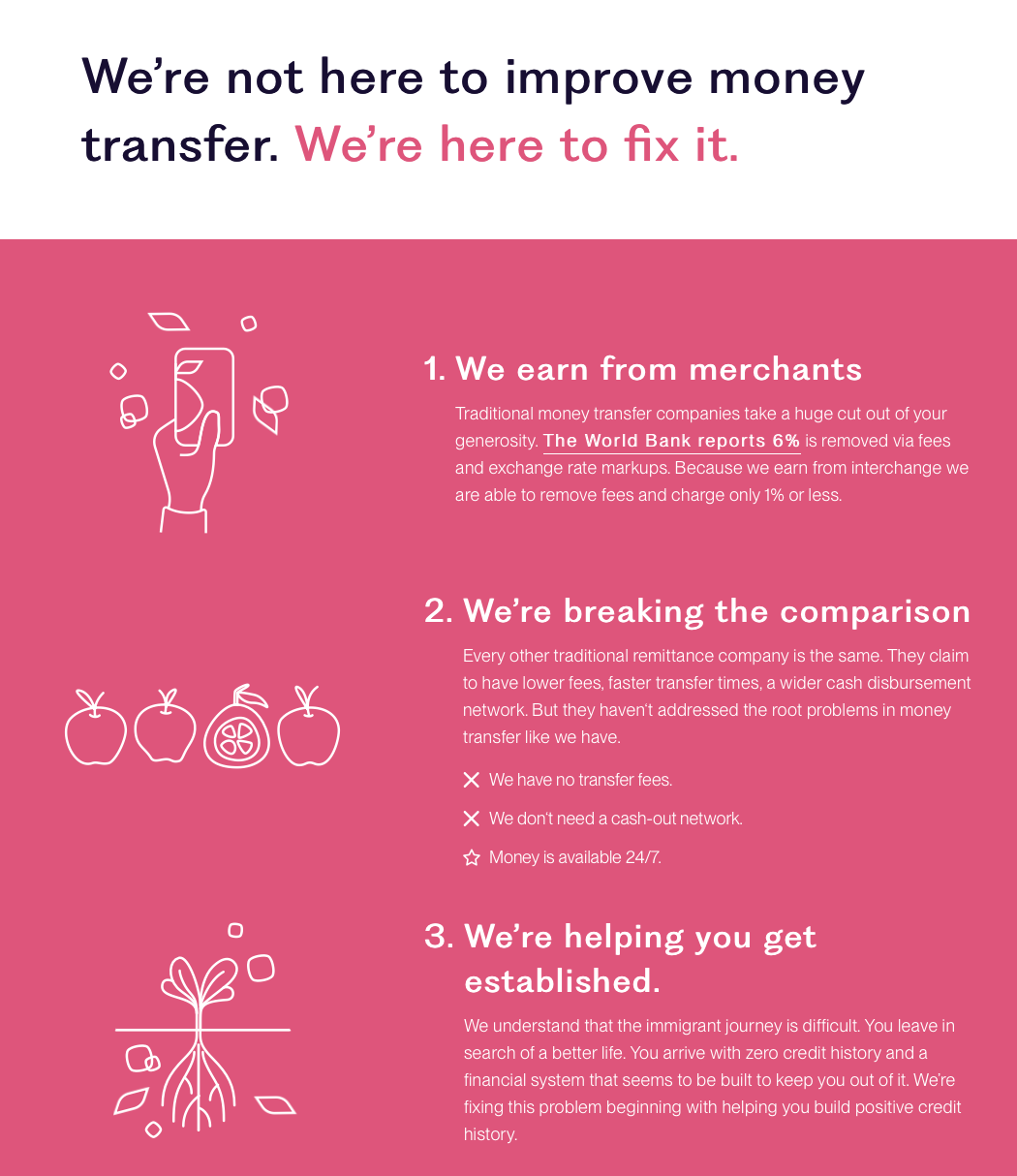

We have great news for you! Since Pomelo operates as a charge card and not a money transfer that needs to be funded before your transaction, your transfer fee is completely free. Pomelo charges no transaction fees.

However, as we touched on earlier, the entire balance must be paid off every billing cycle. Any fee you will face is late fees on your card’s payment.

Pomelo imposes a $1,000 fee on your card to avoid their customers falling behind in their payment.

One of the standout features of Pomelo is that transfer speed does not apply to Pomelo. Money doesn't take days, hours, or even minutes to arrive. Add your “recipient” as a user for the card. As long as the recipient possesses a Pomelo card and has available credit, they can instantly access the funds. In the event of an emergency, there's no need to rush the transfer process, provided there's credit within the limit; the needed funds are readily accessible.

Pomelo ensures the safety of its users by implementing robust security measures. The platform was meticulously crafted with safety in mind, offering a level of security comparable to that of banks for cashless money transfers. Users have the flexibility to pause their card whenever necessary, and all personal information is encrypted to safeguard privacy. This approach eliminates the need for loved ones to queue up at pawnshops or carry large sums of cash.

What sets Pomelo apart is the peace of mind it provides. Users need not worry about the whereabouts of their money; the bill is settled only after the money has been spent by their loved ones. Additionally, Pomelo offers a mechanism to dispute any suspicious transactions, similar to a credit card, providing an added layer of security. This stands in stark contrast to the uncertainties associated with traditional money transfers, where users often find themselves hoping for the best every time their money leaves their bank account. With Pomelo, such concerns are effectively addressed, offering users a reliable and secure money transfer experience.

Now for the biggest question you must have: how does Pomelo work?

Do not worry. It might seem intimidating at first but Pomelo has made the process easy and straightforward.

.png)

[From Pomelo FAQs]

From here, your loved ones spend in the Philippines and you pay off the balance monthly.

Pomelo offers various ways to contact their customer support team for assistance or inquiries.

Pomelo has a FAQ section on their website. This resource can provide answers to many common questions and guide you through various aspects of using their service.

Still need help? Reach out to their customer support team by emailing: [email protected] or you can send a letter at this address:

Pomelo Card

221 Main Street, Suite 770,

San Francisco, CA 94105

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Pomelo card are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of Pomelo remittance service are:

One of Pomelo's most distinctive features lies in its innovative "Send now, Pay later" model, setting it apart in the realm of money transfer services. With Pomelo's charge card, your loved ones in the Philippines gain instant access to funds as soon as they receive their Pomelo cards. What makes this system particularly convenient is that you, as the sender, don't have to worry about immediate payments. Instead, the bill arrives at the end of the month, allowing you the flexibility to handle financial matters at your convenience. The bill is calculated using the Pomelo rate along with any applicable promotional rates you may have, ensuring a transparent and hassle-free experience for both the sender and the recipient. This unique approach not only simplifies the process but also provides peace of mind, making Pomelo a standout choice for effortless and timely money transfers.

If you’re looking for an alternative to Pomelo’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Pomelo? Is Pomelo card legit? Let’s see what users of Pomelo have to say. Sourced from multiple platforms, customer reviews of Pomelo are:

Pomelo scores a “Great” rating on TrustPilot with a TrustScore of 3.9 out of 5.

“Very convenient to use and great card for me and my family in the Philippines. Pomelo Card is awesome ! It is a great help to my family they use it as emergency funds ! I don't have to send cash they just use it for tuition, groceries, utilities, restaurants. So easy and very convenient to use. My special thanks CEO Eric for you are the Best. You act right away for any request I've asked. You are very professional and very supportive! Thank you Pomelo Team !” - Dante on Google Play

“I’m so excited about Pomelo card! I think it’s great to have access to credit without the hassle of traditional lenders. Pomelo is a revolutionary concept, and it’s safe and easy to use.” - User on the Apple App Store

“Fantastic Service. Nice and simple process to open the account and lots of support from the team when something is not right. Sara responds to in app messages 7 days a week, even bank holidays, and always has an answer to a question. I'd highly recommend them to others who want a quick and easily solution to taking card payments and at a low rate. Thanks!” - Daniel on TrustPilot

Pomelo Money Transfer stands out as a reliable and efficient solution for international financial transactions. Its user-friendly interface, no transfer fees, competitive exchange rates, instant availability of the transferred money, and robust security measures make it a compelling choice for individuals and businesses needing to send money across borders. By combining convenience with safety, Pomelo has positioned itself as a frontrunner in the digital money transfer industry. To experience seamless cross-border transactions, consider Pomelo Money Transfer for your financial needs.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

13528 views

13528 views