There are so many remittance companies on the market these days. It is harder than ever to figure out which money transfer company is right for you. Don’t worry! We’ve got you covered.

Profee Money Transfer has emerged as a prominent player in the realm of fast, secure, and efficient cross-border transactions. In this comprehensive review and guide, we will explore the key aspects of Profee, shedding light on what sets it apart in the world of online money transfers. Whether you're a first-time user or someone looking to make an informed decision about using this service, we'll cover everything you need to know about Profee's features, cost, safety, and how to use it.

Profee is an online money transfer service that facilitates swift and secure transfers between individuals and businesses. Unlike traditional methods, Profee leverages cutting-edge technology to provide a hassle-free experience, making it a viable solution for those seeking to send money across borders or within the same country. The platform is available through their website at profee.com and offers a user-friendly mobile app for convenient access.

Profee offers a quick and dependable online platform for card-to-card transactions, catering to residents in the EU and the UK. This service is accessible for a range of card types, including Visa, MasterCard, and Maestro. Notably, recipients can receive funds seamlessly without the need to register with Profee, enhancing the convenience of the entire transaction process.

Profee specializes in sending money from Europe. If you are trying to send money from the United States, this might not be the remittance solution for you.

Countries that you can money to using Profee Money Transfer include:

To view a complete list of countries that Profee serves, navigate to the home page. There you will find the money transfer calculation tool. Select the drop down menu for the receiving country and you will be shown all the countries you can send money to!

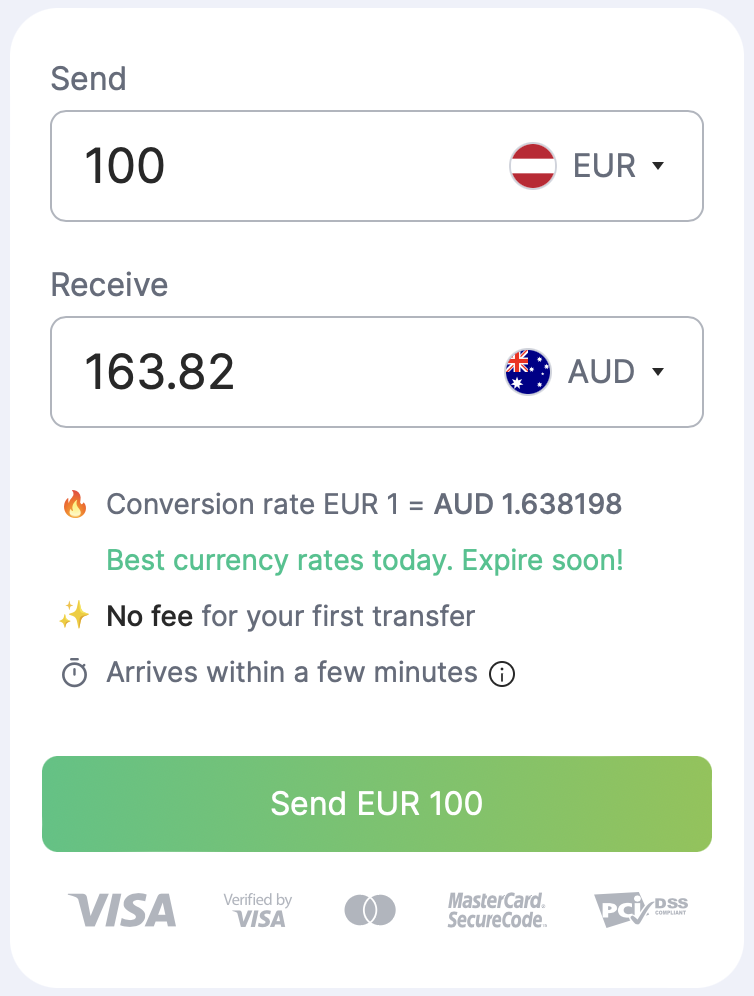

Profee is known for its transparent fee structure. The cost of using Profee typically includes a reasonable transaction fee and currency conversion charges. The exact fees may vary depending on the transfer amount and the specific countries involved. It's advisable to check the latest fee details on the Profee website or app before initiating a transfer.

To find the exact fee that your transfer will face before you commit to the process of signing up for Profee, you can use the same money transfer calculation tool we mentioned earlier. Enter the details of your transfer, including: the country you are transferring from, the country you are sending money to, and how much money you want to transfer. Then, you will see the cost of your transfer, how long your transfer will take, and any special offers that you are automatically qualified for.

Users have the flexibility to send up to 1,000 EUR after setting up their Profee profile. To expand this limit to 15,000 EUR, users need to verify their identity by providing proof, including a selfie holding their identity document.

Additionally, Profee's system might request a document to confirm the user's address, which could be a utility bill, bank statement, municipality or governmental tax letter, or a house insurance document. It's important to note that the document provided should not be older than 3 months. Depending on the user's country, an internal passport might also be accepted.

The verification process typically takes 15 minutes, ensuring a swift and secure experience for Profee users.

Profee prides itself on providing swift money transfers. The time it takes to complete a transfer can vary depending on several factors, including the destination country and the recipient's bank. In many cases, transfers can be completed within minutes to a few business days.

As we briefly mentioned previously, you can use Profee’s money transfer calculation tool on the homepage to get a personalized estimate of how long your transfer will take.

Profee prioritizes the security of your financial transactions. The platform employs advanced encryption technologies to protect your data and utilizes secure payment gateways for financial transactions. It is a legitimate and regulated service, complying with the necessary regulations to ensure the safety of its users' funds.

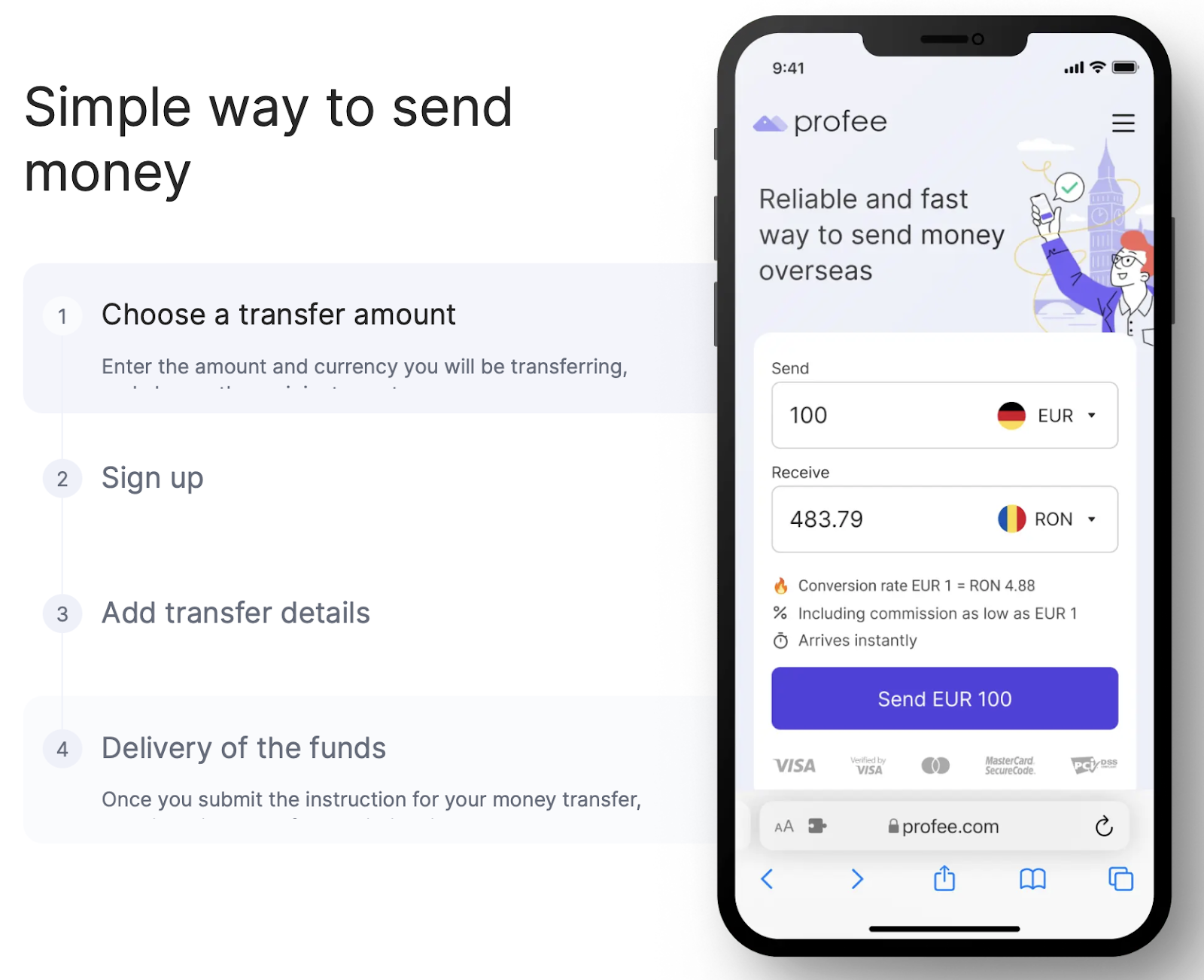

Now for the biggest question you must have: how does Profee work?

Luckily, using Profee for your international money transfers is relatively straightforward. Here's a step-by-step guide:

For any inquiries or issues, individuals can rely on Profee's dedicated Customer Support team. The team members are proficient in English, Russian, and Greek, ensuring effective communication and assistance.

Customers can easily reach out through the chat button located in the lower right corner of the website, via email at [email protected], or by calling the phone number +357 22 000 253. Profee is committed to providing professional and friendly support to its users.

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Profee money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Profee service are:

If you’re looking for an alternative to Profee’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Profee? Is Profee legit? Let’s see what users of Profee have to say. Sourced from multiple platforms, customer reviews of Profee are:

Profee scores a “Excellent” rating on TrustPilot with a TrustScore of 4.3 out of 5.

“I continue to use Profee on a regular basis and wouldn't use any other service.

Profee are second to none.” - andrzej jankowski on Trustpilot

“Thanks for the quick support. Thank you so much for the quick resolution. Now the profile has been verified and I was able to transfer. On the first go, it was very easy to use and very smooth. I will still use the services and repost the review very soon. Good rate of exchange.” - User on Google Play Store

“No problem. The function is easy and the transfers are very fast. The app has several small glitches that can be confusing. However none will cause a real issue. There are other companies out there with a greater name that are not as good.” - User on Apple App Store

Negative reviews pertain to issues with logins, issues with customer support, and transfer fees.

Profee Money Transfer distinguishes itself with its exceptional card-to-card money transfer system, a standout feature that sets it apart in the realm of online financial services. Designed for residents in the EU and the UK, Profee offers a rapid and reliable platform for seamless transactions between various card types, including Visa, MasterCard, and Maestro. What makes Profee's service truly user-friendly is the recipient's ability to receive funds without the necessity of registering with the platform. This streamlined process ensures convenience and efficiency, making Profee a preferred choice for individuals seeking swift and hassle-free money transfers.

In the realm of digital money transfers, Profee stands as a reliable and user-friendly option, offering competitive pricing, swift transfers, and top-notch security. By leveraging its innovative app and website, Profee ensures that users can send money conveniently, making it a commendable choice for various financial needs. To experience seamless money transfers and enjoy peace of mind, consider using Profee for your next transaction.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

14396 views

14396 views