Remitly is a leading online money transfer service that has revolutionized the way people send and receive funds across borders. Unlike many of their competitors, Remitly allows users to send money not only from the US but from 28 different countries, making it a great option for people around the globe.

With a mission to make the remittance process faster, more affordable, and hassle-free, Remitly has garnered a reputation for its efficient and secure platform. Whether you're supporting family overseas or conducting international business transactions, Remitly's user-friendly interface and competitive exchange rates make it an attractive choice.

In this review, we'll explore the features and benefits of Remitly's money transfer service, examining how it stands out in the competitive landscape of global remittance solutions. Whether you are a curious newcomer seeking a reliable remittance solution or a seasoned user of the service, we've got you covered with all the essential information you need to know about Remitly.

In this comprehensive Remitly review, we take a deeper dive into the Remitly online money transfer service and determine if it is the best option for sending money overseas.

Remitly is an online money transfer service that allows individuals to send money across borders quickly and securely. The platform was founded in 2011 with a specific focus on providing an efficient and cost-effective solution for remittances – money sent by immigrants to their families and loved ones back home.

Remitly prides itself on serving 170 countries worldwide and their 24/7 customer service availability.

To get started with Remitly, you simply need to create a free account and begin the simple money transfer process, which will be outlined later in this review. Maintaining your Remitly.com login requires no fee. Once you have secured your Remitly login, you can begin the money transfer process through Remitly.com or the Remitly App.

Countries supported by Remitly Money Transfer include:

You can view the complete list of countries served by Remitly by clicking on the “Select a Country” button on the home screen and scrolling through the list that shows up.

Unlike many of its competitors, Remitly’s fees change based on their own, added metric: speed. Customers can select how fast they want their transfer to be received from two speeds, Express and Economy.

Remitly’s fees and the everyday rate are dependent on how much money you are planning to send, the transfer speed you select, and the country you are sending the money to.

Typically, the Express option gives you a faster transfer but a less optimal transfer rate and the Economy option gives you a slower transfer but a more optimal transfer rate.

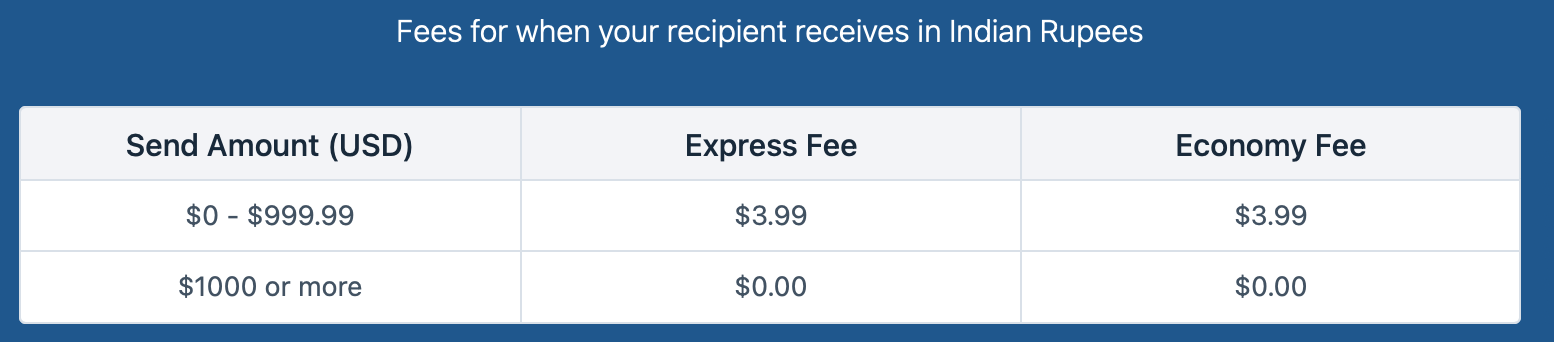

For example, sending money to India with Remitly today will look something like this:

With the fees associated with Express and Economy looking something like this:

Want to have an idea of what your Remitly transfer fee will be before you commit to the process of creating a login? You can visit the Remitly pricing page to get a breakdown of what your transfer fees will approximate to.

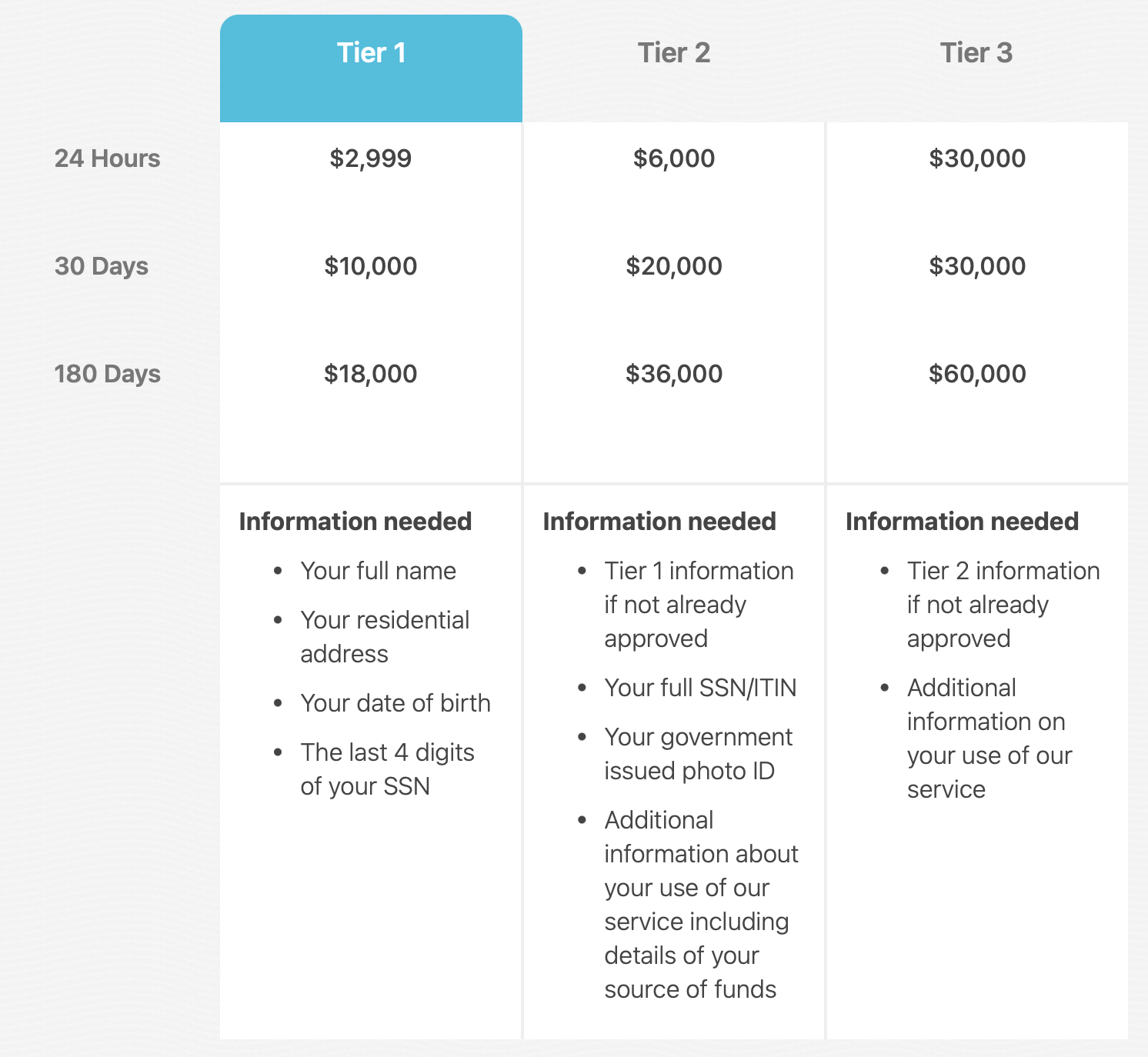

Remitly’s sending limitations are primarily based on your location and your recipient’s location; Remitly also has various limitations on how much you can send in 24 hours, 30 days, and 180 days. But do not worry, if you would like to exceed your limit, then you are allowed to request a limit increase.

Here is an example of what spending limits would look like if you are transferring money to India:

Tier 1 is the basic sending limit, the one every customer starts off with, right from the login. Once you request a sending limit increase, sending all the requested information and it is verified successfully, you will have the Tier 2 sending limits. Similar to the process of achieving Tier 2, once you have submitted a request and have the verification of the necessary information you provided, you will have the Tier 3 sending limits.

To see the sending limits for the country you are choosing to send money to, simply visit the “Increasing Limits” page on Remitly to see a relevant breakdown of the limits, similar to the one shown above.

As we stated above, Remitly is unique in the sense that they offer two speeds: Express and Economy. Express sends your money faster than Economy.

The time your money takes to transfer depends on where you are sending your money to and which speed you chose. To find out a more accurate estimate of how long your transfer will take: open the Remitly app or visit the website, sign in to your account, start a new transfer with your desired sending amount and transfer location, and Remitly will show you the available transfer options and speed details.

Remitly prides itself on having a system made for immigrants. The personal information they ask of you is carefully secured and thoroughly verified, all to ensure that only you can send money from your account. Remitly is licensed to do business in the 28 sending countries and more than 130 of the receiving countries that they serve.

Remitly has also set up a notification system that alerts you if there is any suspicious activity in your account.

Remitly allows you to cancel your transfer if the process is still in its pending status.

To further ease your doubts, Remitly has a 100% satisfaction guarantee. If you aren’t satisfied with your transfer for any reason, Remitly will refund your fees.

Now for the biggest question you must have: how does Remitly work?

Sending money with Remitly requires you to first create an account. The account is free; select the country you would like to send money to and continue to register with your email and chosen password.

Once you have an account created, your personal documents verified, and your identity verified as well, follow these detailed steps to set up your first remittance transaction.

Remitly has 24/7 customer support available to you.

Their search center answers in 15 languages. Their chat feature is available in English, French, and Spanish. Remitly has two phone lines available, one in Spanish and the other in English.

Call toll free from the United States:

(844) 604-0924

For all other countries:

1 844-604-0924.

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Remitly money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Remitly service are:

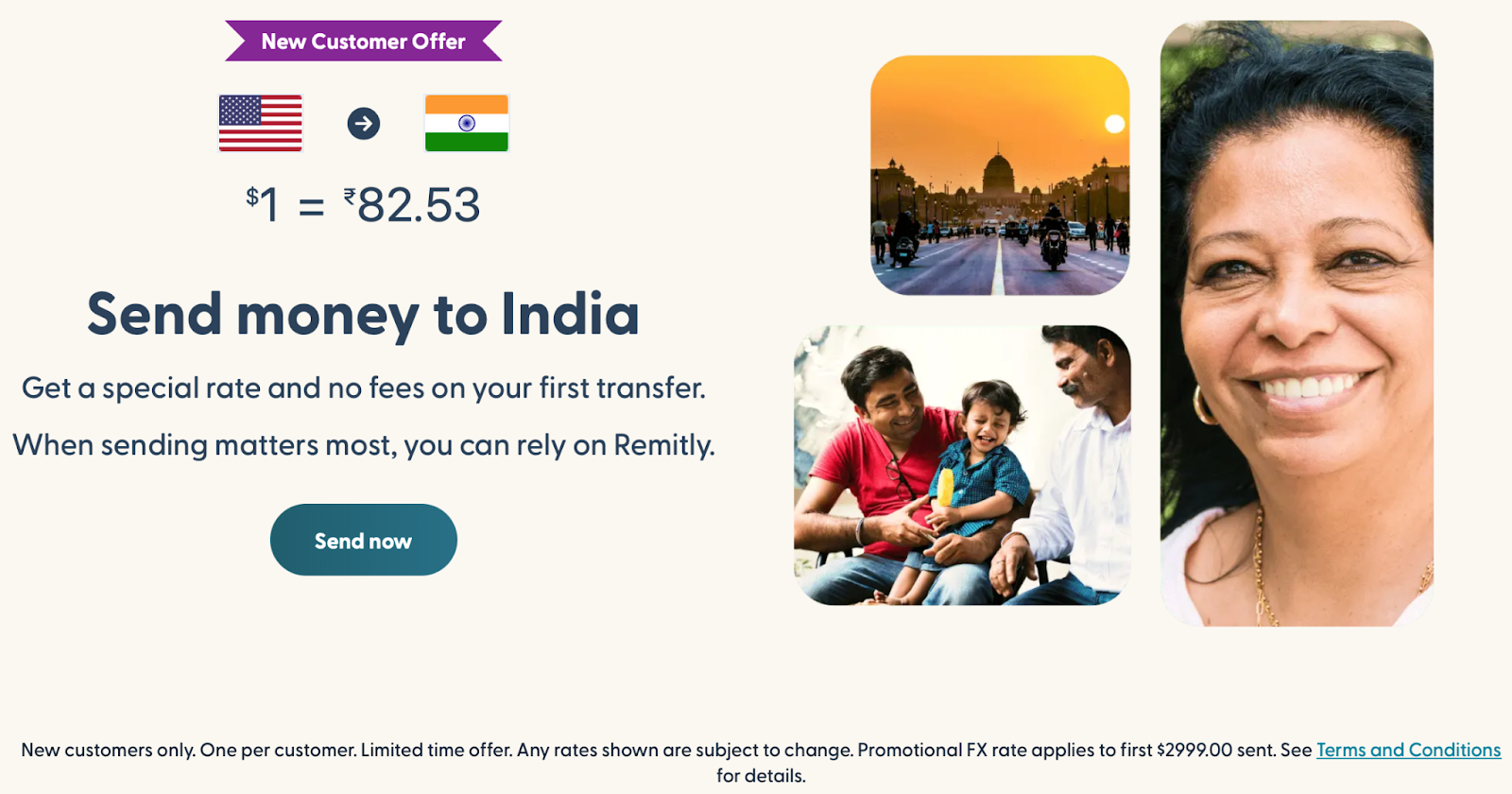

As we mentioned briefly, Remitly offers first-time customers a special deal. This deal allows for you to get the most money to your recipient, a special rate, and no fees on your first transfer. This is a great deal for those considering Remitly.

If you’re looking for an alternative to Remitly’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Remitly? Let’s see what users of Remitly have to say. Sourced from multiple platforms, customer reviews of Remitly are:

Remitly scores high on TrustPilot with a TrustScore of 4.1 out of 5.

“It's [a] user friendly mobile app. I didn't use [the] express service but [the] money reached in 2 hours in my brother's bank account [in] Gujarat, India. [The] rate is [a] bit low plus service charges on top, [it] makes a bit [of a] loss on my side. [They] keep [the] exchange rate for India [a] bit better on [the] plus side to keep customers happy, even [a] few pence/paisa makes [a] big difference in total when sending big amounts. Thanks.” - Mr. K Rajput on TrustPilot

“Amazing! It works exactly as it describes it. It's reliable, quick, [and I'm very] happy for having tried it. For sure I won't use anything else.” - Alex Heraso on TrustPilot

“I always saw Remitly ads and didn't pay much attention until I tried the app, not only am I extremely satisfied with the service in general, and with the customer service, but also happy that the use is very easy and [they] charge less than other apps. 100% recommended.” - IrvingRPolanco on TrustPilot

Negative reviews pertain to issues with identity verification and transfer cancellations as a result.

Remitly is a trusted remittance service with many happy customers. It is a very worthwhile option for beginners because of the first time user offer that Remitly provides.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

40165 views

40165 views