In the ever-evolving landscape of financial technology, neobanks have emerged as a revolutionary force, providing innovative and efficient solutions for managing finances. Vance Money Transfer is a pioneering neobank service that offers a seamless and secure way to transfer money.

In this comprehensive review and guide, we will explore the key aspects of Vance, including its unique features, cost, speed, safety, step-by-step instructions for money transfer, pros and cons, and more.

Vance Money Transfer, offered by the neobank Vance, is a cutting-edge solution designed to meet the needs of individuals seeking efficient international money transfers, especially those with NRE (Non-Resident External) and NRO (Non-Resident Ordinary) accounts in India. Vance is a neobank that specializes in NRI (Non-Resident Indian) banking services, offering a range of financial solutions tailored to the unique needs of the Indian community.

What sets Vance apart from traditional banks is its user-friendly digital platform, which provides an exceptional level of convenience and transparency. Vance offers a unique combination of advanced technology and personalized service, making it a go-to choice for those in need of hassle-free money transfer services.

Keep in mind that currently, Vance only supports GBP to INR and AED to INR transfers. However, they are working hard to add more currencies to their list.

Does Vance have a limit on how much money I can send?

Vance applies a fixed fee of 3 GBP for every transfer made from the UK to India. Regardless of the sum being transferred, this fee remains consistent. Furthermore, there are no additional costs as Vance does not impose any extra mark-up on the live conversion rate, ensuring a fair and honest transaction experience every single time!

Furthermore, at the time of writing this article, Vance is offering a first time special for new customers. On your first transfer, you can get your first money transfer for free.

One of Vance's standout features is its rapid transfer speed. Utilizing advanced technology, Vance Money Transfer enables near-instantaneous fund transfers, ensuring that your money reaches its destination swiftly, a crucial aspect for urgent financial needs and emergencies.

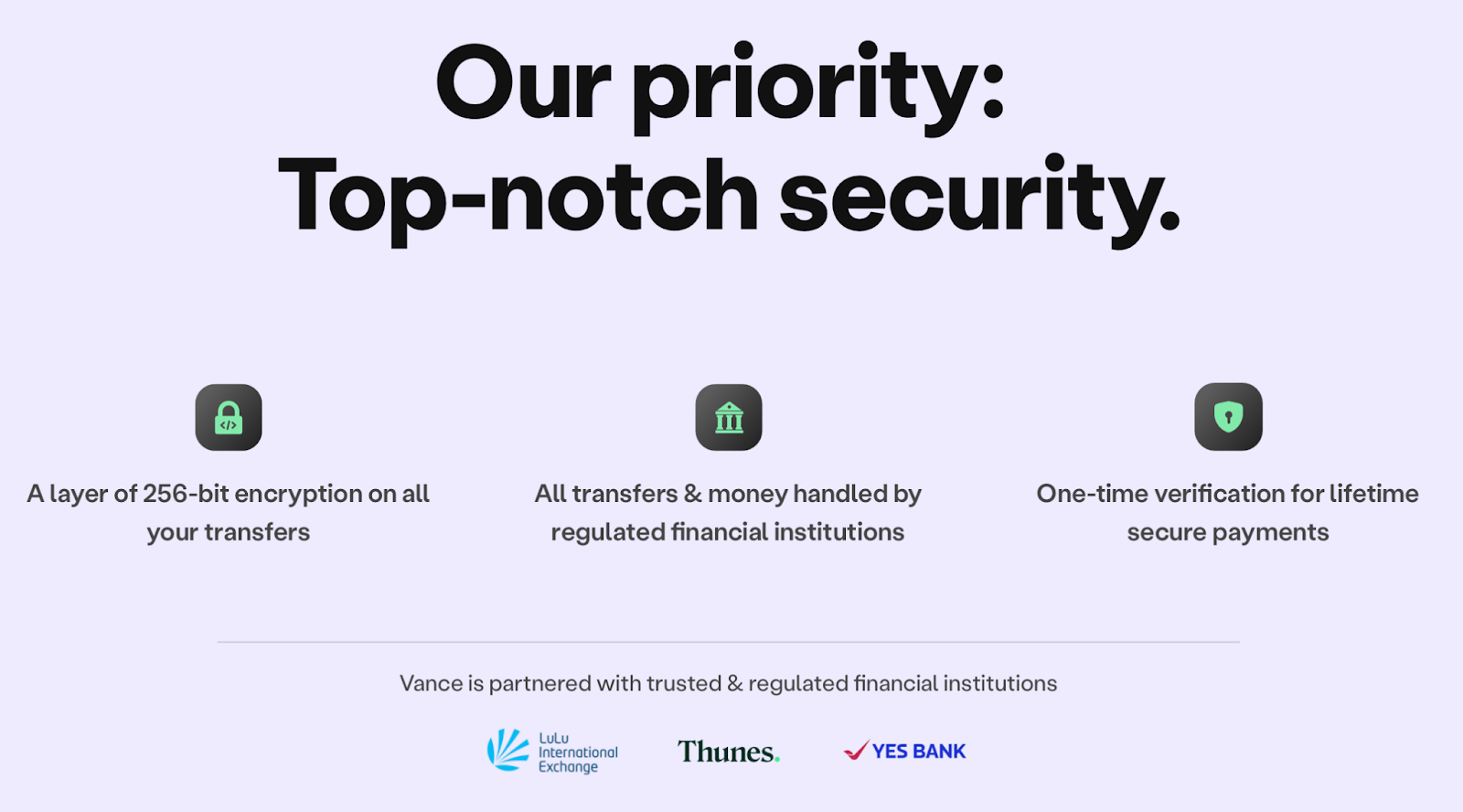

You might be wondering, is Vance reliable? Don’t worry! Safety is a top priority for Vance Money Transfer. Vance utilizes state-of-the-art encryption and security measures to protect user data and transactions. As a part of the Vance neobank, your money is safeguarded in compliance with the regulatory standards governing neobanks. Additionally, Vance provides customer support and resources to help users make safe and secure transfers.

Now for the biggest question you must have: how does Vance work?

Luckily, using Vance for your international money transfers is relatively straightforward. Here's a step-by-step guide:

Getting in touch with Vance for assistance is a hassle-free experience thanks to their multiple contact options. For starters, their extensive FAQs section covers a wide array of queries, providing instant solutions for common concerns.

If customers need more personalized help around the clock, they can reach out via email at [email protected] or chat with the support team on the Vance app.

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Vance money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Vance service are:

If you’re looking for an alternative to Vance’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Vance? Is Vance legit? Let’s see what users of Vance have to say. Sourced from multiple platforms, customer reviews of Vance are:

Vance scores an “Excellent” rating on TrustPilot with a TrustScore of 4.6 out of 5.

“The entire money transfer process was remarkably smooth and hassle-free. From the moment I initiated the transaction to the instant the funds reached the recipient in India, Vance Money Transfer ensured a secure and reliable experience. ” - Sampath on App Store

“It has completely transformed the way I send and receive money, and I couldn't be happier with the service it provides. I no longer have to worry about losing a significant chunk of my money in transfer fees. Vance's pricing is transparent, and I appreciate that they keep it affordable for their users.” - Gurchetan on TrustPilot

“I recently used Vance to transfer money from the UK to India, and I'm beyond impressed with their service. Not only did they offer the best exchange rate, but the transfer was completed in under 2 minutes! ” - User on App Store

Vance Money Transfer, offered by Vance Neobank, stands out as a reliable and efficient solution for individuals engaged in NRI banking, holding NRE or NRO accounts. With its cost-effective approach, swift transaction processing, and emphasis on security, Vance ensures a hassle-free experience for users looking to transfer money internationally. By combining technology and financial expertise, Vance Money Transfer sets a high standard in the realm of neobanking, making it a preferred choice for those seeking trustworthy and convenient international money transfer services.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

18246 views

18246 views