There is no shortage of money transfer solutions out there today. With so many options available, it isn’t easy to pick the best money transfer company for you. Don’t worry, we at CompareRemit got you covered. Let us introduce you to Sigue Money Transfer.

Sigue Money Transfer emerges as a prominent player in this domain, offering a secure and accessible platform for sending money across various countries.

This comprehensive review and guide aim to delve into the facets of Sigue Money Transfer, examining its features, costs, transfer limits, safety measures, and a step-by-step guide on how to use the service.

Sigue Money Transfer stands out among its competitors by providing a user-friendly platform that facilitates cross-border money transfers. With numerous locations worldwide and an easy-to-use app, Sigue enables individuals to send and receive money conveniently.

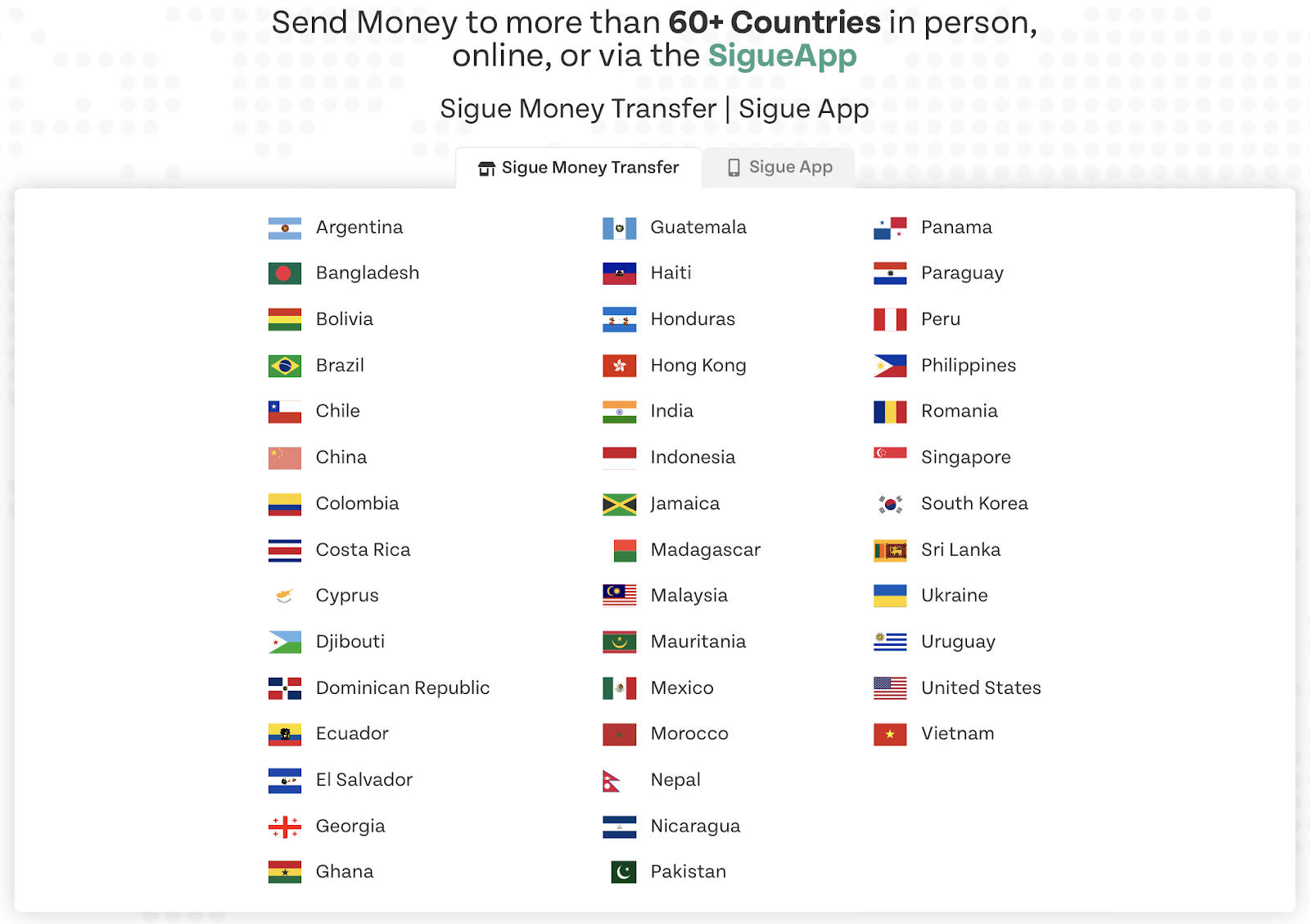

Currently, Sigue offers money transfers to over 60 countries. Countries supported by Sigue Money Transfer include:

To view a complete list of countries that Sigue serves, navigate to the home page. From there, scroll down and click on the button that says “Select a Featured Country.” Then, click on the button that says “list of countries,” and you will be shown all the countries you can send money to!

The cost of using Sigue Money Transfer is a fixed fee, subject to occasional changes. Users can easily check the current transfer fee before initiating any transaction directly on the "Send Money" screen within the app.

There are no hidden fees! The fee breakdown you are given in the app is what you will pay.

In certain transactions, the recipient might receive a reduced amount due to taxes or additional fees imposed by third parties in the destination country. These deductions will be clearly indicated on the receipt for transparency purposes.

Sigue Money Transfer imposes limits on the amount one can send, you can send a maximum of 2,999 USD per day, including the sending amount along with the associated fee.

Sigue Money Transfer offers various methods for sending money, including online transfers through their website or app, and in-person transactions at their extensive network of physical locations across different countries. Users can locate these branches using the provided tool on the Sigue website under "Sigue Money Transfer locations."

The time taken for a money transfer via Sigue depends on multiple factors, such as the destination country, service speed selected, and transfer method. While some transactions may occur within minutes, others might take longer due to verification processes or banking procedures.

For a more precise estimate of the processing times, check the transfer estimate you will get on the Sigue app.

Sigue Money Transfer prioritizes the security of its users' transactions. Employing robust encryption and security measures, Sigue aims to safeguard personal and financial information, ensuring a secure money transfer experience.

Now for the biggest question you must have: how does Sigue work?

Luckily, using Sigue for your international money transfers is relatively straightforward. Here's a step-by-step guide:

Sigue provides a tracking feature that allows you to monitor the status of your transfer in real-time either from the Sigue homepage, Sigue app, or your online login. You'll receive notifications when the money is sent and when it's received by the recipient.

Sigue Money Transfer provides comprehensive customer support through various channels. Users can access assistance by visiting the "Knowledge Center" on the Sigue website, which offers detailed information and FAQs. You can use their chat feature to chat with a live agent and ask your questions.

Still need help? Contact their customer service using this number: 1-877-754-9777

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Sigue money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Sigue service are:

Sigue Money Transfer distinguishes itself notably through its extensive network of physical branches, a standout feature that sets it apart from many competitors in the money transfer industry. Unlike several other services that primarily operate online or through limited partner locations, Sigue offers customers the convenience of accessing cash payment options and physical locations across various countries. These physical branches facilitate in-person transactions, catering to individuals who prefer or require the immediacy and assurance of face-to-face interactions when sending or receiving money. This accessibility to physical branches and cash payment options adds a layer of convenience and flexibility for users, underscoring Sigue's commitment to providing diverse and accessible avenues for international money transfers.

If you’re looking for an alternative to Sigue’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Sigue? Let’s see what users of Sigue have to say. Sourced from multiple platforms, customer reviews of Sigue are:

“The app is very easy and straight forward to use. There are no gimics or application issues. Just good business at a very fair price. The first transfers take some time maybe half a day. After their system is familiar with your account it's much faster, in a matter of hours!!” - Salim McNeely on GooglePlay

“I love how easy it is to send money to anyone in my country of Mexico. Sometimes I enjoy coupon discounts for every time I send money, which is convenient as I send to multiple people in my family. I also like that it shows me how much the exchange is for the various banks and or cash pick up participating stores.” - User on Apple App Store

Negative reviews pertain to app crashes and difficulty with the user interface.

Sigue Money Transfer emerges as a reliable and accessible platform for cross-border money transfers. With its robust security measures, diverse transfer methods, and extensive global network, Sigue provides a viable solution for individuals and businesses seeking efficient money transfer services across various countries.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

6410 views

6410 views

.jpg?v=46)