In an era where financial transactions are increasingly conducted online, the need for fast, secure, and versatile money transfer services has never been greater. Enter Skrill, a leading digital wallet and payment platform that has gained prominence for its simplicity and global reach.

Skrill Money Transfer has become a remittance staple, offering a multitude of advantages to its users. Whether you're sending funds to family overseas, purchasing goods online, or conducting cross-border business transactions, Skrill's versatile platform promises to simplify and expedite your financial dealings.

This comprehensive review and guide will take you on a journey through the intricacies of Skrill's money transfer service, equipping you with the knowledge you need to decide if Skrill is the right solution for your financial needs. We'll explore the ins and outs, provide step-by-step instructions, and weigh the pros and cons so you can make an informed choice as to whether Skrill is the right choice for you.

Skrill Money Transfer is a digital wallet and online money transfer service that allows users to send and receive money securely and conveniently. Formerly known as Moneybookers, Skrill provides a range of financial services, including international money transfers, online payments, and the ability to hold and manage multiple currencies within your Skrill wallet.

Skrill enables users to send money domestically and internationally. You can transfer funds to other Skrill users, email addresses, bank accounts, or mobile wallets, making it versatile for various transaction types.

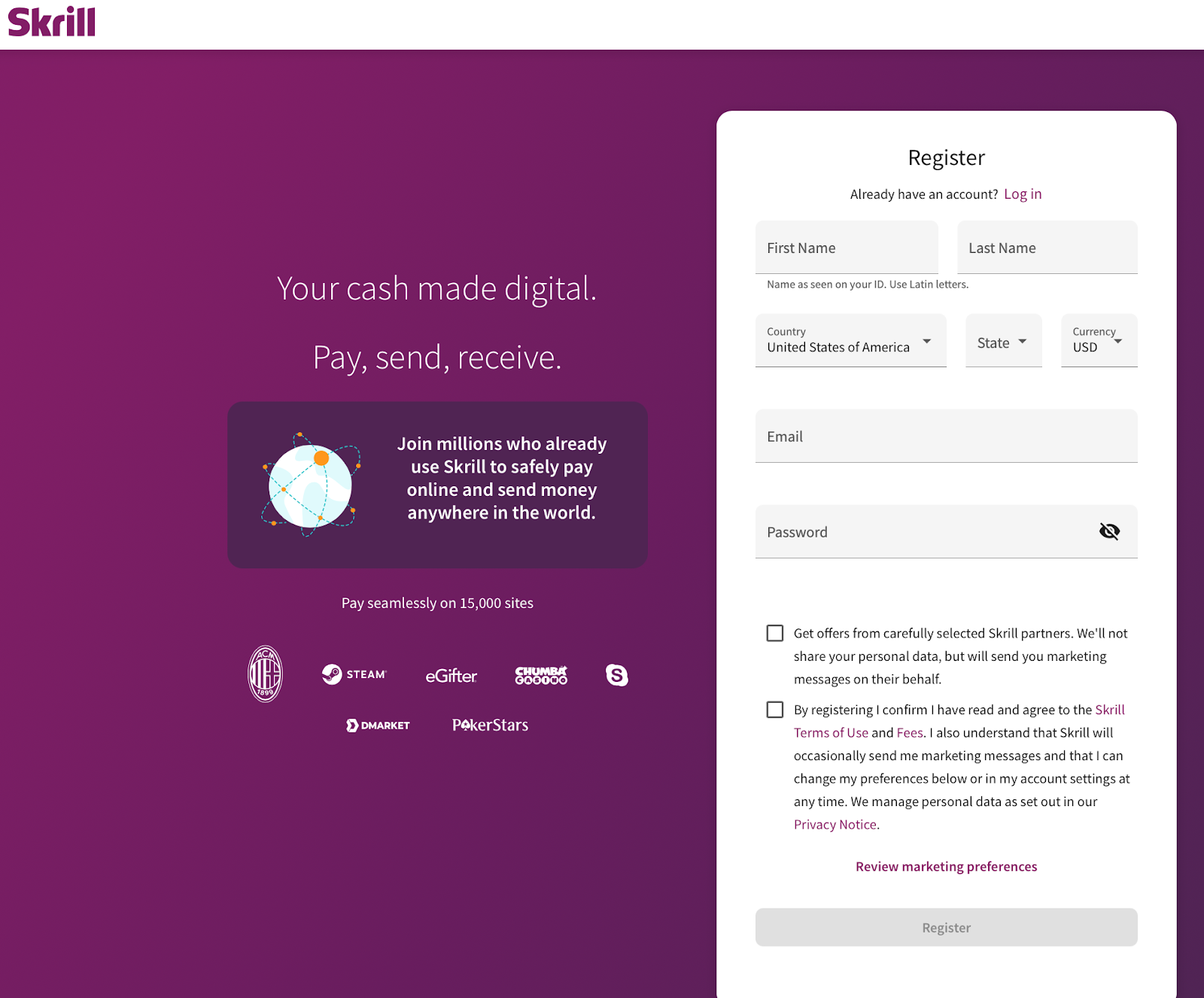

Begin your Skrill journey by creating a Skrill login for free on their website or downloading the Skrill app on your personal device. Transferring money with Skrill does require both you and your recipient to have Skrill accounts. The registration process is straightforward, but you will need to verify your identity to ensure security.

Skrill’s international reach allows you to send money to over 40 currencies and access your Skrill wallet worldwide.

Countries supported by Skrill include:

The cost of Skrill’s fees can vary based on several factors, including the type of transfer, the destination country, and the funding source you use. Skrill prides itself on transparent pricing. You can review all applicable fees before confirming your transaction, ensuring no surprises.

Skrill offers a variety of ways to send money. Whether you're transferring funds to another Skrill user, sending money to an email address, or making bank transfers, the process is intuitive. You can also choose from payment services such as Rapid, Klarna, and Paysafecash to pay for your transfer.

It's important to note that fee structures may change over time, so it's best to refer to the official Skrill website or your Skrill account for the most up-to-date fee information.

Here is a breakdown of the different types of Skrill transfer fee you could face:

[From Skrill Money Transfer website]

[From Skrill Money Transfer website]

Skrill Money Transfer does not charge recipients any fee to receive money transfers.

For a more accurate Skrill fees calculator, you will have to initiate the transfer process. Only then will you get the most accurate exchange rate and transfer fee amount.

The maximum amount of money you can send using Skrill Money Transfer depends on several factors, including your Skrill account's verification level, the country you are sending money to and from, and the payment method you are using. Skrill has different verification levels that may increase your transaction limits as you provide more information and undergo identity verification.

Skrill sets transaction limits that operate on rolling time periods, which can be daily, weekly, or monthly. These rolling periods commence from the moment you finalize a transaction and remain in effect until a specific duration, denoted as X, has elapsed.

As opposed to many of the popular remittance services, which operate on USD, Skrill operates on the European Euro. This does pose the question for many customers: Can I use Skrill in the USA? Yes, you can! Skrill proudly allows U.S. consumers to send money overseas to friends and family.

Here are some general guidelines for sending limits:

It's essential to check the specific limits for your Skrill account, which you can find by logging into your Skrill account and visiting the "Account settings" or "Limits" section. Additionally, when you initiate a transfer through Skrill, the platform will inform you of any applicable limits for that particular transaction.

It's worth emphasizing that every money transfer is distinct, and the time it takes for funds to reach their destination depends on factors such as the transfer amount and the recipient's country. Skrill, however, takes pride in its commitment to fast and efficient money transfers.

When someone sends you money via Skrill, the funds will be instantly available in your Skrill wallet.

Regardless, if not sending your funds within a few seconds of confirming your transfer, Skrill aims to complete your transfer within 24-72 hours.

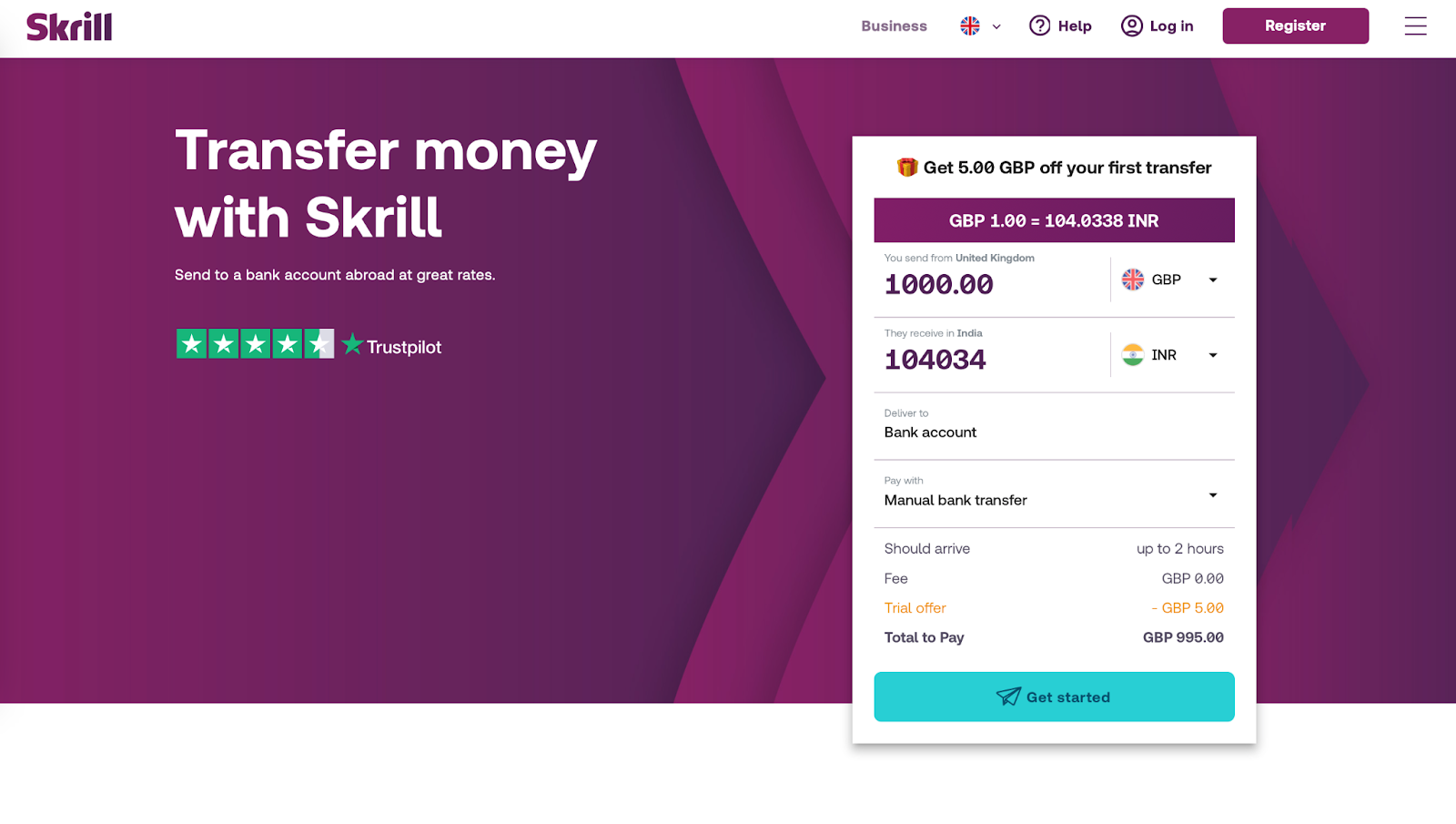

For a detailed overview of your transfer time and fee structure before you commit to the process of registering with Skrill, you can visit the homepage where you will find the calculator tool. Enter the basic details of what your transfer will look like and your estimate will be given to you in seconds.

If you're a first-time user, you might also spot a Skrill promotional code in this section, as shown in the image below.

Skrill places a strong emphasis on security, employing encryption to protect users' personal and financial information. Skrill employs robust encryption protocols to safeguard your personal and financial information during transactions. Furthermore, Skrill takes proactive measures to detect and prevent fraudulent activities, ensuring the safety of your transfers.

Enhance the security of your Skrill account at any time by activating Two-Factor Authentication. This additional layer of security measures adds an extra shield against unauthorized access.

While Skrill has indeed introduced these security measures, it remains crucial for users to take additional precautions to bolster their own security.

Now for the biggest question you must have: how does Skrill work?

Sending money with Skrill is a straightforward process. Skrill is designed to make online transfers and payments convenient and secure.

If you don't already have one, you'll need to create a free Skrill account. Visit the Skrill website or download the mobile app and sign up. You'll need to provide personal information and complete the verification process, which may include submitting identification documents.

Once your account is set up, you can add funds to your Skrill wallet. You can do this by linking your credit/debit card or bank account to your Skrill account and transferring money into it. Your Skrill wallet acts as the source of funds for your transfers.

We will walk you through three different ways you can send money so you can choose which process is the best for you. Here's how Skrill works and how to send money using the platform:

If you're receiving a transfer, Skrill will notify you when the funds are available in your account.

Skrill offers customer support through email, live chat, and phone. Their support team is available to assist with any issues or inquiries.

Skrill's customer service department phone number: 1-855-719-2087*

*Local charges apply

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Skrill money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Skrill service are:

Skrill's standout feature is undoubtedly its Refer-a-Friend program, which allows users to benefit in multiple ways. By sharing Skrill's services with friends, you not only earn valuable referral credits, but your referred friends also enjoy discounts on their initial money transfers as an enticing bonus.

To participate in this program, you typically need to reside in a participating country and have conducted at least one international money transfer above the minimum transfer amount.

The program allows you to utilize up to 5 referral credits in a single Skrill Money Transfer transaction, with the maximum credit applicable specified on their website. Any earned credit is seamlessly added to your account upon making an eligible transaction, and if you hold excess referral credit, it's conveniently applied to your next international Skrill Money Transfer, enhancing your overall savings and convenience.

If you’re looking for an alternative to Skrill’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Skrill? Is Skrill legit? Let’s see what users of Skrill have to say. Sourced from multiple platforms, customer reviews of Skrill are:

Skrill scores a “Great” status on TrustPilot with a TrustScore of 3.8 out of 5.

“I'm really happy with the fastest payment method in a few seconds. Every time I experience Skrill I get confident that everything will be as smooth as expected.” - Md. Kutubuddin on TrustPilot

“Skrill actually makes it easier to transfer the funds throughout the world and their transaction fee is comparatively low. I am really happy with their customer support as well. I can make the payments instantly and receive the funds from anywhere in [the] world within 24 hrs. I would really suggest this app to everyone.” - Kanishka T. on G2.com

“Skrill has made moving money across the globe a lot [faster] and instantaneous. Transferring money from my Skrill wallet to my mobile money wallet takes a fraction of a second.” - Oketch Esdon on TrustPilot

Negative reviews pertain to issues with identity verification and transfer cancellations/delays as a result.

Skrill is a versatile and convenient money transfer platform that can meet various needs, from sending money to friends and family to making online purchases. Its transparent pricing, security features, and global reach make it a viable choice for many users looking for a hassle-free remittance service.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

23475 views

23475 views

.jpg?v=46)