Now more than ever, transferring money across borders has become an essential part of our lives. With numerous options available, it's crucial to choose a reliable and efficient service. Small World Money Transfer is one such platform that has gained attention for its ease of use, cost-effectiveness, and secure transactions.

In this comprehensive review and guide, we will delve into the details of Small World, exploring its unique features, costs, safety measures, and step-by-step guide on how to transfer money. By the end of this article, you will have a clear understanding of Small World Money Transfer and how it can meet your financial needs.

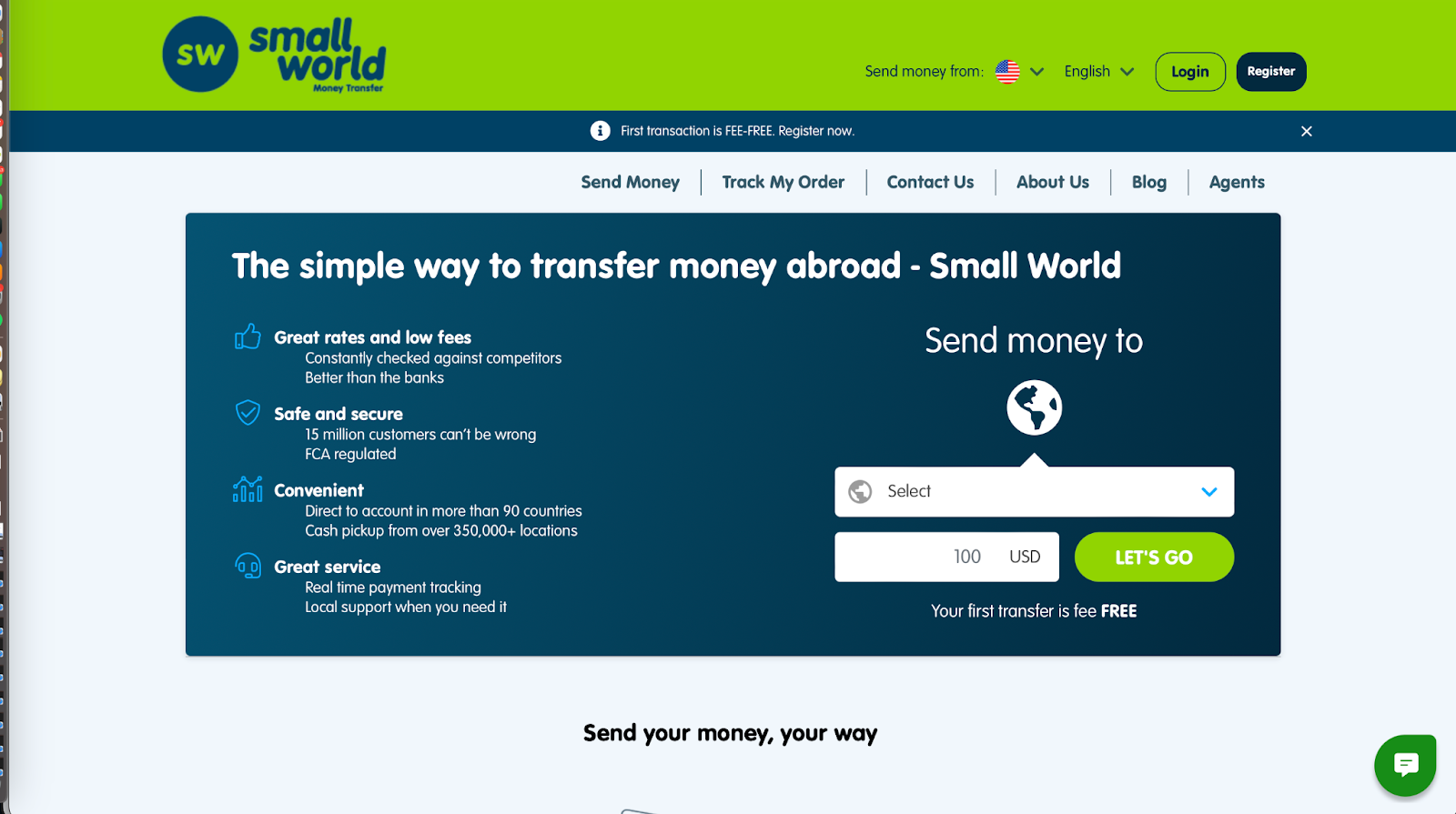

Small World is a global money transfer service that enables individuals to send and receive money across borders with ease. What sets Small World apart is its vast network, covering over 90 countries and more than 250,000 agent locations worldwide. This extensive reach ensures that you can send and receive money in various currencies to nearly any destination. Small World prides itself on offering competitive exchange rates and low fees, making it an attractive choice for international money transfers.

You can access Small World money transfer services through the Small World Money Transfer app or the Small World Money Transfer website.

As mentioned above, Small World proudly services over 90 countries. Here is a list of just some of the Small World Money Transfer location countries:

To view a complete list of countries that Small World serves, navigate to the home page. There you will find the money transfer calculation tool. Select the drop down menu for the receiving country and you will be shown all the countries you can send money to!

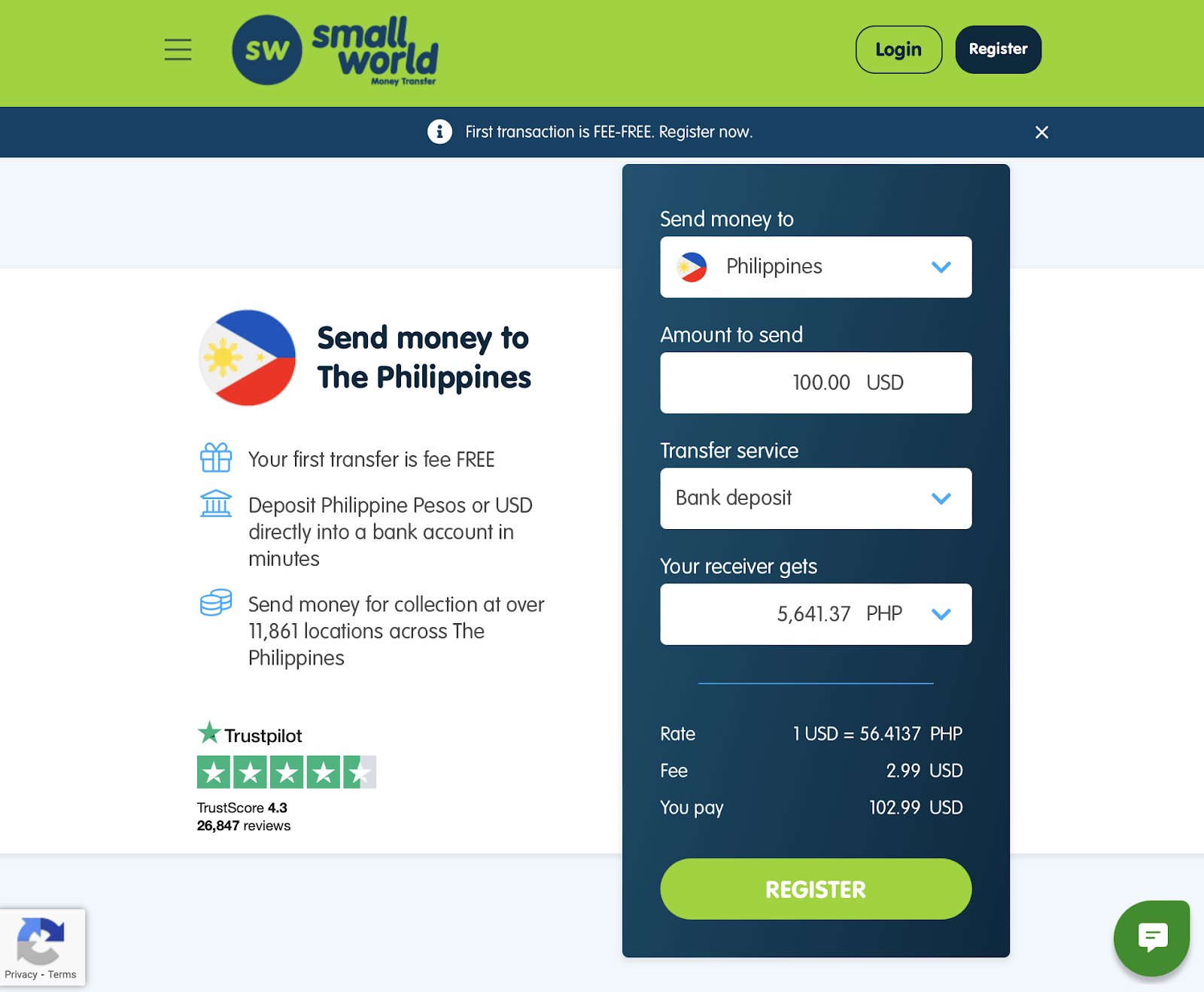

Small World offers transparent and competitive pricing. The cost of transferring money with Small World depends on various factors, including the destination, transfer amount, and the payment method you choose. Typically, Small World's fees are relatively low compared to traditional banks and other money transfer services.

To get an accurate estimate of the costs for your specific transfer, you can use the online calculator provided on their website, which asks you to enter just the transfer amount and the destination country.

Small World offers transparent and competitive pricing. The cost of transferring money with Small World depends on various factors, including the destination, transfer amount, and the payment method you choose. Typically, Small World's fees are relatively low compared to traditional banks and other money transfer services. To get an accurate estimate of the costs for your specific transfer, you can use the online calculator provided on their website, which takes into account the transfer amount and the destination country.

For the United States, you can send up to $2,499.99 per transaction.

The speed of your money transfer with Small World varies depending on several factors, such as the destination and the chosen payment method. In many cases, Small World offers relatively fast transfer times, allowing your recipients to access funds within minutes to a few business days. However, it is important to note that transfer times may be longer in some regions due to local banking regulations and holidays.

For a more precise estimate of the processing times, you can utilize the transfer time estimator tool. Once you enter the basic information it asks on the home page, this tool offers an approximate indication of the timelines for receiving your funds into your Small World account.

You might be wondering, is Small World reliable? Don’t worry! Small World prioritizes the security of its customers' financial transactions. It is a licensed and regulated money transfer service in various countries, ensuring compliance with stringent financial regulations. Small World employs industry-standard encryption and security measures to protect your personal and financial information during the transfer process. Additionally, the company has a dedicated customer support team to assist customers with any issues or concerns.

Now for the biggest question you must have: how does Small World work?

Luckily, using Small World for your international money transfers is relatively straightforward. Here's a step-by-step guide:

Small World provides a tracking feature that allows you to monitor the status of your transfer in real-time either from the Small World app or your online login.

Small World offers various ways to contact their customer support team for assistance or inquiries.

Small World has a comprehensive help center or FAQ section on their website. This resource can provide answers to many common questions and guide you through various aspects of using their service.

Still need help with Small World? Call the support team at any time at their Small World customer service number: 1(866) 210-8002

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Small World money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Small World service are:

One of Small World's standout features that sets it apart in the competitive landscape of money transfer services is its convenient home delivery option. Depending on your eligibility, Small World offers the unique service of delivering your money directly to your doorstep. This feature gives Small World a significant competitive edge, making it an excellent choice for individuals sending money back home to their loved ones, especially parents. The ability to have funds hand-delivered ensures not only the convenience of the recipient but also adds a personal touch to the transaction, setting Small World apart as a reliable and caring money transfer service. This distinctive receiving option reflects Small World's commitment to offering tailored solutions that truly meet the diverse needs of its customers.

If you’re looking for an alternative to Small World’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Small World? Let’s see what users of Small World have to say. Sourced from multiple platforms, customer reviews of Small World are:

Small World scores a “Great” rating on TrustPilot with a TrustScore of 4.2 out of 5.

“Have been using their service for a long period. I have found them trustworthy. Had few small issues but that’s manageable. Will recommend.” - Md Mahmudul on TrustPilot

“The site is userfriendly, the money is transfered quickly, and the first time I wanted to transfer money, Small World called to secure that I was the person I claimed to be. Best solution for transfering money to Cuba so far :-)” - Roy Solnes on TrustPilot

Negative reviews pertain to issues with transfer delays and speeds.

Small World is a reputable international money transfer service that offers a convenient, secure, and cost-effective way to send money across borders. With its extensive global network, competitive pricing, and commitment to customer security, Small World has earned its place in the competitive world of money transfer services. Whether you're sending money to loved ones or conducting business overseas, Small World is a reliable option to consider, thanks to its unique strengths and extensive coverage.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

6965 views

6965 views

.jpg?v=46)