The evolution of money transfer services has significantly changed the way we handle financial transactions. Unplex Money Transfer, an innovative application, has gained attention for its unique approach to seamless and secure monetary transfers. Unplex Money Transfer offers users a seamless way to send money through WhatsApp.

In this review, we will explore the unique features, functionality, safety measures, and overall efficacy of the Unplex App for money transfers, particularly its integration with WhatsApp for seamless international transactions.

Unplex Money Transfer is a cutting-edge financial platform that facilitates easy, secure, and swift money transfers. Unplex stands out from the variety of remittance solutions in its integration with popular messaging app WhatsApp, enabling users to send money domestically and internationally directly through the WhatsApp interface. The seamless amalgamation of Unplex with WhatsApp streamlines the process, making it highly convenient for users.

Countries supported by Unplex Money Transfer include:

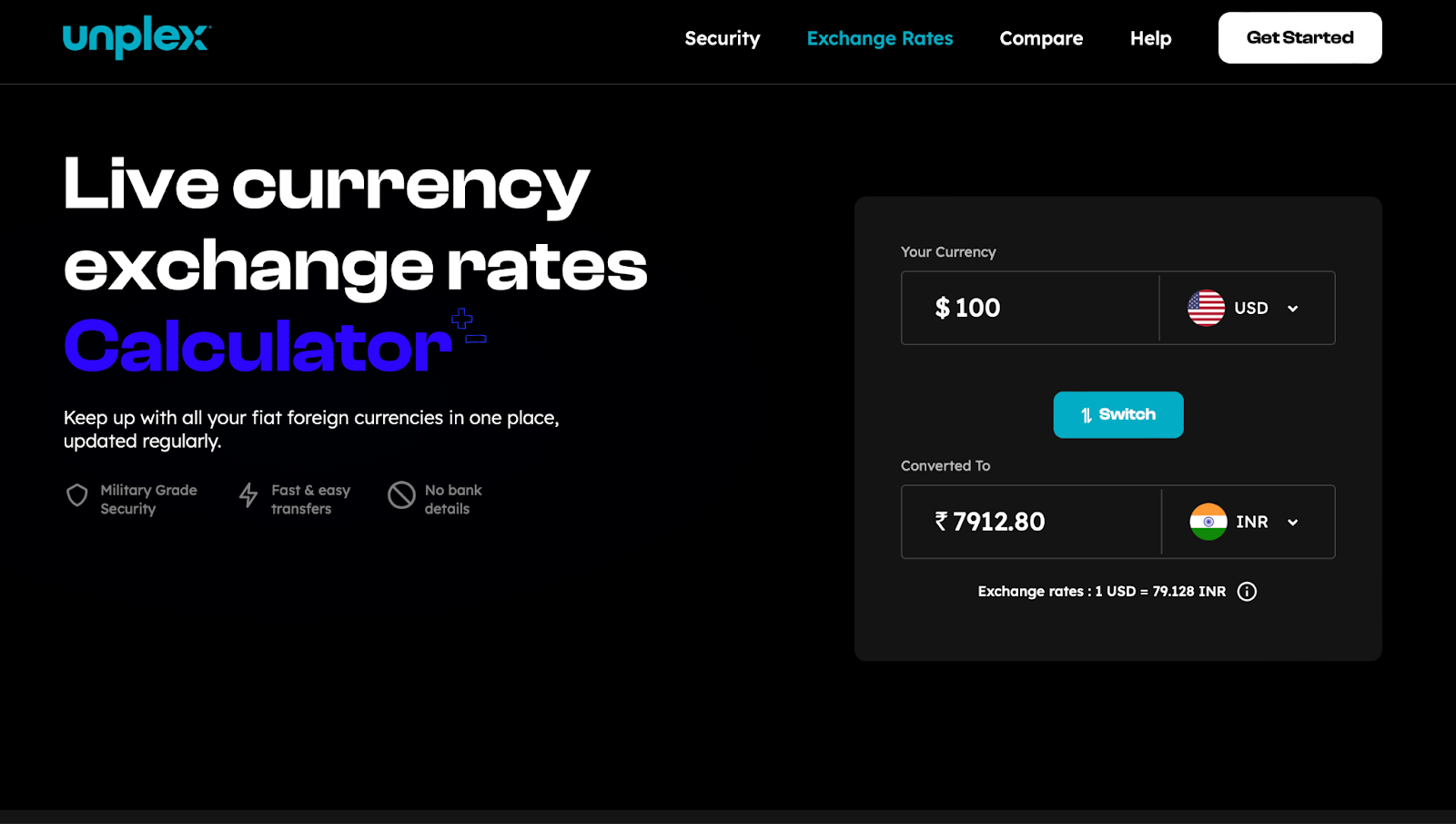

To view a complete list of countries that Unplex serves, navigate to the “Exchange Rate” page. There you will find the money transfer calculation tool. Select the drop down menu for the receiving country and you will be shown all the countries you can send money to!

One of Unplex's remarkable aspects is its cost-effectiveness. Users can transfer money using the Unplex App at a minimal cost compared to traditional banking methods or other money transfer services. The fees for transactions are competitive, often lower than those charged by conventional banks or standalone money transfer services.

Unplex places a fee of $0.99 for every $100 you send

Unplex allows you to send $3,000 per day and $10,000 per month. It is important to note that Unplex may ask you to validate additional information for security purposes if you want to send more than the limit.

Unplex is recognized for its swift transaction speeds. Typically, transfers through the Unplex App, especially within domestic boundaries, occur almost instantaneously. Your recipient will receive their money within 1 business day if not within 30 minutes.

Unplex prioritizes the security and privacy of its users' financial information. The app employs robust encryption techniques and follows strict security protocols to safeguard transactions and user data, ensuring a secure money transfer environment.

Now for the biggest question you must have: how does Unplex work?

Staying true to their mission of creating a money transfer service that prioritizes convenience, using Unplex is relatively straightforward. Here's a step-by-step guide:

Unplex offers various ways to contact their customer support team for assistance or inquiries.

Unplex has a comprehensive help center or FAQ section on their website. Here you can get answers to many common questions and get guided through various aspects of using their service.

If you have a more personalized question, you can chat with their support bot by going to the “Help” section of the Unplex app site.

Still need help with Unplex? Send an email to the support team at any time at: [email protected]

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Unplex money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Unplex service are:

Unplex app's standout feature is its groundbreaking integration with WhatsApp, redefining the landscape of money transfers. What sets Unplex apart from its competitors is its seamless incorporation of financial services within the widely-used messaging platform. This unique integration offers users an unparalleled level of convenience, enabling them to effortlessly send money directly through WhatsApp's familiar interface.

Unlike many competitors in the market, Unplex simplifies the entire remittance process by providing a user-friendly, intuitive, and secure platform that operates within WhatsApp, eliminating the need for separate apps or complex procedures. This distinctive approach distinguishes Unplex as an innovative solution that maximizes ease-of-use and accessibility for individuals seeking swift and hassle-free money transfers.

If you’re looking for an alternative to Unplex’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

In summary, Unplex Money Transfer presents a compelling option for individuals seeking a convenient, secure, and efficient means of sending money domestically and internationally. Its integration with WhatsApp amplifies its usability, making financial transactions more accessible within the familiar interface of a widely-used messaging app. While some limitations exist, Unplex stands as a promising solution in the evolving landscape of digital finance.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

6505 views

6505 views

.jpg?v=46)