Wells Fargo is a worldwide financial institution founded back in 1852 by Henry Wells and William G. Fargo that began as just a hopeful start-up looking to help build businesses and improve the management of money for the average person. Today, Wells Fargo operates in 35 countries and serves over 70 million customers worldwide.

In addition to the bank services that Wells Fargo offers, they have branched out into the remittance sector with their service Wells Fargo ExpressSend, a simple way for Wells Fargo account holders to send money abroad.

In this Wells Fargo ExpressSend review, we will explore the essential features, advantages, and disadvantages of this service and whether or not it is a viable option when choosing a remittance provider.

Let’s take a closer look at the Wells Fargo remittance service and whether or not it is a preferred choice for sending remittance overseas.

Wells Fargo ExpressSend® is a person-to-person remittance service that allows individuals in the United States to send money electronically to 13 countries worldwide. To use this service, you’ll need an eligible Wells Fargo checking or savings account. Money can be sent through Wells Fargo Online®, the Wells Fargo Phone Bank, or at a Wells Fargo Bank branch location.

When sending through Wells Fargo, you can also choose how your recipient gets the funds - either in their account through their receiving bank or cash pick-up. Wells Fargo has over 50 Remittance Network Members and has ties with over 49,000 payout locations.

Countries supported by Wells Fargo ExpressSend® include:

Wells Fargo ExpressSend® does not charge any fees for enrolling in the service or for continuing to be enrolled in the service. The recipient of the funds also pays no fees.

The only cost is a transaction fee which is a one-time fee for each transaction. These transaction fees are country-specific and vary. There are also limits per country of how much you can send in a single transaction.

You can estimate the exact cost of your transaction using their ExpressSend Remittance Cost Estimator.

The minimum amount of money you can send daily is $25. The limits vary per country, but are relatively low compared to other remittance services. For example, Mexico limits range from $500 to $1,600 depending on whether your recipient is picking up cash or receiving bank credit.

There are also daily limits per user for all beneficiaries if sending multiple transactions. You can only send up to $5,000/day total, and only up to $12,500 in a consecutive 30-day period.

You can find a complete list of limits for individual countries supported on the Wells Fargo website.

Signing up for Wells Fargo ExpressSend® first requires you to have an eligible checking or savings account with Wells Fargo. If you are an account holder, follow these steps to set up your first remittance transaction.

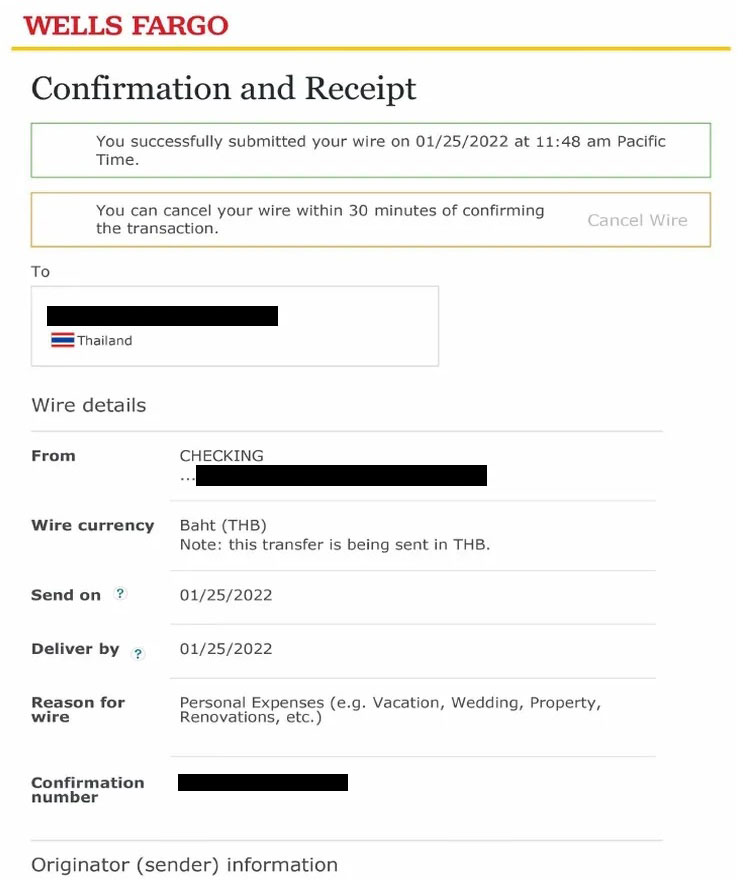

Source: https://www.scribd.com/document/594651200/WELLS-FARGO-WIRE-5#

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Wells Fargo ExpressSend® service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Wells Fargo ExpressSend® service are:

The best feature of the Wells Fargo ExpressSend® Service is the convenience of sending funds straight from your existing bank account as well as the ability to track your transaction in your online account.

If you’re looking for an alternative to Wells Fargo’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

If you are a current Wells Fargo checking or savings account holder, it may be convenient for you to take advantage of this service.

However, due to the poor exchange rates and lengthy turnaround time for transactions, we believe there are many other top-rated remittance providers that may better suit your needs.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

26863 views

26863 views

.jpg?v=46)