When it comes to sending money across borders or even just across town, reliability, speed, and security are non-negotiable factors. In an age where financial transactions are the lifeblood of our interconnected world, one name has stood the test of time: Western Union. With a legacy spanning over a century, Western Union has been the go-to choice for countless individuals and businesses seeking to move money seamlessly.

As we dive into this comprehensive review and guide to Western Union's money transfer services, we will explore its rich history, the diverse range of financial solutions it offers, and provide you with a step-by-step roadmap to navigate the world of international money transfers.

Whether you're a first-time user seeking clarity or a seasoned sender looking for the latest insights, this article is your go-to resource for harnessing the power of Western Union's global financial solutions.

Join us as we uncover the secrets to safe, efficient, and convenient cross-border transactions, helping you decide whether Western Union’s money transfer is the right option for your next transfer.

Western Union is a well-established and globally recognized financial services company that specializes in money transfers and cross-border payments. Founded in 1851, it has a long history of providing secure and convenient solutions for sending and receiving money across international borders.

Western Union allows individuals to send money to recipients in different countries. Senders can initiate transfers through Western Union's agent locations, online platforms, or mobile apps. Recipients can typically collect the funds in their local currency from nearby Western Union locations.

In many regions, Western Union has partnered with mobile money providers to enable financial access and transactions via mobile devices, especially in underserved areas. To further ease the money transfer process, Western Union offers online and mobile applications that enable users to initiate and track money transfers, check exchange rates, and manage their transactions conveniently from their computers or smartphones.

To send money with Western Union, you will need to simply create a free online account. Once you have secured your Western Union login, you can begin the money transfer process through westerunion.com or the Western Union mobile application.

Western Union takes great pride in its global network, allowing customers to easily move their money to over 200 countries:

The cost of a money transfer with Western Union can vary widely based on several factors, including the amount you're sending, the destination country, the method of payment, and the delivery method.

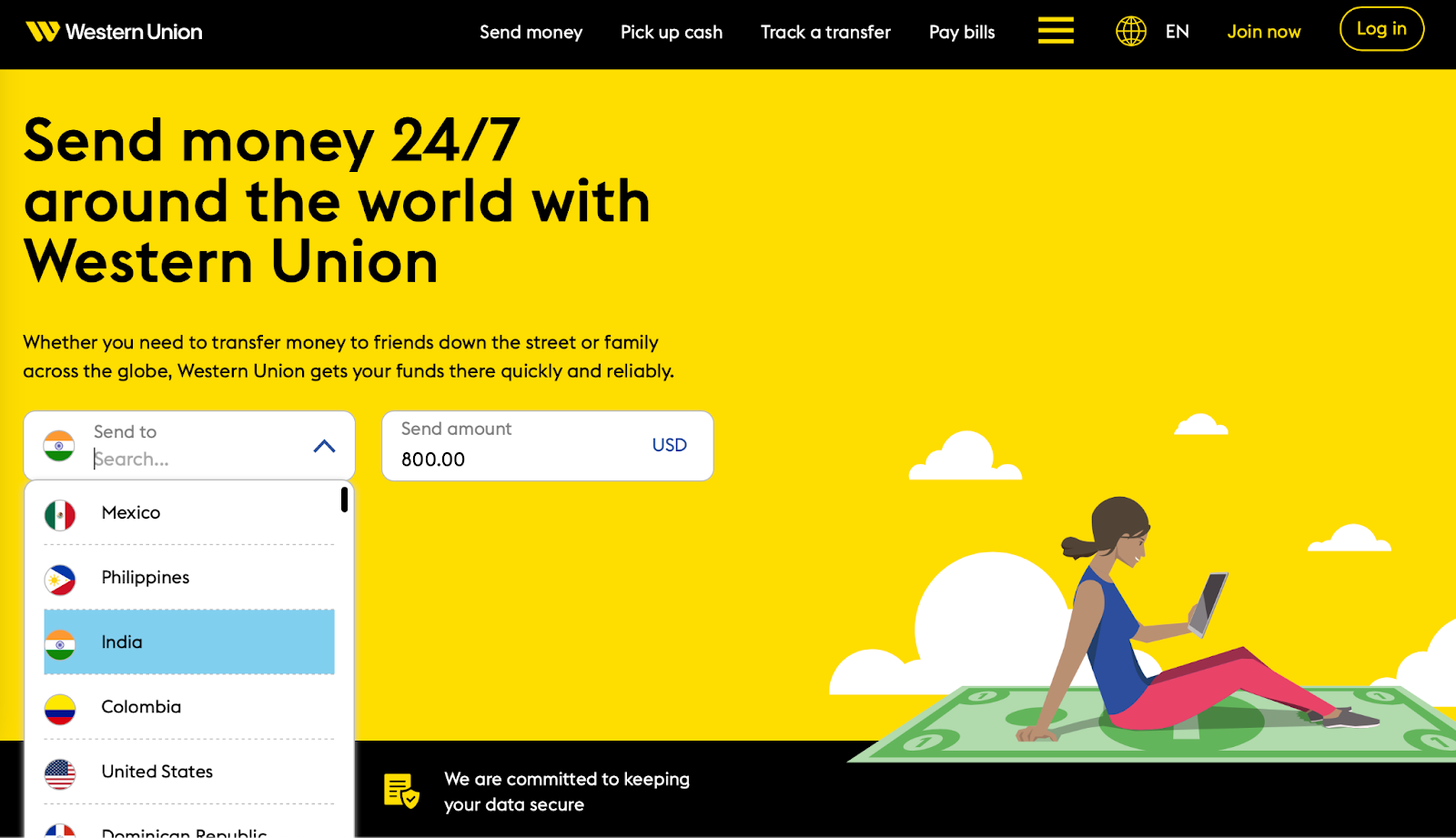

Luckily, there is a way you can get an accurate estimate of all the nitty gritty details of your transfer before you even begin the transfer process. If you want to get an estimate of what your transfer fees will look like, navigate to the “Send To” dropdown on the Western Union home page. This is their money transfer calculation tool. You will now select the country you would like to transfer money to.

Then, you will be taken to a page where you can indicate the exact amount of money you plan to transfer to the country of your choice. This is where you will find all the details having to do with your transfer. Western Union will transparently display information such as your fee breakdown, your exchange rate based on payment method, the variety of ways your recipient can receive their money, how long the transfer will take, any Western Union’s promo codes available to you, and more.

(At the time of writing this article, new users of Western Union get the offer of having no transfer fees on their first transfer)

If you are still unsure about your fee breakdown, you can get an accurate estimate of the cost for your specific money transfer by initiating the transfer process or by contacting a Western Union agent.

Transfer amount limitations can be placed both by Western Union and the country that your recipient will be receiving their funds in.

Luckily, Western Union’s transfer limits are very straightforward. With Western Union, you can transfer up to 3,000 USD without identity verification. Once you have verified your identity online or through a Western Union agent, you can transfer up to 5,000 USD. If you are not transferring using USD, your limit is the adjusted equivalent.

The time it takes for a Western Union money transfer to be completed can vary depending on several factors.

The speed of the transfer can depend on the delivery method chosen. Western Union typically offers options like "Money in Minutes," "Next Day," and "2-5 Days." "Money in Minutes" is the fastest option, allowing the recipient to pick up cash or have the funds delivered within minutes after the transfer is sent. Other options may take longer.

The method you use to pay for the transfer can also impact the time it takes for the funds to be available to the recipient. For example, using a credit card or debit card can result in faster processing compared to paying with cash at an agent location.

Still, to ensure the most convenience for their customers, Western Union typically aims to complete transfers within 0-4 business days, if not completed in minutes.

Western Union employs several measures to keep your money transfer safe and secure. These measures are designed to protect both senders and recipients from fraud, unauthorized access, and other potential risks.

Before all else, Western Union adheres to strict AML and KYC regulations, which require them to verify the identities of customers and report suspicious transactions to relevant authorities. This helps prevent money laundering and other illicit activities.

To protect your identity, Western Union requires both senders and recipients to provide valid identification when sending or receiving money.

Western Union uses encryption technology to secure the transmission of sensitive data, such as personal information and financial details. This encryption helps protect your information from interception by unauthorized parties during the transfer process.

Putting the power in your hands, Western Union provides customers with the ability to track their money transfers online or through their customer support services.

While Western Union takes these security measures seriously, it's also important for customers to play their part in ensuring the safety of their money transfers. This includes safeguarding the Money Transfer Control Number (MTCN) and not sharing it with unauthorized individuals, as well as being cautious when sending money to unknown recipients or in response to unsolicited requests.

Now for the biggest question you must have: how does Western Union work?

Sending money with Western Union is a straightforward process. Western Union has designed a user-friendly system to ensure the most efficient and hassle free transfers for their customers.

If you haven’t secured a free login yet, go ahead and sign up for Western Union now. This is how you will begin the money transfer process. You can create an account on the Western Union website or the Western Union app.

Now let's dive into how to transfer money with Western Union:

That's it! Your money transfer is complete, and the recipient can collect the funds at a Western Union agent location or through the chosen delivery method.

Should you need assistance with your Western Union money transfer, contacting customer service is straightforward. They offer various support methods:

Physical agents:

Visit an authorized agent location for in-person support.

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Western Union money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Western Union service are:

Western Union's standout feature lies in its exceptionally comprehensive and transparent money transfer calculation tool, readily accessible on its homepage. With just a few clicks, you can select your destination country and the amount you wish to send, and voilà, you gain access to a wealth of crucial transfer details.

Here, Western Union doesn't hold back, providing a complete breakdown of fees, exchange rates based on your chosen payment method, an array of options for your recipient to receive the funds, estimated transfer duration, available promo codes, and more.

Notably, the tool even takes the complexity out of fee calculations, transparently displaying your total fee, sparing you the need for manual calculations.

This level of transparency and comprehensive information sets Western Union apart, offering a convenience that many of its competitors simply do not provide.

If you’re looking for an alternative to Western Union’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Western Union? Is Western Union legit? Understanding user feedback provides the best assurance. Western Union scores an “Excellent” status on TrustPilot with a TrustScore of 4.3 out of 5.

In conclusion, Western Union has proven itself as a reliable and accessible option for international money transfers and bill payments. Its extensive global network, multiple transfer options, and commitment to security make it a valuable choice for those needing to send funds across borders. For quick and convenient transfers to loved ones or for essential bill payments, Western Union can be an excellent choice.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

Western Union can stop unpaid transfers and issue refunds upon request. You must immediately contact the fraud department at 1-800-448-1492 or submit an online fraud claim form to initiate the process.

Call Western Union's verification line at 1-800-325-6000 or visit an agent location with the money order details.

You can track your transfer online or via customer support using the money transfer control number (MTCN) provided after completing the transfer.

Funds typically expire after 90 days if unclaimed, though this varies by destination country.

No, recipients can collect cash at agent locations without a bank account. Sender payment methods may vary.

Transfer limits help ensure security and compliance with financial regulations while giving you flexibility based on your verification status.

40113 views

40113 views

.jpg?v=46)