Finding the right service to use for your international money transfer needs is very tricky. Especially with the list of options of money transfer services being longer than ever.

Placid Money Transfer is a service that has gained significant attention for its efficiency and ease of use. In this comprehensive review and guide, we will delve into the features that make Placid unique, explore its cost-effectiveness, safety measures, and provide you with a step-by-step guide on how to transfer money using this platform.

By the end of this Placid Money Transfer review, you will have a clear understanding of whether Placid is the right choice for your money transfer needs.

Placid Money Transfer is a financial technology platform that facilitates international money transfers. What sets Placid apart is its focus on providing a user-friendly and cost-effective solution. Unlike traditional banks, Placid offers competitive exchange rates and lower transfer fees, making it an attractive choice for those seeking affordable international money transfers. Placid also boasts a user-friendly interface and offers both mobile and web-based platforms for convenience.

Placid’s money transfer expertise lies in transferring money to Asia, making them an excellent option to send money home to loved ones. However, they do serve a larger list of countries.

Countries that Placid sends money to include:

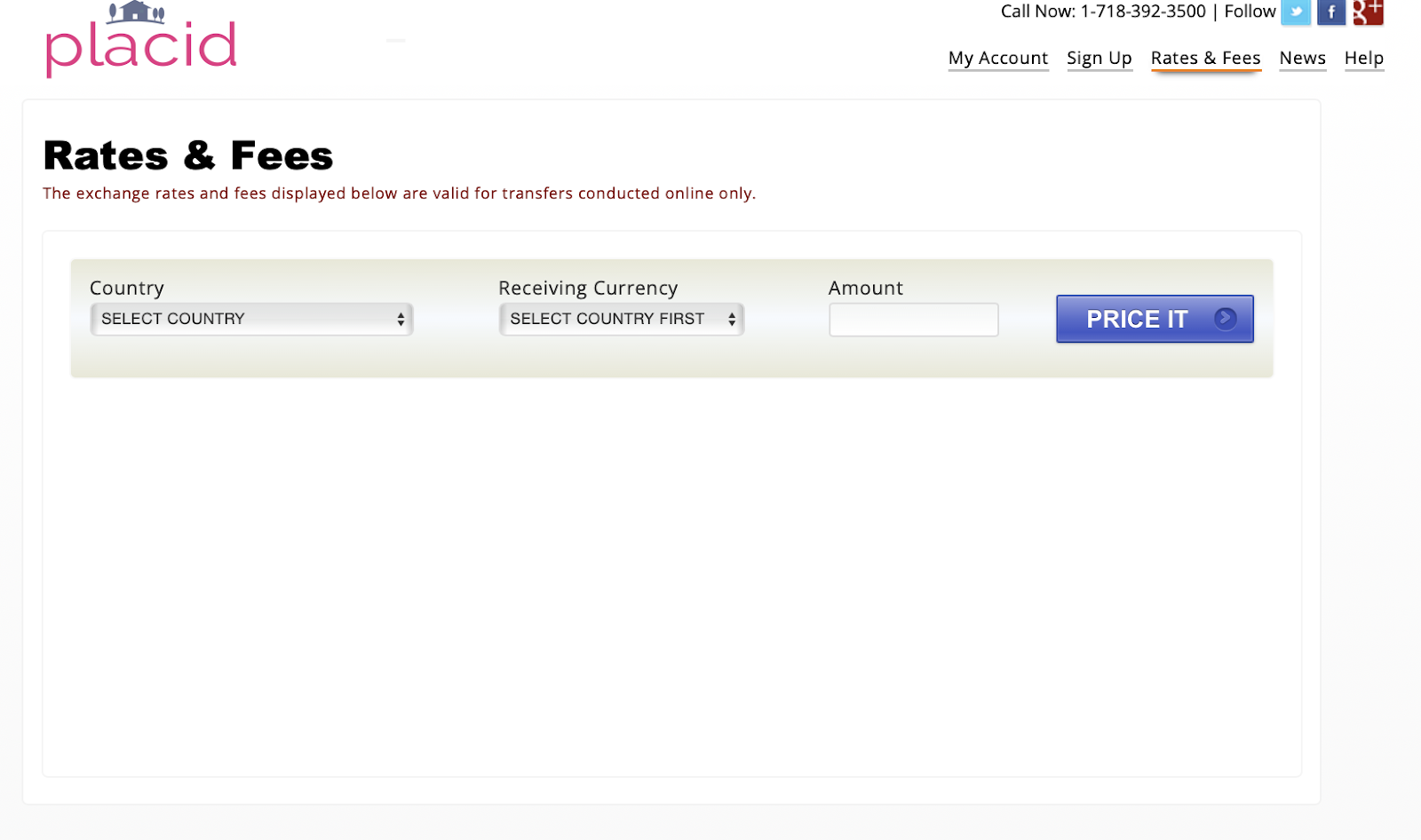

To make sure that Placid services to the country you want to send money to, navigate to the home page. There you will find the money transfer calculation tool. Select the drop down menu for the receiving country and you will be shown all the countries you can send money to! Another option is to go to their “Rates and Fees” tab and click the dropdown menu labeled “Country,” and all of the countries they service to will appear.

Placid’s fee structure can be tricky for those who don’t know how to look for it. The fee and exchange rate differs per country. To check how much you will be charged and what your exchange rate will look like, navigate to the “Rates and Fees” page. Then, you will select the country that you want to transfer money to. At this point, the currency of that country will automatically appear. Then, you can enter the amount of money you want to transfer and your exchange rate and fees will appear.

In most cases, Placid customers are allowed to send up to $9,900 within a 30-day period. It's important to note that the Placid money transfer limit might combine transactions within your household or with other parties if we suspect a connection between them. When using a debit card, the maximum per transaction is $3,000.

Keep in mind that certain payout institutions might have their own limits, and Placid might lower your limit without notice. They might also ask for extra information or documents due to regulatory requirements or their internal procedures. This could be necessary regardless of the amount you're transferring.

You have two options for your payment that will affect your fees. If you use a US based bank account, you will benefit from the lowest fees. If you use a debit/credit card, the fees are higher but your money transfer is usually approved faster.

Placid offers competitive transfer speeds. The time it takes to transfer money with Placid depends on factors like the destination country, currency, and the chosen delivery method. Generally, many transactions can be completed within 1-3 business days. Placid provides real-time tracking and notifications, allowing users to monitor the progress of their transfers with ease.

Here is the estimated transfer time based on payment option:

[From Placid Help Centre]

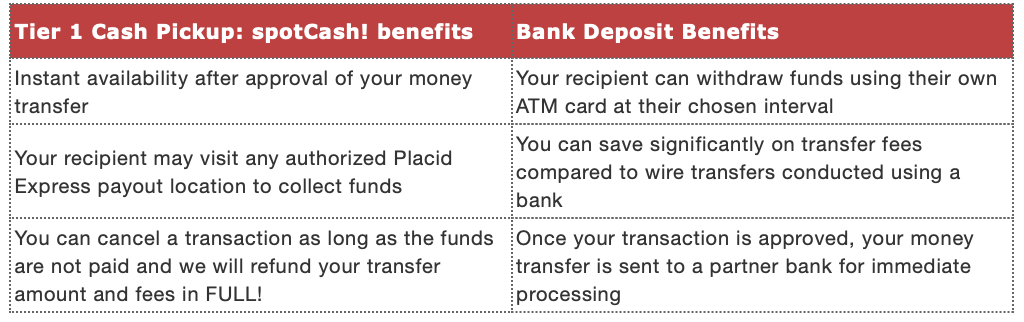

For customers seeking flexibility and convenience in transferring money, Placid offers versatile options. The Tier 1 Cash Pickup service, spotCash™, permits recipients to collect remitted funds at authorized Placid Express payout locations in their country. This requires presenting a valid government-issued identification document.

Additionally, their Bank Deposit service provides a secure and swift method to directly deposit funds into your recipient's bank account. Typically, you'll need to provide the account holder's name, bank details, and account number for the transaction. Placid ensures seamless transfers, catering to diverse recipient preferences.

Here are the benefits of Placid’s spotCash™:

[From Placid Help Centre]

Security is a top concern when it comes to international money transfers. Placid understands this and prioritizes safety. The platform uses robust encryption and authentication protocols to safeguard user data and financial information. It also complies with the relevant financial regulations and operates under licenses in different countries. Users can have confidence in Placid's commitment to maintaining the highest security standards.

Now for the biggest question you must have: how does Placid work?

Luckily, using Placid for your international money transfers is relatively straightforward. Here's a step-by-step guide:

Placid offers various ways to contact their customer support team for assistance or inquiries.

To get a frequently asked question answered, visit their Help Centre. You can find a in depth breakdown of the whole process of transferring money with Placid here.

You can also reach out to Placid customer service or submit a question by contacting the Placid customer support team via their email: [email protected]

Still have questions? Contact Placid by calling their 24/7 support line at 1-877-889-7021

Based on our research of customer reviews and comparison to other remittance providers, the pros of the Placid money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the Placid service are:

Placid’s standout feature, spotCash™, revolutionizes the money transfer experience with its seamless Cash Pickup system. This innovative Tier 1 service enables recipients to swiftly collect remitted funds from any authorized Placid Express payout location in their country. The process is incredibly straightforward – recipients need only present a government-issued valid identification document.

What truly sets spotCash apart is its speed; as soon as the processing is complete, the cash is ready for pickup. This means recipients can access their funds immediately, eliminating the wait associated with traditional banking methods. Placid's dedication to providing instant access to funds through spotCash ensures a hassle-free and efficient transaction process, setting it apart as a leader in the realm of international money transfers.

If you’re looking for an alternative to Placid’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about Placid? Is Placid legit? Let’s see what users of Placid have to say. Sourced from multiple platforms, customer reviews of Placid are:

Placid scores an “Great” rating on TrustPilot with a TrustScore of 4.2 out of 5.

“Placid don’t wait for commitment date they provided during the transaction initiation.

All the times they deposit the money well before the commitment date.” - Suraj Jaiswal on TrustPilot

“It was fast transfer. Making transactions for a long time with Placid express. Experienced and polite agents are working 24 hours to serve people in Placid. I trust Placid more than any other Money transfer agents.” - Mohammad Moniruzzaman

on Trust Pilot

Negative reviews pertain to issues with communication, fluctuating exchange rates, and transfer delays.

To see even more trusted reviews from users of Placid, check out CompareRemit’s review page.

Placid Money Transfer is a promising option for individuals seeking a cost-effective, secure, and efficient way to send money internationally. Its competitive exchange rates, low fees, and user-friendly interface make it a compelling choice for cross-border financial transactions. By prioritizing safety and compliance, Placid has earned the trust of users worldwide. To explore its benefits further, sign up for Placid, and experience a streamlined and affordable international money transfer solution today.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

5618 views

5618 views

.jpg?v=46)