As the global economy continues to evolve, so do the ways we send and receive money across borders. One name that has gained prominence in this arena is WorldRemit. Offering a platform designed to simplify global financial transactions, WorldRemit has garnered attention for its user-friendly interface and competitive rates. In this review and guide, we will explore WorldRemit's features, fees, security, and how to use it for your next money transfer.

Whether you're supporting family abroad or conducting cross-border business, join us on a journey through WorldRemit's offerings, as we explore the potential benefits of choosing this service for your international money transfer needs.

WorldRemit is a digital money transfer service founded in 2010. It allows users to send money to over 150 countries worldwide, covering a vast network of destinations. With a mission to make sending money as easy as sending an instant message, WorldRemit offers a convenient and cost-effective way to transfer funds internationally.

Countries supported by WorldRemit Money Transfer include:

To view a complete list of countries that WorldRemit serves, navigate to the home page. There you will find the money transfer calculation tool. Select the drop down menu for the receiving country and you will be shown all the countries you can send money to!

To get started with WorldRemit, begin by creating a WorldRemit account on their website or mobile app. You'll need to provide your personal information and verify your identity in compliance with regulatory requirements.

WorldRemit's fees for money transfers can vary based on several factors, including: transfer method and where you are sending money to.

Regardless, WorldRemit prides itself on being one of the most affordable remittance services on the market. Sending money to most countries will typically have a standard fee of $3.99 applied; although this cost may decrease to as little as $1.99 depending on specific transfer conditions.

Pro tip! WorldRemit will often have some promo code or promotional offer available, so we advise that you keep an eye out and see if there is one you can use before you begin your transfer process.

Depending on your location, the methods available for sending money through WorldRemit can vary. Fortunately, there is typically a wide array of options for you to use. Here are some of the methods you can use to send and receive money via WorldRemit:

These versatile options cater to various preferences and needs, making WorldRemit a flexible and user-friendly platform for international money transfers.

The maximum amount of money you can send using WorldRemit can vary by your payment method.

If you are paying for your WorldRemit transfer with debit, credit, or pre-paid cards, you have a maximum sending amount of 9,000 USD in 24 hours and 5,000 USD per transaction.

If you are paying for your WorldRemit transfer with ApplePay, you have a maximum sending amount of 9,000 USD in 24 hours and 300 USD per transaction.

The speed of WorldRemit's transfers relies on your chosen delivery method. f you select cash pickup, mobile money, or airtime top-up, your funds can be available within minutes, if not instantly.

If you are transferring money using a bank transfer, it can take up to 2 business days; if you are transferring money using a home delivery service, it can take up to a week.

WorldRemit is considered a reputable and safe platform for international money transfers.

WorldRemit operates under the regulations of various financial authorities in the countries where it offers services. These regulations are in place to ensure the company complies with anti-money laundering (AML) and know your customer (KYC) requirements. By following these regulations, WorldRemit helps prevent fraudulent activities and money laundering.

WorldRemit uses strong encryption techniques to protect the transmission of data between users and its platform. This ensures that your personal and financial information remains confidential and secure during the transfer process.

Right off the bat, WorldRemit requires you undergo identity verification procedures to confirm the identity of its users. This may include submitting government-issued identification documents and other relevant information to verify your identity before you can use the platform.

Regardless, always make sure to exercise caution and follow best practices for online security when using any financial platform.

Now for the biggest question you must have: how does WorldRemit work?

Getting started with WorldRemit is a straightforward process. Here's a step-by-step guide:

WorldRemit offers various ways to contact their customer support team for assistance or inquiries.

Based on our research of customer reviews and comparison to other remittance providers, the pros of the WorldRemit money transfer service are:

Based on our research of customer reviews and comparison to other remittance providers, the cons of the WorldRemit service are:

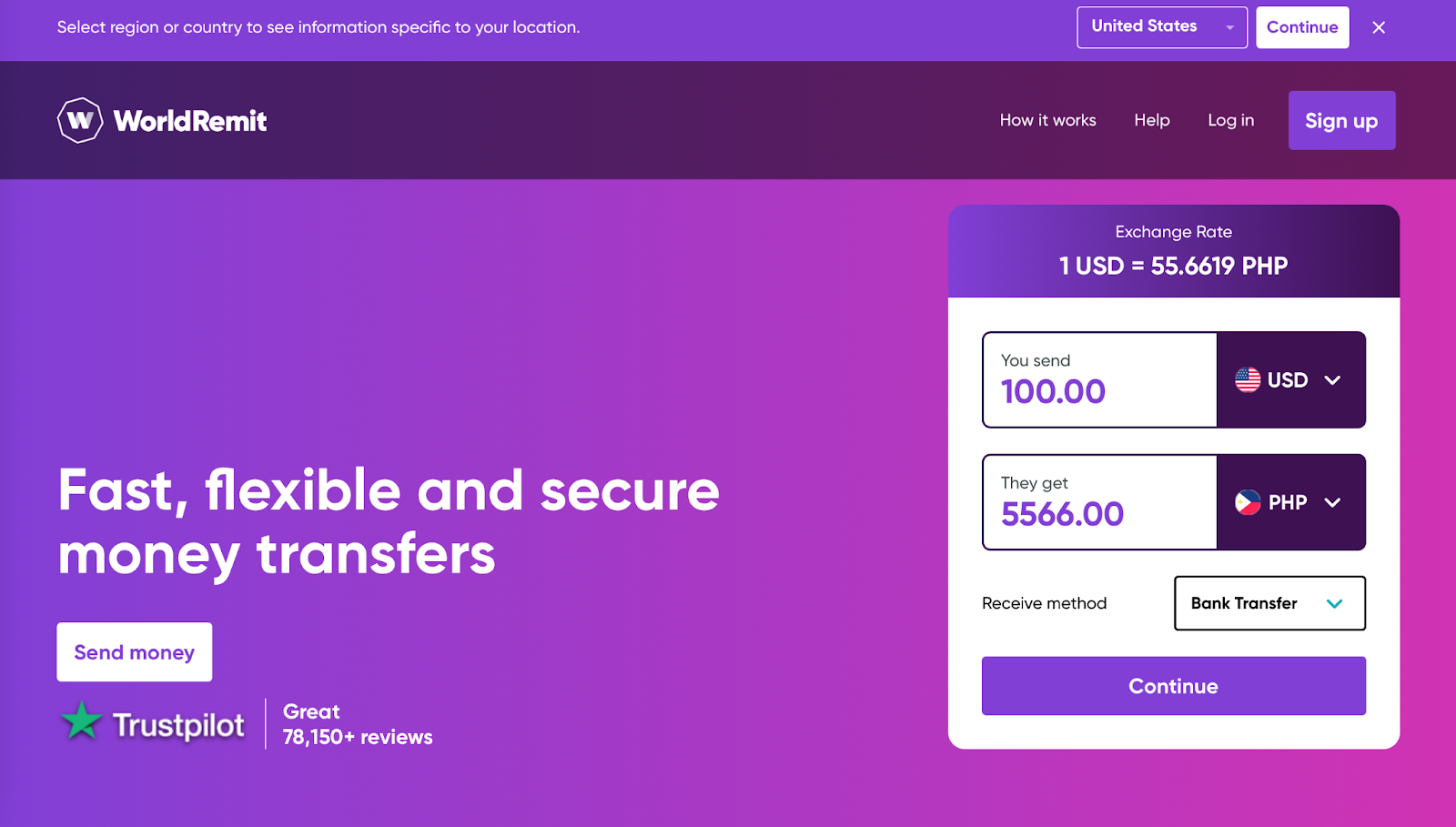

As we briefly mentioned it before, WorldRemit's standout feature is undoubtedly its user-friendly transfer calculation tool.

Accessible right from the homepage, this tool requires only a few key details – without needing any personal information. You input your recipient's receiving country and your chosen transfer method, and in an instant, you're presented with a comprehensive breakdown of your proposed transfer. From estimated transfer times to precise fee calculations and more, it offers unparalleled transparency, providing you with the clearest possible view of your transaction before you proceed.

This invaluable tool ensures that your money transfer experience with WorldRemit is both straightforward and fully informed.

If you’re looking for an alternative to WorldRemit’s remittance service, here are some top remittance providers we recommend that offers low fees, excellent exchange rates, and are easy to use:

Need more assurance about WorldRemit? Let’s see what users of WorldRemit have to say. Sourced from multiple platforms, customer reviews of WorldRemit are:

WorldRemit scores a “Great” rating on TrustPilot with a TrustScore of 4.1 out of 5.

“Once again, a flawless transfer! There are times when a number is "mistyped" or times when the connection between WorldRemit and MasterCard has a hiccup, but generally, my transactions are timely and flawless, and I'm very pleased with the service.” - Steve A. on TrustPilot

“I am a long-term customer of WorldRemit. I use them to send money internationally to myself and to friends and family. Their fees are the cheapest I have come across. They are very cheap as compared to regular bank wire transfers. For about one dollar I can send money and it is received instantly. I therefore have no use for regular bank wire transfers.” - Mazhar C. on Supermoney

“The ease of the process of sending money. I have one recommendation, can you guys add to your system info on where the recipients pickup the money exactly. Which particular outlet that the money is received from and have that info placed into the transaction history on my account.” - James on Trustpilot

Negative reviews pertain to issues with identity verification and transfer cancellations as a result.

To see even more trusted reviews from users of WorldRemit, check out CompareRemit’s review page.

WorldRemit is a convenient and reliable platform for international money transfers, offering a wide range of transfer methods, competitive exchange rates, and a strong commitment to security. Whether you need to support family, pay bills, or invest overseas, WorldRemit provides an efficient and user-friendly solution.

In a world that's becoming increasingly interconnected, having a trustworthy money transfer service like WorldRemit at your fingertips can make managing your global finances easier and more convenient than ever.

We invite you to compare remittance providers using CompareRemit’s comparison tool today to find the best rates, lowest fees, and fastest turnaround times for your specific destination and transfer amount.

23674 views

23674 views

.jpg?v=46)